The following is commentary that originally appeared at Treasure Chests for the benefit of subscribers on Wednesday, August 11th, 2010.

The fear of God - or the perception of power - this is the primary tool of the Fed these days. It's not credibility anymore, as this has been damaged to the same extent as its balance sheet. This is widely understood as a primary fundamental within the larger scheme of things in that the dollar ($) is the world's primary reserve currency, where expectations associated with renewed Quantitative Easing (QE) is common place, and now talk of hyperinflation is growing amongst the more plugged in market observers. And it's this that accounts for the growing and extreme bearishness amongst speculators concerning the $.

The thing most speculators / market observers can't figure out about the above however is that the Fed, being center in the larger price managing bureaucracy, uses the above understanding(s), in that bearish sentiment in $ related betting markets (think derivatives, ETF's, etc.) will support its price, which in turn will aid in dampening demand for precious metals. That, ladies and gentlemen, is the whole idea around Fed meetings these days - to confuse the heck out of people and keep the traders on edge. This in turn allows the Fed to carry on in its price managing ways until the sentiment loop becomes exhausted.

And as far as the $ is concerned, speculators are betting to the extreme (see Figure 12) that a bounce is immanent, making such a reality unlikely until after ETF options expiry next week (UUP is the bullish $ ETF), even if the Fed does not follow through on the market's expectations of QE II. So, this should make for some increasing volatility in coming days (which is happening already today), however again, don't expect something big and lasting until post options expiry on the 20th. After that, and especially if as mentioned Monday, the high yielding (risky) bonds brokers and hedge funds have been riding (with all the liquidity flowing into the bond bubble of late) are leading down, which happens to already be the case, expect volatility to pick up as we enter September. (i.e. in addition to high yielding bonds leading lower, especially if open interest put / call ratios make direction changes.)

Speaking of which, you likely noticed US index open index put / call ratio plots were updated here yesterday to assess sentiment given this volatility. Because if the S&P 500 (SPX) breaks 1110 today, it would breach a trend-line extending back to last month's lows, raising the specter normally supportive sentiment based drivers have become ineffective is controlling price direction(s). I see SPX futures are already suggesting the cash market will open below this level, however again, it's difficult envisioning a rout in stocks developing as we move into options expiry even though it appears the Fed is now completely impotent in that put / call ratio profiles for US stock indexes, the CBOE Volatility Index (VIX), high yielding bonds (HYG), and the $ are not supportive of such an outcome.

As a matter of fact, and ignoring the fundamentals for now, the overnight price action is quite surprising given the Fed's pledge to monetize bonds increasingly yesterday, this and the sentiment picture running into expiry next week. Previously, this kind of picture would have yielded quite a different result, which is likely a legitimate shot across our collective bow(s) that it's different this time, and that the effects of the buyers strike on Wall Street are about to come home. (i.e. the nightmare has now arrive for the larger bureaucracy.) It's either that or the bureaucracy's price managers don't like the fact it looks like gold and silver are about to bust a move higher and they are allowing stocks to fall in order to keep people thinking deflation.

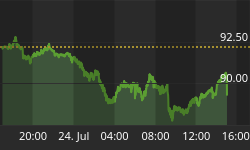

Leaving conspiracy theories aside for now however, in spite of all this from a technical perspective the VIX is poised to rally (and stocks to plunge), which would be the natural path at the moment. (See Figure 1)

Figure 1

So, if I had to guess on what will transpire between now and options expiry the 20th, although we could have a trend break in stocks here, next week should still prove to be market(s) friendly towards equities, with a testing process associated with breaks this week being the result. And who knows, perhaps the breaks won't even last the day, making all such talk moot. Such an outcome would not be surprising considering yesterday's price action in high yield bonds, where although cycle influences have rolled over (MACD, etc.), prices remain buoyant. (See Figure 2)

Figure 2

Of course when one looks at the matrix behind the scenes (ratios) the picture appears quite different. And although one could not aggressively bet on the head and shoulders pattern in the trade breaking lower in the iShares iBoxx High Yield Corporate Bond Fund (HYG) / iShares iBoxx Investment Grade Corporate Bond Fund (LQD) Ratio seen below, based on the way stock futures are dropping this morning, who knows, it could happen anyway. (See Figure 3)

Figure 3

But that's the way these price managers work. They see gold and silver are about to break out and take the larger equity complex down to prevent this via a deflation scare. Then, when they think they have the market(s) sufficiently rattled, magically (think short squeeze), a bid comes back into stocks like nothing ever happened, which again, is likely what we will see next week. After expiry next week, if stocks turn down on their own, then price managers will worry about not allowing things to fall off a cliff after gold and silver have been smashed lower. This tactic, along with other elements of the price suppression scheme, has been the bureaucracy's modus operandi in keeping precious metals prices under control for some time now. Too bad for them physical supplies are now running out fast with the larger system about to implode, no?

Unfortunately we cannot carry on past this point, as the remainder of this analysis is reserved for our subscribers. Of course if the above is the kind of analysis you are looking for this is easily remedied by visiting our web site to discover more about how our service can help you in not only this regard, but also in achieving your financial goals. As you will find, our recently reconstructed site includes such improvements as automated subscriptions, improvements to trend identifying / professionally annotated charts, to the more detailed quote pages exclusively designed for independent investors who like to stay on top of things. Here, in addition to improving our advisory service, our aim is to also provide a resource center, one where you have access to well presented 'key' information concerning the markets we cover.

And if you are interested in finding out more about how our advisory service would have kept you on the right side of the equity and precious metals markets these past years, please take some time to review a publicly available and extensive archive located here, where you will find our track record speaks for itself.

Naturally if you have any questions, comments, or criticisms regarding the above, please feel free to drop us a line. We very much enjoy hearing from you on these matters.

Good investing all.