Summary of Index Daily Closings for Week Ending September 24, 2004

| Date | DJIA | Transports | S&P | NASDAQ | Jun 30 Yr Treas |

| Sep 20 | 10204.89 | 3242.33 | 1122.20 | 1908.07 | 112^21 |

| Sep 21 | 10244.93 | 3271.22 | 1129.30 | 1921.17 | 113^01 |

| Sep 22 | 10109.18 | 3194.66 | 1113.56 | 1885.74 | 113^26 |

| Sep 23 | 10038.90 | 3173.97 | 1108.36 | 1886.36 | 113^13 |

| Sep 24 | 10047.24 | 3202.11 | 1110.11 | 1879.48 | 113^14 |

| SHORT TERM FORECAST (Next Two Weeks) | ||||

| TREND | PROBABILITY | Legend | ||

| Substantial Rise | Low | |||

| Market Rise | Medium | Very High | 80% | |

| Sideways | Medium | High | 60% | |

| Market Decline | High | Medium | 40% | |

| Substantial Decline | Medium | Low | 20% | |

| Very Low Under | 20% | |||

| INTERMEDIATE TERM FORECAST (Next 12 Weeks) | ||||

| TREND | PROBABILITY | Substantial | 800 points+ (DJIA) | |

| Substantial Rise | Low | Market Move | 200 to 800 points (DJIA) | |

| Market Rise | Medium | Sideways | Up or Down 200 (DJIA) | |

| Sideways | Medium | |||

| Market Decline | High | |||

| Substantial Decline | High | |||

Last week's Short-term TII was one of the more severe readings we've seen in a while, negative (69.00), portending a significant decline. This week the Dow Jones Industrial Average obliged, closing down 237.22. Once again prices have failed to bust up decisively through the 200 day moving average and in fact are now substantially below the 200 day MA and have broken below their 50 day MA. The DJIA's RSI is not at oversold levels, and the MACD is dropping hard, in negative territory.

Yet the decline did not instill fear, the VIX hardly budging, with downside volume light, and breadth mediocre. Major rallies typically commence at bottoms characterized by panic selling on high volume. The fact this is missing is Bearish. Until fear hits this market, while there may be choppy rallies, prices are destined to go lower.

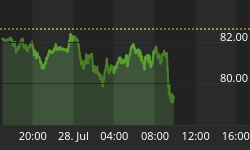

All the major averages fell hard this week. Interestingly, the Trannies had a key reversal week, hitting a new high for its intermediate-term move since 2002 at 3,271.22 on Tuesday, but ending the week lower than last week. That's a Bearish Hanging Man candlestick pattern on a weekly chart, and could signal a top. The pattern is not textbook perfect, but is evident.

| Equities Markets Technical Indicator Index (TII) ™ | ||||

| Week Ended | Short Term Index | Intermediate Term Index | ||

| May 28, 2004 | ( 3.50) | (48.48) | Scale | |

| June 4, 2004 | (55.75) | (34.07) | ||

| June 11, 2004 | (77.75) | (25.92) | (100) to +100 | |

| June 18, 2004 | (40.25) | (31.17) | ||

| June 25, 2004 | (34.00) | (26.10) | (Negative) Bearish | |

| July 2, 2004 | (41.50) | (27.64) | Positive Bullish | |

| July 9, 2004 | (32.50) | (30.21) | ||

| July 16, 2004 | (33.75) | (41.99) | ||

| July 23, 2004 | (59.00) | (49.98) | ||

| July 30, 2004 | 46.25 | (52.18) | ||

| Aug 6, 2004 | (38.00) | (50.40) | ||

| Aug 13, 2004 | (15.75) | (49.03) | ||

| Aug 20, 2004 | 9.25 | (43.82) | ||

| Aug 27, 2004 | 9.25 | (39.81) | ||

| Sep 3, 2004 | (39.25) | (40.06) | ||

| Sep 10, 2004 | (49.25) | (45.78) | ||

| Sep 17, 2004 | (69.00) | (44.73) | ||

| Sep 24, 2004 | (52.25) | (42.02) | ||

This week the Short-term Technical Indicator Index comes in at negative (52.25), indicating a market decline is probable. This indicator is a useful predictor of equity market moves over the next two weeks, both as to direction and to a lesser extent strength of move. For example, readings near zero indicate narrow sideways moves are probable. Readings closer to +/-100 indicate with a higher degree of confidence that an impulsive move up or down is likely over the short run. Market conditions can change on a dime, or the Plunge Protection Team can come in and temporarily stop market slides, so it may be unwise to trade off this weekly measured indicator.

