We prepare to head into the long Martin Luther King Jr. Day weekend with some interesting data today and some even more interesting data tomorrow.

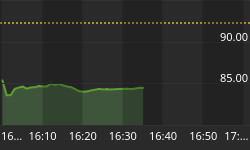

The report from the Labor Department that weekly initial claims for unemployment insurance rose to 445k versus expectations for 410k. Again we see that forecasters have gotten a bit too ebullient about the recent data. While our eyes tend to see on the chart (see below) a clear downtrend since August, statistically that downtrend isn't there - because in August, the true underlying level of Claims wasn't 500k, but more like 460k. Remember, these data are only samples of an underlying distribution that we cannot perceive directly. The spike in August tempted us to wonder if the second dip was beginning, but in fact it wasn't. The July dip was paid back by the August jump, while the underlying process remained fairly stable.

The horizontal lines indicate the previous presumed range.

It does appear, though, that we have enough data to suggest that the underlying pace of Claims has improved from the 440-480k range it had held for nearly a year, but consider how much we actually know about that improvement. This week's 445k figure was probably higher than it should have been because claims offices were catching up on last year's paperwork, so the last several weeks should be considered together. The 8-week average is at 420k, and I think that's probably a reasonable estimate of where we are. But if we have moved from a 440k-480k range to a distribution with 420k as the central tendency, that isn't so dramatic. The eye creates a trend here, but in fact all we can say is that the underling pace of Claims has moved from "about" 460k to "about" 420k over the last couple of months. That does not imply that further improvement is automatically in store. Remember - as if this week's data wasn't reminder enough - that late-year and early-year seasonal are extremely uncertain.

The number knocked a tiny bit of froth out of stocks...with an emphasis on a tiny bit. Prices recovered almost to unchanged, because that's what stock prices do these days, but bonds rallied and inflation swaps declined 4-5bps.

Looking over the Atlantic, ECB President Trichet offered what some observers saw as a threat that the ECB would raise interest rates to combat inflation if energy-price increases pass through to broad price increases. The German bond market, and others, sold off on his "conditional warning":

"We see evidence of short-term upward pressure on overall inflation, mainly owing to energy prices, but this has not so far affected our assessment that price developments will remain in line...Very close monitoring of price developments is warranted."

This is an empty threat. There is no chance that the ECB will raise rates to combat inflation while they are simultaneously buying every bond in sight to try and lower borrowing costs for member nations (and especially the periphery countries). The ECB may be slightly more politically independent than the Fed, but tightening while member nations are trying feverishly to balance their budgets - with their only chance being either a strong resurgent economy or a cheapening of their nominal liabilities through inflation - is highly unlikely.

Trichet has more credibility, though, than our own domestic monetary policymakers. I have to take some time here to mention Fed Vice-Chair Janet Yellen's speech from last weekend, since I have been meaning to for several days. It is important because the speech was an important defense of the Large Scale Asset Purchase (LSAP) program that the Fed has been conducting, and in that context we should be very afraid of what comes next. Because if this is the best thinking they have to share on the subject, then we are in a situation not unlike the baby who finds Daddy's firearm in an unlocked position. Tragedy is likely to ensue.

In a nutshell, Dr. Yellen's argument boils down to this:

- The LSAP program is not affecting the dollar.

- The LSAP program is not triggering "significant excesses or imbalances in the United States."

- The LSAP program does not risk markedly higher inflation because there is slack in the economy.

- However, the LSAP program has had an enormous effect on jobs, adding about 3 million jobs to the economy.

So, the program has been hugely successful in the ways they needed it to be, without any side effects and no chance of anything going wrong. Does it make me a bad person that I am naturally suspicious of a drug that will make me immensely strong, lengthen my life, improve my love life, and cure hangovers but has no negative side effects? How about if that drug worked as intended the first time it was tested?

Incidentally, the claim that the LSAP program has created about 3 million jobs is interesting because the Administration claimed 2 million jobs were saved or created through fiscal stimulus. Each is not claiming that their policy in conjunction with other policies not under their control created jobs, so these must be additive. Fiscal policy, plus monetary policy, saved or created some 5 million jobs. Right now, the Civilian Labor Force is 153,690,000 and unemployment is 14,485,000 (9.4%), so these actions have prevented an Unemployment Rate of about 12.7%. This is interesting because no one was forecasting a 12.7% Unemployment Rate before these programs were put into place, so the people who are now telling us that the drug is working perfectly are the same people who had previously told us that no drug would be needed.

These results - the 2 million, 3 million jobs - are coming from time series regressions that are conducted with high mathematics and great rigor. But there are lots of reasons that econometric analysis should not be expected to work well in this case:

- The distributions you are trying to analyze are not static, which is a precondition for most time series analysis, nor normal. Indeed, you are actually trying to change the distributions with your policy.

- It is pretty plain that the model is not completely specified. That is, the people who were examining whether fiscal policy was effective didn't include the separate effect of monetary policy, and vice-versa, so they both think it was their policy which worked. The fact that both of these policies are pushing in the same direction at roughly the same time also creates a problem of multicollinearity, a technical condition that basically means that with two people pulling on the same rope at the same time it is hard to tell who is pulling how much.

