As the global economy shows continued signs of a sustainable economic recovery, there are two notable areas lagging behind; employment and housing in the United States. Continued trends in these areas could lead to renewed weakness in the U.S. dollar, which in turn could help boost stock and commodity prices. From a December 26th Bloomberg article:

A wave of foreclosures waiting to reach the market means home prices will remain under pressure in 2011, representing a risk to household finances. Rising equity values and an improving job market will probably help offset the damage, ensuring that confidence and spending continue to climb. "The inventory overhang is so big, with foreclosures looming, it'll take five years to absorb the supply," said Paul Ballew, chief economist at Nationwide Mutual Insurance Co. in Columbus, Ohio. "The consumer is feeling better although there is still a high level of caution and anxiety."

According to a December 29th NPR article:

Mark Zandi, chief economist at Moody's Analytics, says in 2010 the labor market was running hard, but going nowhere. The economy needs to generate about 150,000 jobs a month, Zandi says, just to keep up with population growth and people re-entering the workforce. It didn't do that in 2010. "It wasn't negative. We weren't hemorrhaging jobs," he says. "But in the context of 10 percent unemployment, standing still isn't all that great."

In general, a weak U.S. dollar is favorable to stocks and commodities, with the benefit of the doubt going to stocks in emerging Asian countries since their debt burdens are small relative to developed nations. The short-term outlook for the U.S. dollar is somewhat mixed presently with the bulls having the upper hand over the last seven weeks. Recent action in the U.S. dollar, aided by growing concerns about ongoing weakness in housing, has left the door ajar for the dollar bears. The dollar is also under assault from the Fed's quantitative easing program (a.k.a. money printing).

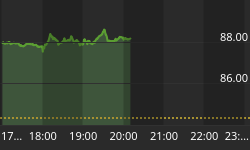

On December 17th, we noted the dollar had recently completed two of the three steps usually associated with a change in trend. As shown in the chart below, the dollar has been unable, thus far, to complete the third step, which is to close above 81.19. Recently, the dollar has made a lower high, which leans bearish (compare point A to point B). The Rate of Change (ROC - see bottom) indicator also tells us the recent push higher was lacking conviction from buyers (compare A1 to A2 below). As of the close on December 30th, nothing was settled from a very short-term perspective.

For now, the dollar sits in a technical no man's-land from a short-term perspective. A close below 79.29 would increase the odds of a resumption of the greenback's longer-term downtrend. Should the bears regain control of the dollar, it would continue to favor commodities such as copper (JJC), silver (SLV), oil (USO), and agriculture (DBA). Significant weakness in the dollar may be followed by a resumption of leadership by emerging market stocks (EEM) relative to U.S. stocks (SPY).

With a six-to-twelve month time horizon, favored sectors for 2011 include energy (XLE) and materials (XLB). Strength in these sectors tends to be associated with periods of weakness in the U.S. dollar. From a bullish perspective, we could see strength in energy and materials, coupled with strength in the dollar, if U.S. growth, housing, and/or employment surprise on the upside, but that may be an ambitious scenario. Our 2011 outlook for stocks does not rule out better than expected economic outcomes in the first of 2011, based on recent technical deveopments.

We will continue to monitor the U.S. housing and labor markets along with relative moves in global currencies. Markets have a lot of moving parts; keeping an open mind, paying attention, and remaining very flexible are sound practices for all investors.