The Intermediate-term Technical Indicator Index is useful for monitoring what's over the horizon - over the next twelve weeks. It serves as an early warning system for unforeseen trend changes of considerable magnitude. This week the Intermediate-term TII comes in at negative (42.02).

Markets tend to seek order, both in terms of price and time. They especially like to hit tops and bottoms on Fibonacci numbers of days or weeks, or on Fibonacci ratios of prior moves. Leonardo Fibonacci was a 12th century mathematician who focused upon a unique sequence of numbers that continuously turned up in nature. The sequence goes like this: It starts with the number 1 and then adds that number to itself to get the next number. It then takes those two numbers and adds them together to get the next number in sequence. Each number next in sequence is the sum of the prior two numbers in the sequence, ad infinitum. Thus the sequence looks like this: 1, 1, 2, 3, 5, 8, 13, 21, 34, 55, 89, 144, 233, 377, etc... The ratios between these numbers are unique in that each addend is either .382 or .618 of the sum. For example, 13 plus 21 equals 34. 21 is .618 of 34. 13 is .382 of 34. .618 plus .382 equals a complete 1.00. This holds true for all pairs. These pairs are known as phi mates. The world around us is filled with these ratios and relationships. What is so amazing is that market price and time movements are also dominated by Fibonacci numbers and ratios.

Take note that the Dow Industrials ended their two decade Bull Market on 1/14/2000. They topped there and ever since have been in a secular Bear market. Since this dramatic date, every single market top or bottom of significance has occurred at a Fibonacci .618 to .382 ratio of trading days from either the starting date 1/14/00, or another top or bottom, based upon closing balances. Since this golden ratio has been consistent so far during this Bear market in the DJIA, it is therefore logical to extrapolate this phi ratio into the future in order to determine high probability bifurcation points - future tops or bottoms.

The August 12th 2004 closing low came 1,150 trading days from 1/14/00. It was also 440 trading days from 11/11/02's mini-bottom (8,358.95). This 11/11/02 mini-bottom was 710 trading days from 1/14/00. 440 trading days equals .382 of 1,150 trading days, and 710 trading days equals .618 of 1,150 trading days.

The recent top in the DJIA came on September 7th, 2004 (at 10,341.16). 9/7/04 is 1,167 trading days from the start of the Bear, 1/14/00. 9/7/04 is also 445 trading days from 11/27/02, a significant high. This high, 11/27/02, came 722 trading days from 1/14/00. 445 trading days is .382 of 1,167, and 722 trading days is .618 of 1,167. Thus, the 9/7/04 and 11/27/02 tops are phi mates.

What's important for us is the next turn date. It is amazing that each successive future top or bottom projects a phi relationship from each successive past high or low, in date order. Thus, if 9/8/04's turn came from 11/27/02, then the next turn must come from the next top or bottom that followed 11/27/02, which was 12/27/02's bottom. To calculate the next turn date in 2004, we count the number of trading days from 1/14/00 to 12/27/02. That gives us 742 trading days. Projecting this to be phi .618 of the total trading days to our next turn date, we get an exact 1,200 trading days. From 1/14/00, if we count 1,200 trading days we come to a turn date of 10/22/04. Thus, our next projected key turn date is 10/22/04. We don't know if this will be a top or a bottom. Right now it looks like a bottom. But that is a long way off. If it is a bottom, then we are in the midst (start?) of a significant decline. 10/22/04 is 458 trading days from 12/27/02, a Fibonacci .382 of 1,200 trading days. This projection was right on the money for September 7th's turn, and was very close in anticipating June 23rd's turn. Yes, markets seek order, billions of transactions from millions of people all over the world following program trades, computer strategies, greed, fear, insider knowledge, no knowledge, random events influencing buy and sell decisions - yet the sum of all trades continuously make tops and bottoms that occur at perfect Fibonacci golden ratio times. Could it be that God has a sense of humor, that in spite of man's arrogance, his intelligence, his self-serving decisions with no regard to anything but what is individually on his mind, ultimately the sum total of all trades is orderly? Is this God saying, "Man, you can try as you might, but ultimately I am in control."? How else could these Fibonacci trade dates be working to perfection for so long a period of time?

The above chart shows that whenever we reached a Fibonacci number of weeks from 1/14/00, a secondary market top or bottom of some significance occurred and a trend reversal ensued.

