Prices - on website - http://www.authenticmoney.com/subscribe.htm

Contact us at - goldauthenticmoney@iafrica.com

· Send for Free Sample Copy of "GoldAuthenticMoney" ??

· Special Offer!: - Do you want to receive your own copyof "Gold - The Weekly Global Perspective" direct to you? - Sendemail address to: goldauthenticmoney@iafrica.com

"Gold - The Weekly Global Perspective" is not written so as to give you guidance on the Gold, Silver or Platinum prices. It is an informed commentary on the events that reached the market since the last issue. For price guidance and the FULL picture of the markets, with perspectives and insights, see below for details of these publications.

That was the week that was!

Since our last issue when gold stood at $407 and the Euro at $1.2344, not much seems to have happened, or has it? Gold is around $406, but the Euro has weakened by 2%. Oil has seemingly peaked, or is this the weight of wishes making it seem that the $2 fall was a real weakening? Little has changed, as one can see when you sweep the emotions out of the way. But the fall in the Euro and the seeming stability in the $ price of gold tells you what? Linked to oil? The funds may use that as a reason for the weekly stampede on Friday, to push the price down? But few see a direct link between gold and oil. No, the link comes as a symptom of the darkening of the clouds of uncertainty over the markets, whether they be the Dow, or oil, or the U.S. economy, or the Euro or the $. For the myopic, life can be confusing, but for those prepared to put their emotions to one side, their spectacles on, to get the longer view, the darkening of the clouds is symptomatic of a change of current, of seasons. The superficial calm in the markets belie some deep seated fundamentals rising to bring major changes to the gold market as efficiently as "El Nino" brings global weather changes. Do you understand what these are?

The Funds were back in the market again, which remained out of season and thin, jolted this way and back by well worn news on the Euro, Terror, and underwhelming economic news from the States. But their presence was neither significant nor adventurous as they too, wait for the Trade winds to blow again. After yet another "Frantic Friday" last week [and we could get another this week], in which we saw the gold price lurch up in $, to the mid teens above $400, this week saw it subside down to below $405, but not convincingly. It then seemed to rise to the steady, current level.

We are still waiting for the market to come back into season. The news from the holiday resorts is that the suntans have reached "I could be a local" level and most have learned the most important sentence in the local language ["Two beers please and my friend is paying"] and thoughts of home are beginning to appeal. Next week will see the long journey home then back to work, with eyes focussed on the high season for gold.

The Indian harvest, looking much better now, will be coming in. So, with prices at steady and tested levels, the pulse of the market will quicken.

Will you make it happen or will it happen to you?

Short term prospects for the price:

A thin, easily startled market, is what we see, waiting to be led or stampeded. We see a market used to being dominated by New York, with all eyes on the $ and the U.S. economy. When the other, huge, fundamentals kick in, they are likely to take the market back to Europe with the U.S. following. With the funds preferring to be passengers at the moment, the fundamentals should dominate and give direction. These are as strong as we have ever seen them, but never more misunderstood by the market than now. Under the dark skies of uncertainty, the 'surf' can be whipped up in a flash, catching all, but the informed, by surprise. The informed will act soon. But which way will the market go now and how far? We give the Technical picture and action instructions in "Changing Tack" and "Changing Tack Gold & Precious Metal Shares" We detail the changing fundamentals in "Gold -Authentic Money" in full. We specialise in the broad spectrum of gold market forces and what drives the gold price. These are the publications you need to do so too [details below].

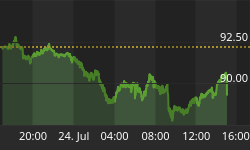

At the time of writing gold stood at $405.65 and Euros 335.66. The Euro itself is worth $1.2085.

Large Scale Speculators.

The total net long speculative position amounted to 270 tonnes, before last Friday's surge of buying took it up another 40 to 70 tonnes. The speculative activity is still muted, at half the level of last years herd like activity and should remain so. This week saw some unwinding of their positions as the gold price failed to follow through to higher levels and left them exposed at the front of the price charge. We do not expect them to act any differently, near term, until someone else leads the charge and for better reasons. Some say they are heavily short of the market as they feel it will drop substantially. We don't say that.

The Euro, just another currency?

