In our "roadmap for the next couple of weeks", I stated that the market dynamics appear to be changing. I sense that yesterday's price action is beginning to confirm for investors what I have been seeing on the charts for about a week now.

The markets are overbought and there are too many bulls, and under this set of conditions, a pullback is not only expected, but it should be welcomed by the bulls. The markets are going to need more fuel to avoid a lower high or the "dreaded" double top. Market momentum is on the wane and has been so for a couple of weeks. See figure 1, a weekly chart of the S&P Depository Receipts (symbol: SPY), to see a double top or lower high in the works.

Figure 1. SPY/ weekly

The biggest conundrum (from this vantage point) appears to be longer term interest rates. Yields on the 30 year Treasury really haven't followed yields on the 10 year Treasury lower. Yields on the 10 year Treasury are approaching the December, 2008 crisis lows while yields on the 30 year Treasury are far from those levels. This can be seen in figure 2, a weekly chart comparing the 30 year Treasury yield (symbol: $TYX.X, upper panel) to the 10 year Treasury yield (symbol: $TNX.X, middle panel). The indicator in the lower panel of figure 2 measures the difference between the 30 year yield and the 10 yield, and what is noted is that this spread is the highest value in a generation.

Figure 2. 30 year Treasury yield v. 10 year Treasury yield/ weekly

Once again, the 30 year yield is not following the 10 year yield lower. Like any divergence, this is noteworthy and begs the question: What does it mean, if anything?

The persistence of the 30 year Treasury yield to stay elevated (relative to the 10 year) could be due to two factors. One, market participates are anticipating inflationary pressures, which will likely be seen years down the road as a by-product of current Federal Reserve monetary policy. Two, QE2 may not be as large (initially) or even involve buying of Treasury bonds at the long of the end curve as many market participants originally anticipated. These events have yet to occur, so we must assume (rightly or wrongly) that the market is anticipating higher yields. There is one factor that appears to be off table as to why longer term yields are rising. Yields are not rising in response to a booming economy. Most would agree that growth will remain muted to weak for the foreseeable future.

From this perspective - the technical one that is -, longer term Treasury yields have found a bottom. Figure 3 is a weekly chart of the Ultra Short Lehman 20 + Treasury Fund (symbol: TBT). This 2x leveraged ETF product moves in the direction Treasury yields or inverse to bond prices. This is a bullish price pattern indicating a bottom as prices on the TBT are now firmly above the key pivot point at 31.93.

Figure 3. TBT/ weekly

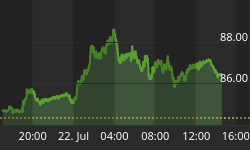

How far will TBT go? Resistance is at 36.26. Is this the "once in a lifetime" trade we heard about back in the Spring of 2010 when it was widely assumed that yields could only go up and go up big time? At this point, my guess - and it is only a guess albeit an informed one - is that this is not that time.