- The noise in the relationships far outweigh the signal, which means that all conclusions will (or should) have massive error bars on them.

- The analyst is analyzing the result of a single experiment. It is like trying to divine the laws of motion after hitting a cue ball a single time on the break of a game of billiards, except that the balls aren't round, you can't measure anything directly, and you have dirt in your eye. But in this case, the implications of reaching incorrect conclusions are far greater than if you were lining up your next shot in a game of pool.

Econometricians ought to be more guarded about conclusions such as this. Indeed, any reasonable experience with financial data sets tends to produce the realization that it is often hard to get any conclusive information out of them, although it is very easy to generate suggestive relationships that can't be rejected simply because the error bars are too large to reject any particular hypothesis. It may be that the econometricians within the Fed who are actually doing the dirty work are providing the policymakers with all of the proper caveats, and warnings about the usefulness of the data, and that they policymakers are simply ignoring it. Or it may be that econometricians at the Fed feel pressure knowing that while 90% of the time there is nothing conclusive to say, it is hard to support your case for continued employment when your results most of the time are indistinguishable from not working.

The Fed continues to be especially cavalier about the end game. Yellen says the Fed remains "unwaveringly committed" to price stability, but says:

"I disagree with the notion that the large quantity of reserves resulting from our asset purchases poses some special barrier to removing policy stimulus when the right time comes. The FOMC will be able to increase short-term rates by raising the interest rate that we pay on excess reserves--currently 1/4 percent. That ability will allow us to manage short-term interest rates effectively and thus to tighten policy when needed, even if bank reserves remain high."

Oh really? And you'll be able to do that, politically, with unemployment at 9%? And you're so sure that the effect will be immediate, perfectly calibrated, and won't have any unanticipated side effects? She also suggests that they can withdraw stimulus by offering deposits to member institutions through a Term Deposit Facility, and also by selling portions of their holdings. The notion that you can have a huge effect by implementing a policy, but that reversing the policy will have little effect, is an offense against common sense. No, it's an offense against financial physics. Yellen isn't the first Fed official to make statements like this, and won't be the last. And then, we'll have several years of apologies when it doesn't work out the way they said it would.

.

Retail Sales (Consensus: +0.8%, +0.7% ex-autos) is released tomorrow for December, and also Industrial Production (Consensus: +0.5%) and Capacity Utilization (Consensus: 75.6%). I think these estimates are very generous.

More important is the release of December CPI (Consensus: +0.4%, +0.1% ex-food-and-energy). It is probably useful to hearken back to November's release at this point and recall the odd quirk that we saw. In that release, the seasonally adjusted numbers produced different year-on-year rates than the unadjusted numbers - an effect that was most important for core CPI. On the unadjusted numbers, the year-on-year change in core CPI rose to 0.768%, 0.2% above the consensus expectation. But, oddly, the month-on-month rise was 0.1%, which was as-expected. This happened because the BLS used very different seasonal adjustment factors than the market expected. Had it used the seasonal adjustment we had all assumed, then core CPI would have risen 0.2% rather than 0.1%.

The fact that the year-on-year number rose a surprising amount tells you that core inflation last month surprised on the upside but the monthly change came in at consensus due to the dampening effect of the seasonal adjustment. But seasonal adjustments are just that: seasonal. Over the course of a year, they cancel out. There are two ways that can happen: (1) the offsetting adjustment can be spread over eleven other months, in which case the BLS has been doing this all year and we didn't notice, or (2) the offsetting adjustment occurs in one or two other months. Since December is the only month left, there is a chance that the offsetting adjustment occurs this month.

This is all very confusing, but here is the bottom line. If the year-on-year rate of change in core CPI is to stay at 0.768% and the year-on-year change in the seasonally-adjusted and non-seasonally-adjusted series converges to that rate, the reported month-on-month change in core inflation this month will not be 0.1% but a little above 0.2%. If the whole adjustment occurs in December, and if there is any acceleration in core inflation, a print of 0.3% is possible. Imagine what that would do to the market?

To be sure, this is all guesswork. My models suggest core CPI ought to be slowly rising now anyway, as the lags associated with inflation-related variables are finally starting to pass through the python. There is a small offsetting effect to the seasonal quirk mentioned above, which relates to the fact that energy price increases actually tend to dampen core CPI in the short run because of how the BLS extracts utility price increases from rents, and that's why I am not sitting around expecting 0.3%. But I am much more on my guard for that possibility than I have been in a long time. We haven't seen a 0.3% from core since 2008.

The headline is much less significant from a monetary policy standpoint, but quite important from a consumer confidence standpoint. The forecasts for headline inflation also look to me to be shaded on the low side somewhat; I think that year-on-year headline CPI could easily jump to 1.5% from 1.1%-1.2% where it has been for the last 6 months (this represents epic stability in this indicator!).

None of those figures are anything to get excited about in the big picture, but as of tomorrow morning the underlying beliefs that Trichet and other policymakers are relying on - chief among them that inflation is dead so long as there is a lot of unemployment, regardless of the lessons of history in this regard - may begin to be tested.

.

I will be making several visits in the City tomorrow, but will put out a comment concerning the CPI release sometime before Monday. There will be no commentary on Monday because of the bond market holiday; the regular schedule will resume on Tuesday.