Perhaps the most significant market event in the last week, has been a significant break between the Euro and Gold. Now 10 Euros higher than a couple of weeks ago, we note the market recognition, at last, that Gold is not a Euro related currency. The Euro, alongside other international currencies has no interest in weakening its competitive position in the international markets. It does want stability in Euroland, but not a trade weakening strength in the exchange rate. Is this a trade off in the integrity and insularity of the Euro, against its role in global trade. Yes, and it had to happen, because there is no territorially linked currency that can act as a global currency, without the interference of internal national interests. A currency must also reflect its global trade position, but not reflect any concept of intrinsic value. As such, this "conflict of interests" disqualifies any currency from holding such a role!

The impartial maintenance of value, is a role better suited to Gold, particularly when global economic clouds darken! In addition, gold can rise in price far further than a currency, trying not to rise to hold trade advantages. As such a far better investment? In the right setting it can be a vital support for currencies!

Argentina buys Gold

South America has a history of currency disasters, of inabilities to repay debt, of excessive inflation, for "Dollar Standards" that failed. $ savings have been reduced by 40% when confiscated by government authorities, in exchange for Pesos. What has particularly rubbed the South American authorities has been the fixing of their currencies to the $, only to find the incompatibility of their currency to the $ led to a breakdown of the system. The purchase of 42 tonnes of gold by Argentina is not to be seen as a capricious act by a rebellious nation, but an act of a nation that desperately seeks to hold what it can in an asset that "will counter the swings in the $" and any local currency crisis, as well as represent a wise reserve asset that can give a measure of credibility to a South American currency.

Argentina's move represents a significant move forward by any nation outside the States. It should be seen as a move being carefully watched by other nations, faced not only with an uncertain $, but a nation reaching out for at least a small measure of independence from the overwhelming presence of the $ in international money. The control the States can exert on the value of the $, is one that removes the control over the value of foreign governments reserves [of $s]. This should not be the case where gold is that reserve. Taken in the context of global discussions on the composition of monetary reserves going on at the moment, this is a definite step forward for gold in that system. This is to be discussed further in "Gold - Authentic Money" in the next issue, as it is a vital subject for the future of monetary gold.

World Gold Council report on the first half of 2004.

The World Gold Council report for the first half of 2004 contains the elements which will lead the way in the gold market for the second half of the year. The mixture of these will precipitate a very different market for the last quarter of the year, than seen in the previous three quarters. The full picture is contained in the next issue of "Gold - Authentic Money".

The U.S. Recovery.

The statistics released since our last issue did little to convince the markets that the recovery is vigorous. It will probably prove self sustaining, but at lower levels and in uncertain conditions. This prospective "lacklustre" performance will not remove uncertainty.

The housing market appears to be peaking with the Commerce Department informing us that July new home sales slid to 6.4% to a 1.134 million annual rate, their slowest pace since December. Analysts had expected a 1.29 million pace. A key reason for this was the rise in the average rate on a 30year conventional mortgage to 6.06% in July, up from a low of 5.23% in June 2003.

Orders for longlasting goods gained 1.7% in July, the Commerce Department said. But orders other than transportation were up only 0.1%. As a result, the indications are that growth is slowing. On the other hand the lower inflation rate, in itself, effectively makes interest rates a bit more 'real', giving more confidence to the market, but for how long?

Generally, fewer and fewer people are confident that growth is as portrayed by Greenspan, of late. The fact that Greenspan alluded to the oil price as being detrimental to the U.S. recovery at all, has brought the oil price to centre stage and is being read as a major influence over the economy.

The Oil price.

The fact that not only are supplies from oil producers reaching full capacity, but also refining capacity is over 90% utilised, worldwide, shows that the demand / supply balance in the oil industry has reached critical and possibly destabilising levels.

The oil price, although it dropped slightly, is a pernicious influence on growth. Resumption of supplies from Iraq and reassurances from the Russian governments that interruptions in their supply of oil to the market, calmed the market slightly, but the underlying strong demand ensured that the prices are staying far higher than expected. With the likelihood that prices will stay high for many years to come, any dip in the oil price has to be seen, by all, as a "buying" opportunity.

