An article by J.W. Jones

Last week's articles focused specifically on the option Greek Theta. This week we will shift gears and adjust our focus on Delta, another fundamental tenet of option trading. The official definition of Delta as provided by Wikipedia is as follows:

Δ, Delta - Measures the rate of change of option value with respect to changes in the underlying asset's price.

Delta has a significant impact on the price of an option contract(s). When a trader is long a call contract, Delta will always be positive. Likewise, if an option trader owns a put contract long, Delta will always be negative. As option contracts get closer to the money their Delta increases causing the option contract to rise in value rapidly as the option gets closer to being in the money.

Clearly Theta has an adverse impact on a trader who is long a single options position (own options long with no hedge or spread), however Delta is extremely dynamic and is one of the major factors directly responsible for option pricing as the price of the underlying changes throughout the trading day.

If an option is deep in the money, the option contract will have a higher Delta and will generally act similarly to actually owning the individual stock. For a deep in-the-money GLD call that has a Delta of +.80, the first dollar GLD rises by then the value of the GLD call options increases by roughly $0.80 or $80.

If the delta is 0.80, this essentially means that the GLD call option will increase in value 0.80 ($80) for every $1 that the GLD ETF increases. As the GLD option goes deeper into the money, the Delta will typically rise until it nearly produces the same gains as the GLD ETF until the delta asymptotically approaches 1.00 and the option moves in lockstep with the underlying. While my next article will continue to help explain Delta, it is important to understand how Delta can enhance a trader's return when trading options with a specific directional bias.

While options exist for the gold futures contract, typically if I want to trade gold I utilize the GLD ETF. The primary reason is that the ETF offers liquid options, which makes it easier to initiate spreads and multi-legged orders. If options are thinly traded, the bid ask spread is almost always wide making it more difficult to get a good fill and a good overall price. Most option traders stay away from underlying stocks that have illiquid options.

In order to better illustrate how an options' Delta can create profits, I will use GLD as an example. Keep in mind, I am not advising any traders to buy or sell options naked. I only trade options using strategies that help mitigate various risks to my capital. Theta (time) risk, volatility risk, and market risk are not being considered as this is merely an example to illustrate the power of Delta.

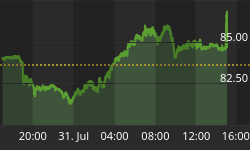

Recently Gold and subsequently GLD suffered a pretty significant pullback. GLD broke down through a major horizontal trend line and the daily chart was extremely bearish. Just when a lot of traders were preparing to get short GLD, buyers stepped in and pushed GLD's price back above the support area. The GLD daily chart listed below illustrates the breakdown and subsequent failure and a powerful rally followed.

Let us assume for contrast that an option trader and an equity trader each wantto get long GLD. The equity trader buys 200 shares of GLD at $115/share. Assumingthe equity trader does not use margin, the total trade would cost around $23,000not including commissions. The option trader decides to utilize delta and purchases5 October 107 calls which in our example cost $900 per contract for a grand totalof $4,500 not including commissions.

We will assume the October 107 calls have a Delta of 1.00. When a call optionhas a delta of 1.00, it essentially means that the owner of the call is goingto get 100% of the move reflected in the premium of the option he/she owns. Thusif GLD increases by $1, the value of the option would increase $1 all thingsbeing held constant.

This is where Delta really shines; it shines even brighter than gold in thisillustration. Both the equity trader and the option trader have a profit targetof $118/share. A few days later GLD reaches $118/share and both traders closetheir trades with profits. The equity trader made $3/share which relates to atotal gain of $600, or around 2.60%.

The option trader realized roughly 95% of the move, meaning around $2.85. Theoption trader had five total contracts for a total gain of $1,425 less commissions.The total gain for the options trader was over 31% less commissions.

Keep in mind, the option trader only had $4,500 of maximum risk while the equity trader was risking over $20,000. The option trader made over 100% more money, while risking only 25% of the total capital required by the equity trader. Behold, the power of Delta!

Learn more about how to find low risk options trades and get our alertsat: www.OptionsTradingSignals.com

J.W. Jones is an independent options trader using multiple forms of analysisto guide his option trading strategies. Jones has an extensive background inportfolio analysis and analytics as well as risk analysis. J.W. strives to reachtraders that are missing opportunities trading options and commits to writingcontent which is not only educational, but entertaining as well. Regular readerswill develop the knowledge and skills to trade options competently over time.Jones focuses on writing spreads in situations where risk is clearly definedand high potential returns can be realized.