Stocks took it on the chin on Tuesday, the extended position being exposed by a couple of fairly innocuous developments.

Bank of America reported a $7.3bln loss for the quarter, rather worse than expected. But don't worry! Since the reported P/E of the S&P these days is usually shown ex-companies-with-losses (except for the number reported in Barron's, which still calculates it properly), this won't make the S&P look more expensive. BOA made $3.1bln before a $10.4bln 'one time' write-down of goodwill due to recently-enacted laws that (according to Bloomberg) could slash debit-card revenue as much as 80%. It seems to me that if they didn't see this one coming, it's hard to believe they know it's a one-time charge. Both barrels of the legislature are trained on the banking sector, and sometimes they hit.

That news set stocks back in the pre-open hours, as did Apple's guidance (after announcing a solid 'beat' today) that they would miss analysts' expectations in the current quarter. These are hardly watershed events, but negative enough considering how far the market has come recently.

Housing Starts surprised on the high side, with 610k units (annual pace) being started last month. But the chart (see below) gives the proper context - this is hardly earth-shattering news either. The new construction part of the market isn't the part that still needs to normalize: that would be the overhang of existing homes. But as long as 'Starts stay low like this, it helps to reduce the total stock of housing for sale (new and existing) and that will eventually heal the housing market. Not this year, but eventually!

The recovery is 'L-shaped' in Housing Starts, at least.

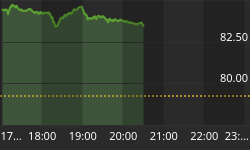

Stocks spent the first half of the day shaking off the overnight weakness, or trying to, but then took a big leg lower when Dallas Fed President Fisher said that the Fed's "debate on possible easing may not be completed in November." See how much of the market's ebullience is based on the greater-fool theory that the Fed will be flushing free money into the system to push asset markets higher? But Fisher simply hasn't gotten the memo. He is correct that the debate will not be completed in November; for all intents and purposes it was completed in October. Chicago Fed President Evans, just today, was discussing how the Fed needs "large purchases" to get inflation's behavior to be what they want it to be. NY Fed President Dudley also supported that notion today. And they are hardly alone. Fisher may be trying to throw down the gauntlet, but all that really needs to be decided is whether there are two dissents or only one. Let's just say that if the Fed does not actually initiate QE2, the whole "transparent communication" policy needs to be re-thunk because there is a pretty strong consensus right now that QE2 is coming and no dovish Fed official is doing anything to discourage that notion. (Regular readers will know that I favor more opacity, but if you're going to say you're transparent you'd better actually be transparent. The double-agent routine would deliver a crushing blow to markets).

After the Fisher bombshell (which, as I say, isn't really much of a bombshell because we knew where he stood), stocks never really could recover very much. Bonds ended higher, with the 10y yield down to 2.47%, but bond folks know how to read the Fed chatter and probably realize this doesn't signal that the Fed is backing off at the last minute.

A late rally cut the S&P's loss to -1.6%. The dollar streaked higher, and commodities were set back hard. Inflation-linked swaps declined 1-4bps. All in all, it was a rough day for trend-followers.

On Wednesday, regional Fed Presidents Plosser and Lacker will both be speaking (in addition to the speakers still remaining today). The Beige Book will be released. And there are more earnings announcements. It remains to be seen if today's technical damage, more than the events themselves, is enough to make investors somewhat wary to push prices back to their recent extremes.