The gold price, whilst not linked to oil, reflects the uncertainty the oil price brings to the global economic prospects. The oil price does reflect the buying power of the $, which is felt every time one goes to the pump. And this is only reasonable as this is an oil driven world still. The possibility of alternatives, the prospects for greater supplies, or any other eventual possibilities are irrelevant, at the moment. The reality is that this situation is now and unlikely to change in the short or medium term, so should continue to hurt us all. Its effects will spread to other sectors as it feeds through to the economies of the world. There is no doubt that, as in the past , these prices will precipitate inflation as all try to defend their profits and so raise prices. Central Bankers are not worried, feeling that when prices cross $70 or $80, only then will we could see a recession or worse. This is disturbing, because it makes it either inevitable or uncontrollable and probably both!

More Good news for South African Miners!

Inflation is dropping quite rapidly in South Africa, according to government figures to the bottom end of the 3% -6% of their inflation targets. This will have the effect of making the current level of interest rates more "real". The recent drop in the Prime rate of 0.5% could well be followed by more drops. Hopefully the next drop will be a full 100 basis points to take Prime to 10%. In turn, this may well take the Rand back below R7 :$1. But still more will be required before South Africa's export industries are back in the peak of condition.

Sad to say, it seems unlikely that this will be enough to reverse the mining industries policy of diversifying into other countries. It will take a policy that is friendly, profitable and encouraging to Miners, to bring them back. What a price to pay in jobs, for such myopia. In a country so small, the job losses in the hundreds of thousands are unaffordable.

But in terms of the drop in gold produced by South Africa, the gold price will benefit, eventually.

A strike has been called at two more Platinum mines for more wages, above the inflation level [see below]. Oh Africa!

Silver $6.62

Silver speculators reflected the performance of the metal and dropped the total speculative long position in Silver to 331 million ounces, not a lot, but showing that the metal is becoming the poor relation of the three. Still vulnerable!

Platinum $855

Strikes are threatened at Impala Platinum and Northam, in addition to Anglo American Platinum (Angloplat). The three firms account for over half of the world's production of platinum, with output of around 3,5million ounces last year, compared to world production of 6,1million ounces. At Angloplat management offered a 4,7% increase. Angloplat and other mining companies, pressured by a strong rand that cuts export income, have warned workers not to expect wage hikes much above inflation. Angloplat is in the midst of a costcutting programme and has vowed to keep unit cost increases in line with inflation this year. The union has demanded 15% wage increases at Angloplat and Northam, but the platinum companies have only offered between 4,7% and 6,5%. The Implats talks concern the second year of a twoyear wage deal agreed last year, which stipulated a wage hike of 1,5 percentage points over headline inflation, which is currently running at 5%. The deal had a provision for either side to reopen talks if that would lead to an increase of lower than 7,5% or higher than 9%. The company is offering 6,5%, while the union is seeking 8,5%. It is the constant abrasion brought by these types of demands, taxation and a strong Rand that is undermining the future of the mining industry.

It is no wonder that the total speculative long position in Platinum rose to 178,000 last week. The price now has a measure of added strength with a potential rupture in supplies. The metal is looking more attractive than the shares at the moment for sure, for short term Traders?

The London Gold Fix Gold

26th August a.m. $405.95 E 336.413

26th August p.m. $406.05 E 336.468

Gold moving up and away from the Euro now?

Testimonials - "I must say that I am very impressed with the efforts that you go to both in your publications and your one to one attention." - " Being a relatively new subscriber, I want to congratulate you on giving the exit (commonly referred as "stop loss" exit) price on your recommended trades. One famous trader was interviewed many years ago. He was asked what he accredited his success in trading to? His response, "great defense". Knowing when to exit a bad trade. That is the key to trading success. I am glad to see you putting that in your recommendations - without that, small losses become big losses. Congratulations."

- "I find your technical analysis of the Dow very useful to me and since the markets seem correlated anyways... ... As always, continue the great work."

Our services: -

1. "GoldAuthentic Money" - Macroeconomic and gold market reports - Important articles on facets of gold - Gold and Silver Technical Analysis - Medium and Long Term. - Approx Bi Monthly

2. "Changing Tack - Gold & Precious Metal Shares." - Gold & Silver Technical Analysis - Short term. Share Prices, Company information - " Comparative Performance Model" - shows shares that will lag and those that will lead. - Weekly

3. "Changing Tack" - Gold & Silver Technical Analysis - [ Same as above - without the share service] - Weekly

Discount Prices - on website http://www.authenticmoney.com/subscribe.htm

Contact us at goldauthenticmoney@iafrica.com