The good news is:

• The blue chip averages hit multi year highs last week and the NYSE AD line hit an all time high on Friday.

According to MARKET BREADTH INDICATORS by Gregory L. Morris the Advance - Decline Line (ADL) (a running total of declining issues subtracted from advancing issues) was created by Leonard P. Ayres and James Hughes in 1926. The concept had been alluded to by Charles Dow in 1900.

The theory is the ADL represents the broader market while the indices are usually over weighted with blue chips. Attention should be given when the major indices diverge from the AD lines.

The chart below covers the past year showing the S&P 500 (SPX) in red and the NYSE ADL in blue. The NYSE ADL closed at an all time high last Friday. Dashed vertical lines have been drawn on the 1st trading day of each month.

The next chart is similar to the one above except it covers the past 50 years. Dashed vertical lines have been drawn on the 1st trading day of each year.

Until about 10 years ago the NYSE ADL had a negative bias, but that has changed to an extremely positive bias. The parameters for using this indicator need to be adjusted for this change.

The chart below covers the past 35 years showing the NASDAQ composite (OTC) in blue and an AD line calculated from NASDAQ issues (OTC ADL) in green.

The OTC ADL has always had a somewhat negative bias, but that negative bias appears to have strengthened in the past 10 years.

Since the mid 1980's the number of fixed income issues traded on the NYSE has been increasing. Currently about half of the issues traded on the NYSE are fixed income related (bond funds and preferred). If interest rates remain constant, fixed income issues should accumulate value daily until they go ex dividend; usually monthly or quarterly. This would give them an extremely positive bias.

FastTrack (FastTrack.net) maintains a database of 72 corporate bond funds.

The chart below covers the past 20 years showing an index of those funds in red and an ADL calculated from those funds in black.

This chart is the opposite of what I expected.

From April 1915 through April 2002 Dow Jones published 3 bond indices with advance decline and new high new low data. An AD line calculated from that data had an extremely positive bias. I do not understand why bond funds would be different.

FastTrack also maintains a database of 199 high yield bond funds (AKA JUNK). The chart below is similar to the one above except the index in red and the ADL in black have been calculated from the high yield database.

The Junk ADL appears to have a more positive bias than the non-Junk ADL.

The lesson to be gained is indicators calculated from data streams can vary widely must be studied individually.

The negatives

The chart below covers the past year showing the SPX in red and a 10% trend (19 day EMA) of NYSE new highs (NY NH) in green. Dashed vertical lines have been drawn on the 1st trading day of each month.

NY NH has been trending lower while the SPX was up 6.6% in December.

The next chart is similar to the one above except it shows the NASDAQ composite (OTC) in blue and OTC NH has been calculated from NASDAQ data. OTC NH fell sharply last week while the index was down modestly.

The positives

New highs declined last week, but so did new lows.

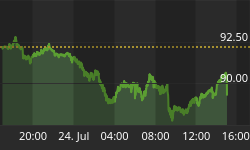

The chart below covers the past year showing the OTC in blue and 40% trend (4 day EMA) of the ratio of NASDAQ new highs to new highs + new lows (OTC HL Ratio) in red.

The value of the indicator on Friday was 90%. There are trading systems that impose a no sell filter when variations of this indicator are above 80%.

The next chart is similar to the one above except is shows the SPX in red and NY HL Ratio, in black, has been calculated from NYSE data.

NY HL Ratio closed on Friday at 94%.

The strong positive seasonal bias of the last 2 weeks makes any analysis of the period questionable.

Seasonality

Next week includes the first 5 trading days of January during the 3rd year of the Presidential Cycle.

The tables below show the return on a percentage basis for the first 5 trading days of January during the 3rd year of the Presidential Cycle. OTC data covers the period from 1963 - 2009 and SPX data from 1929 - 2009. There are summaries for both the 3rd year of the Presidential Cycle and all years combined.

Returns by all measures have been extraordinarily positive.

Report includes the first 5 days of January.

The number following the year represents its position in the presidential cycle.

The number following the daily return represents the day of the week;

1 = Monday, 2 = Tuesday etc.