The chart on the next page highlights all the trading day phi-related tops and bottoms since 1/14/2000. If this doesn't humble Wall Street, I don't know what will.

| * 3/7/2000's low is 38.0% of the total # of trading days from 1/14/2000's High to 5/26/2000's Low * 5/26/2000's Low is 38.0% of the total # of trading days from 1/14/00's High to 12/20/00's Low * 9/6/2000's High is 38.3% of the total # of trading days from 1/14/00's High to 9/21/01's Low * 10/18/2000's Low is 38.8% of the total # of trading days from 1/14/00's High to 1/4/02's High * 11/6/2000's High is 37.6% of the total # of trading days from 1/14/00's High to 3/19/02's High * 11/22/2000's Low is 37.9% of the total # of trading days from 1/14/00's High to 4/29/02's Low * 12/5/2000's High is 38.7% of the total # of trading days from 1/14/00's High to 5/14/02's High * 1/3/2001's High is 37.6% of the total # of trading days from 1/14/00's High to 8/22/02's High * 3/22/2001's High is 37.9% of the total # of trading days from 1/14/00's High to 3/11/03's Low * 5/21/2001's High is 62.6% of the total # of trading days from 1/14/00's High to 3/19/02's High * 9/5/2001's High is 38.0% of the total # of trading days from 1/14/00's High to 5/17/04's Low * 9/21/2001's Low is 61.6% of the total # of trading days from 1/14/00's High to 10/9/02's Low * 1/4/2002's High is 61.5% of the total # of trading days from 1/14/00's High to 3/31/03's Low * 3/19/2002's High is 63.4% of the total # of trading days from 1/14/00's High to 6/17/03's High * 7/23/2002's Low is 61.7% of the total # of trading days from 1/14/00's High to 2/11/04's High * 8/22/2002's High is 62.1% of the total # of trading days from 1/14/00's High to 3/24/04's Low * 10/9/2002's Low is 61.6% of the total # of trading days from 1/14/00's High to 6/23/04's Low |

The SPX to VIX ratio hasn't dropped much during this week's 237 point sell-off. It remains at levels signaling stock market crashes, sitting at an extreme high 77.74 reading as of September 24th. This ratio must decline below 35 for an intermediate-term sustainable Bull run. The S&P 500 must decline substantially, and the VIX must rise sharply for this to occur. Just to give you an idea what we're talking about here, the S&P 500 would have to fall to 1,000, and the VIX simultaneously rise to 30 for the SPX to VIX ratio to fall to 33. That would be the equivalent of about an 1,100 point drop in the DJIA from today's 10,047 level.

The chart on the top of the next page compares the 10 day average of the Call/Put ratio to the Dow Industrials since this Bear Market began. This is a contrary sentiment indicator. We've noted that whenever this ratio approached 1.40, a decline is imminent. Whenever it approaches 1.0, a rally is imminent. We sit at 1.16 as of Friday September 24th. That is a neutral reading, conducive to a little more decline and then a bounce over the next week to ten days.

The chart that follows is an update of the Transports/Industrials divergences since 1999. Since February 2004, we have had one of the longest time-wise, and most flagrant price-wise, of any non-confirmations ever. What is instructive here is that since 1999, every single major divergence between these two averages has led to a stock market crash within 2 months. This chart is saying there is very high probability that an equity crash is imminent.

Since February 2004 the DJIA has bounced up and down from the upper to lower boundary of the downward sloping trend-channel, almost like clockwork. The temptation is to expect the current decline to do the same, fall to 9750 or slightly below, then bounce back up toward 10,250. While that may transpire, we think this decline is more significant than March's, April/May's, or July/August's. We believe this decline has good probability of breaking the lower trend-line, probably not immediately, but before the end of October as wave iii of 3 of 1 of (3) down completes. Here's why:

The moves since February 2004 have been choppy. That means they are either an expanded wave 4 of C of (2) up, with wave 5 up about to occur - or the labeling above is the accurate case which implies we are finally entering some downside wave 3's. Wave 3's are typically powerful and the longest waves - longer than 1's or 2's. Thus, if so, this move down should take prices much lower than the bottom boundary line. We also feel the divergence between the Dow Transports and the Dow Industrials - one of the most flagrant ever! - portends a powerful decline, a crash, and soon. Also, given the next Fibonacci turn date of 10/22/2004, a month away, that means prices should decline further due to the length of time for this trend to remain in play before the next turn.

