Chart above of the Agri-Food Price Index makes a very clear statement on the state of Agri-Food prices. Index continues at a new cycle high. Versus the all time high of 2008, it is down only 3%. Those results compare more than favorably with the dismal results of the U.S. equity markets.

While the prices of Agri-Foods do not translate directly into investment performance, it is the framework for returns to be earned by those investments. Further, movement of Agri-Food prices is based on global markets that are tightening in a permanent manner. Many misinformed pundits have failed to note continuing growth of demand for Agri-Foods due to income growth in China and India. And most important, the market for wheat and the market for iron ore are different markets.

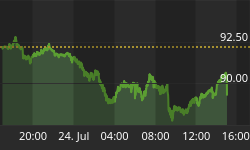

When we visited last, wheat, in above chart, was just beginning the break out from the bear trend in which it had been trading. In a matter of weeks, the price of wheat has moved more than 70%, and recently made a new 90-week high. Further, that price action has moved the entire global grain market to higher prices. If those using wheat as animal feed, particularly in Russia, are unable to obtain wheat, they will utilize some other grain. That shift to other grains will push up those prices.

The catalyst, not the cause, of higher wheat and grain prices is the severe drought in Western Russian and surrounding region. Russia, a major wheat exporter, has banned wheat exports through December. That date is important as wheat is not produced in a factory, but rather grown in a field. Clearly, no grain is produced in Russia in December or January. That date does, importantly, allow sufficient time to determine the potential of the Russian winter wheat crop which should be put in the ground next month. However, at the present time the drought has so reduced ground moisture that much of the Russian winter wheat crop may not be planted.

Real cause of higher wheat prices, as well as higher grain prices in general, is world's just in time inventory approach to Agri-Food. Most nations and food businesses operate as if the world was awash in Agri-Food. Just in time inventory management works with continuous manufacturing processes. It is doomed to regular failure given annual batch production of Agri-Food.

USDA's most recent forecast places wheat stocks in the next year at only 3.2 months of consumption. As that is the average and includes the massive reserves of China, much of the world has far fewer months of wheat consumption in reserve. For the world, the difference between shortages of 2008 and today's supplies is only about 0.8 months of consumption. Converted to days, world has 24 days more of wheat than it did in 2008. Eat up, while you can.

As is apparent in the above graph, a clear beneficiary of all this is U.S. grain exports. That graph portrays the year-to-year change for U.S. grain that has been exported or is to be exported in the current crop year. U.S. has exported 13% more grain this year than last. Export sales yet to be exported are up 19%. Taken together, U.S. grain exports are up 14%. Accelerating those trends are U.S. export sales of wheat, June 1 start of crop year, which are 53% ahead of last year. Rice export sales, which started a new crop year 1 August making the statistics less than ideal, are up 57%.

While Russia suffers from lack of water, Pakistan is suffering from too much water. Floods in that country have destroyed 17 million acres of planted crops and more than a million tons of grain in storage have been washed away. Pakistan had the world's largest integrated irrigation system, and the damage to that system is extensive but unknown at the present time. As the world's third largest exporter of rice, the condition of that production remains uncertain. Much of that rice will likely need to be consumed domestically, thus limiting rice exports.

We need to acknowledge some realities of Agri-Food. The world does not have as much Agri-Food as many believe. In less than a month without wheat production somewhere in the world, shortages would develop. Given the current situation, wheat shortages are possible at the beginning of the new year. Second, while technology can enhance Agri-Food production, it cannot make wheat grow without water. Third, the iPad is cool, but it cannot produce food.

At what price will wheat sell in ten years? Is US$18 a bushel possible? Corn perhaps at $11? In a price inelastic world such as is now the case for Agri-Food, prices will be far higher than historical precedent suggests. Many remain mired in the eras of bounty now part of history. Let your thinking become freer by reading The Joy of Agri-Food Price Inelasticity. Perhaps then you will be able to feed your family when palm oil is US$2,100 a ton and eggs are US$2.50 a dozen at wholesale.

AGRI-FOOD THOUGHTS is from Ned W. Schmidt,CFA,CEBS, publisher of The Agri-Food Value View, a monthly exploration of the Agri-Food grand cycle being created by China, India, and Eco-energy. To contract Ned or to learn more, use this link: www.agrifoodvalueview.com