| OTC Presidential Year 3 | ||||||

| Day1 | Day2 | Day3 | Day4 | Day5 | Totals | |

| 1967-3 | 0.41% 2 | -0.04% 3 | 0.92% 4 | 1.02% 5 | 0.76% 1 | 3.08% |

| 1971-3 | 0.35% 1 | -0.87% 2 | 0.66% 3 | 0.78% 4 | 0.28% 5 | 1.20% |

| 1975-3 | 1.47% 4 | 0.87% 5 | 0.83% 1 | 0.24% 2 | -0.63% 3 | 2.79% |

| 1979-3 | -0.12% 2 | 1.08% 3 | 1.30% 4 | 1.15% 5 | -0.11% 1 | 3.31% |

| 1983-3 | -0.78% 1 | 0.46% 2 | 0.51% 3 | 1.62% 4 | 0.84% 5 | 2.65% |

| 1987-3 | 1.27% 5 | 2.24% 1 | 1.34% 2 | 1.77% 3 | 1.36% 4 | 7.98% |

| Avg | 0.44% | 0.76% | 0.93% | 1.11% | 0.35% | 3.58% |

| 1991-3 | -0.44% 3 | -1.26% 4 | -0.07% 5 | -1.91% 1 | -0.34% 2 | -4.02% |

| 1995-3 | -1.11% 2 | 0.30% 3 | -0.02% 4 | 0.54% 5 | 0.32% 1 | 0.03% |

| 1999-3 | 0.70% 1 | 1.96% 2 | 3.08% 3 | 0.24% 4 | 0.79% 5 | 6.76% |

| 2003-3 | 3.69% 4 | 0.16% 5 | 2.47% 1 | 0.72% 2 | -2.13% 3 | 4.91% |

| 2007-3 | 0.33% 3 | 1.25% 4 | -0.78% 5 | 0.16% 1 | 0.23% 2 | 1.19% |

| Avg | 0.63% | 0.48% | 0.93% | -0.05% | -0.23% | 1.77% |

| OTC summary for Presidential Year 3 1967 - 2007 | ||||||

| Averages | 0.52% | 0.56% | 0.93% | 0.58% | 0.12% | 2.71% |

| % Winners | 64% | 73% | 73% | 91% | 64% | 91% |

| MDD 1/8/1991 3.97% -- 1/8/2003 2.13% -- 1/3/1995 1.11% | ||||||

| OTC summary for all years 1963 - 2010 | ||||||

| Averages | 0.17% | 0.62% | 0.26% | -0.11% | 0.14% | 1.07% |

| % Winners | 59% | 70% | 62% | 62% | 60% | 68% |

| MDD 1/6/2000 9.78% -- 1/8/2001 8.44% -- 1/8/2008 7.98% | ||||||

| SPX Presidential Year 3 | ||||||

| Day1 | Day2 | Day3 | Day4 | Day5 | Totals | |

| 1931-3 | 3.32% 5 | 1.45% 6 | -0.93% 1 | 1.26% 2 | -0.25% 3 | 4.85% |

| 1935-3 | 0.11% 3 | 0.21% 4 | -0.21% 5 | 0.63% 6 | 0.10% 1 | 0.84% |

| 1939-3 | -0.98% 2 | 1.15% 3 | -1.28% 4 | 0.08% 5 | -1.15% 6 | -2.19% |

| 1943-3 | 0.72% 6 | 0.81% 1 | -0.20% 2 | -0.10% 3 | 0.20% 4 | 1.43% |

| 1947-3 | -0.65% 4 | 0.39% 5 | 0.26% 6 | 0.92% 1 | -0.78% 2 | 0.14% |

| Avg | 0.50% | 0.80% | -0.47% | 0.56% | -0.37% | 1.01% |

| 1951-3 | 1.76% 2 | -0.39% 3 | 0.87% 4 | 0.00% 5 | 0.05% 6 | 2.30% |

| 1955-3 | 2.14% 1 | -0.90% 2 | -2.47% 3 | -1.35% 4 | 0.83% 5 | -1.75% |

| 1959-3 | 0.42% 5 | 0.40% 1 | -0.13% 2 | -1.26% 3 | 0.93% 4 | 0.36% |

| 1963-3 | -0.65% 3 | 1.64% 4 | 0.64% 5 | -0.02% 1 | 0.97% 2 | 2.59% |

| 1967-3 | 0.06% 2 | 0.21% 3 | 1.30% 4 | 0.71% 5 | 0.77% 1 | 3.05% |

| Avg | 0.75% | 0.19% | 0.04% | -0.38% | 0.71% | 1.31% |

| 1971-3 | -1.09% 1 | 0.71% 2 | 0.60% 3 | 0.03% 4 | -0.21% 5 | 0.05% |

| 1975-3 | 2.44% 4 | 0.68% 5 | 0.51% 1 | -0.07% 2 | -1.38% 3 | 2.18% |

| 1979-3 | 0.65% 2 | 1.11% 3 | 0.80% 4 | 0.56% 5 | -0.33% 1 | 2.77% |

| 1983-3 | -1.64% 1 | 2.18% 2 | 0.43% 3 | 2.33% 4 | -0.06% 5 | 3.24% |

| 1987-3 | 1.77% 5 | 2.33% 1 | 0.23% 2 | 1.01% 3 | 0.76% 4 | 6.10% |

| Avg | 0.43% | 1.40% | 0.51% | 0.77% | -0.24% | 2.87% |

| 1991-3 | -1.14% 3 | -1.39% 4 | -0.28% 5 | -1.73% 1 | -0.17% 2 | -4.72% |

| 1995-3 | -0.03% 2 | 0.35% 3 | -0.08% 4 | 0.07% 5 | 0.03% 1 | 0.34% |

| 1999-3 | -0.09% 1 | 1.36% 2 | 2.21% 3 | -0.20% 4 | 0.43% 5 | 3.70% |

| 2003-3 | 3.32% 4 | -0.05% 5 | 2.25% 1 | -0.65% 2 | -1.41% 3 | 3.46% |

| 2007-3 | -0.12% 3 | 0.12% 4 | -0.61% 5 | 0.22% 1 | -0.05% 2 | -0.44% |

| Avg | 0.39% | 0.08% | 0.70% | -0.46% | -0.23% | 0.47% |

| SPX summary for Presidential Year 3 1931 - 2007 | ||||||

| Averages | 0.52% | 0.62% | 0.20% | 0.12% | -0.04% | 1.42% |

| % Winners | 55% | 80% | 55% | 55% | 50% | 80% |

| MDD 1/6/1955 4.65% -- 1/8/1991 4.64% -- 1/7/1939 2.34% | ||||||

| SPX summary for all years 1929 - 2010 | ||||||

| Averages | 0.06% | 0.52% | 0.00% | 0.09% | -0.13% | 0.53% |

| % Winners | 46% | 75% | 49% | 56% | 46% | 66% |

| MDD 1/5/1932 7.02% -- 1/8/1988 6.77% -- 1/8/2008 5.32% | ||||||

Money supply (M2)