Here's the way we see prices moving. Minuette degree wave i down of minor degree 3 down should complete just below 10,000 sometime next week. That should be followed by a strong minuette degree wave ii up from oversold levels that moves prices back into overbought territory. Then minuette degree wave iii down of 3 down will feel like a crash and bust through the lower boundary of this declining trend-channel. We believe the top of primary degree wave (2) up completed June 23rd, 2004 as a truncated 5th of C up of an A-B-C up of (2). From a Fibonacci time perspective, this date was most important as the phi mate of the bottom for the four year Bear Market that occurred on October 9th, 2002, labeled primary degree wave (1) down from January 14th, 2004. Given this belief, the choppy down-up move from June 23rd to August 12th to September 7th was a minor degree wave 1 down and minor 2 up, a move that fits the personality of waves 1 and 2. Wave 2 retraced .786 of wave 1, as has been the pattern for 2's since this Bear began. It was clearly a 3-wave a-b-c move - corrective, not impulsive.

That leaves us with the current decline, which we believe to be wave iii of 3 of 1 of (3) - a likely crash. Supporting this is the SPX to VIX ratio, declining M-3, a major Dow Theory nonconfirmation and divergence in the Trannies/Industrials, awful fundamentals, oil through the roof, the Fed raising interest rates, and the September/October negative season for stocks. Dubya can't have this. To halt the carnage, watch for the Plunge Protection Team to step in. Look for a rally from October 22nd into the election. What a fascinating time for the markets.

The above chart of the Trannies (courtesy of www.stockcharts.com) shows a completed Elliott Wave count, minuette degree wave v up of minor degree 5 up of intermediate degree C up of primary degree (2) up finishing at Tuesdays' 3,271 top. Minuette degree wave v up was a Rising Bearish Wedge pattern, a termination pattern seen often at major tops. The MACD is falling hard and looks to be forming a Bearish Head & Shoulders pattern. Same in the RSI, which is not oversold.

After a brief reprieve, the Philadelphia Semiconductor Index ($SOX) looks like it is heading back down again. The corrective rally could only manage to retrace a Fibonacci .382 of the decline over the summer. Friday this index lost nearly 3 percent of its value, pulling back from an RSI level where three recent prior tops occurred, and enough to cause the MACD to rollover.

This index is a picture of perfect distribution from strong in-the-know hands to weak amateur hands, the massive two year Rounded Bearish Top forming a perfectly symmetrical halo over prices. Prices have reached due east (picture a globe) and thus have nowhere to go but south for this Rounded Top pattern to complete.

A Head & Shoulders Top has been confirmed with the price action over the summer, a decisive break below the neckline. We are able to estimate a minimum downside target for the ultimate decline by measuring the distance from the neckline to the head and subtracting this from the neckline. That gets us a target of around 300, another 82 points below where we currently sit.

This action will be felt by the NASDAQ.

The Economy:

Let's open with Dubya's latest reelection-move. The Energy Department has announced it will release crude oil from the nation's strategic reserve to alleviate "shortages created by Hurricane Ivan" (i.e., prices). Understand this is not what Dubya wanted to do. He had to do it. What he wants to do is reward his oil friends with much higher oil prices. That goodie will have to wait until December.

The headline read "Retail Sales up from last year" on www.cnnmoney.com, but buried in the copy was the fact that sales fell 1.1 percent last week, according to the International Council of Shopping Centers and UBS. Department stores are getting especially hit.

That's it for the good news. Enough sugarcoating. Now the tough stuff: The Conference Board reported that its U.S. Index of Leading Economic Indicators fell 0.3 percent, the third straight monthly decline. We learned from the Commerce Department on Friday that Durable Goods Orders fell 0.5 percent in August. Transportation was the main drag. Including aircraft orders, and excluding defense, orders fell a whopping 7.4 percent, the largest decline in two years. Think Dubya has another war in mind for early next year?

The National Association of Realtors reported that Existing Home Sales fell 2.6 percent last month. Still it was the sixth highest reading ever. So the numbers are good, but watch for a countertrend developing. While Housing Starts rose in August (wouldn't want to be doing that on spec) Building Permits fell 5.5 percent in August. Fannie Mae is in trouble as regulators have found improper accounting practices being used to smooth quarter to quarter earnings according to CNNMoney. Fannie Mae (FNM) crashed fifteen percent this week.

While we're on the subject of corporate news, Morgan Stanley announced its third quarter 2004 earnings will be 34 percent less than a year ago. Trading income was blamed. Wonder Bread and Hostess Cakes' bakery owner, Interstate Bakeries, filed for Bankruptcy. This one is personal as I used to be one of those happy Twinkie delivery guys during the summers of my college years at Villanova University. I remember getting up before the sun - about the time my buddies were going to sleep - loading fresh-baked pastries, and heading off to the first store I could find open, loving the smells and munchin' on something sweet, often a blueberry pie. It was then that I acquired a fondness for strong coffee. Twelve hour days and cash collections from tough neighborhood Deli's motivated extra hard studying during school. I was paid well, learned a lot and wouldn't take the experience back for anything. Here's to hoping the Twinkie rises again.