The money supply chart was provided by Gordon Harms. Money supply growth continued on its elevated trend last week.

January

Since 1963, over all years the OTC, in January, has been up 64% of the time with an average gain of 2.8% making it the best month of the year. During the 3rd year of the Presidential Cycle January has been up 91% time with an average gain of 8.1%, the best month of the best year of the Presidential Cycle. The worst January ever, 2008 (-9.9%), the best 1999 (+14.3%)

The average month has 21 trading days. The chart below has been calculated by averaging the daily percentage change of the OTC for each of the 1st 11 trading days and each of the last 10. In months when there were more than 21 trading days some of the days in the middle were not counted. In months when there were less than 21 trading days some of the days in the middle of the month were counted twice. Dashed vertical lines have been drawn after the 1st trading day and at 5 trading day intervals after that. The line is solid on the 11th trading day, the dividing point.

The blue line shows the average of the OTC in January over all years since 1963 while the green line shows the average during the 3rd year of the Presidential Cycle.

Since 1928 the SPX has been up 64% of the time in January with an average gain of 1.2%. During the 3rd year of the Presidential Cycle the SPX has been up 85% of the time with an average gain of 3.5% making it the strongest month of the strongest year of the Presidential Cycle. The best ever January for the SPX was 1987 (+13.2%) the worst 2009 (-8.6%). The SPX has not been up in January since 2007, the last 3rd year.

The chart below is similar to the one above except it shows the daily performance over all years for the SPX in January in red and the performance during the 2nd year of the Presidential Cycle in cyan.

Since 1979 the Russell 2000 (R2K) has been up 56% of the time in January with an average gain of 1.7%. During the 3rd year of the Presidential Cycle the R2K has been up 75% of the time with an average gain of 4.1%. The best ever January for the R2K was 1985 (+13.1%), the worst 2009 (-11.2%). The R2K also has not been up in January since 2007.

The chart below is similar to those above except it shows the daily performance over all years of the R2K in January in black and the performance during the 3rd year of the Presidential Cycle in green.

Since 1885 the Dow Jones Industrial Average (DJIA) has been up 63% of the time in January with an average gain of 0.9%. During the 3rd year of the Presidential Cycle the DJIA has been up 71% of the time with an average gain of 2.3%. The best January ever for the DJIA 1976 up 14.4%, the worst 2009 (-8.8%)

The chart below is similar to those above except it shows the daily performance over all years of the DJIA in January in Magenta and the performance during the 3rd year of the Presidential Cycle in green.

Conclusion

The market is overbought and due for a correction, but seasonality is likely to dominate again next week.

I expect the major averages to be higher on Friday January 7 than they were on Friday December 31.

Last week the Blue chips were up slightly while the secondaries were down slightly so I am calling last weeks positive forecast a tie.

This report is free to anyone who wants it, so please tell your friends. They can sign up at: http://alphaim.net/signup.html. If it is not for you, reply with REMOVE in the subject line.

In his latest newsletter Jerry Minton looks at the idea that continuous exposure to stocks is the way to get the "average" long-term return of the market. If you are retired or about to retire, you will want to read "Unnecessary Risks" at www.alphaim.net and sign-up for Jerry's free bi-weekly newsletter.

Thank you,