An article by Porus P. Cooper in the Philadelphia Inquirer 9/21/04 noted that there has been a marked increase in negative forecast guidance among S&P 500 companies, over fifty percent of the third quarter 2004 guidance coming in lower than analysts' expectations according to Thomson Financial.

Jobless Claims rose significantly this past week, reported at 350,000 according to the Labor Department.

The ABC News/Money magazine Consumer Comfort Index fell to negative (-9) last week.

Money Supply, the Dollar, and Gold:

M-3 fell again last week, down another $4.9 billion on a seasonally adjusted basis. Over the past eleven weeks, M-3 is down 34.8 billion. Our research has found that whenever M-3 either plateaus or declines for more than two months, stocks fall one to three months thereafter.

The U.S. Dollar has been tracing out a Symmetrical Triangle pattern, and it appears to have broken down from its vertex. Symmetrical Triangles are continuation patterns and are considered Bullish in uptrends and Bearish in downtrends. The probability is high that breakouts will be in the same direction as the prior trend - in the current case down. Often what follows is an even stronger move in the same direction as the prior trend. What is happening here is buyers are not able to push prices into a new trend. As sellers see this weakness, they gain confidence that the past trend will resume, forcing a breakout to the downside. Once prices break below 87, a small Head & Shoulders Top will be confirmed with a decline to the low 80s expected. Should price action defy the odds, a decisive break above 91 would be Bullish.

Gold remains inside both its rising short-term and long-term trend-channels while battling a Bearish Double Top. A break below 397 is Bearish; above 420 Bullish. The Mining Stocks ($HUI) rose above the small Bullish Flag we mentioned last week - as expected - and are completing a Rising Bearish Wedge termination pattern as an Elliott Wave v of c of corrective wave 2 up. Wave v has completed 1 up, 2 down, 3 up, and 4 down. Only micro degree wave 5 up of v is required, and it is possible it will reach for 224.60, the .786 retrace of wave 1 down. Its RSI is now overbought.

U.S. Bonds and Interest Rates:

Price action this week blew apart the long-term Elliott Wave count we had, as the move up since May has retraced all of the decline from March. So no wave 2 up going on here. Further, the long-term Bearish Head & Shoulders pattern - while still in play - is losing some of its proportionality and has yet to be confirmed. A move below 100 would confirm the Bearish case. But that is a long way off. It may be that prices will reach a new high, above 118.50. That could happen should the economy continue to weaken and stocks fall. Bonds are clearly not happy about the prospects for economic growth, and perhaps even smell the foul scent of deflation.

Orrrr, could the Master Planners be purchasing the long end of the curve to keep the housing bubble going? On the one hand the Fed claims the recovery is coming along just fine, and yet the long end of the curve sees very little threat of inflation. We are watching the yield curve flatten, the end to the carry trade squeezing trading profits at the big boy banks. Flattened yield curves portend a slowing economy, sometimes recessions, and equity slides.

The Relative Strength Indicator is in overbought territory. This might lead to a decline, however prices can remain overbought for a while. The MACD is curling back up again, saying it wants more. Tough call right now for U.S. Bonds.

On the other hand, the Long-term Bearish Head & Shoulders Top remains intact in the U.S. Treasury Ten Year Note. All that is needed is a confirmation with a price break below 108. Prices have reached a Fibonacci .618 retrace of the March to June decline, a common place for a trend reversal. The RSI is approaching overbought levels and may be tracing out a small Head & Shoulders top formation. Same for the MACD, which appears to have also traced out a Bear hook. Notes look like they are about to break lower, which may be the clue that clarifies the U.S. Bond picture. However, there is room for the Note to rise further, to a .786 retrace level, around 115.50ish. An equity slide would likely push notes up there before turning down in earnest.

Bottom Line:

Several major technical patterns and indicators warn of crash potential. However, even if this is the start of one, there are rallies inside crashes when conditions become oversold, and the Plunge Protection Team is alive and well and chartered to stop severe slides. Thus shorts can get their hat handed to them if they are not careful. The major Dow Theory non-confirmation and divergence bothers me the most. This is a very bad sign for the markets. Perhaps Dubya can push a slide past the election, so the Bears may have to be patient for another six weeks. That said, this is a time where great caution should be exercised.

"There is no wisdom and no understanding

And no council against the Lord.

The horse is prepared for the day of battle,

But the victory belongs to the Lord."

Proverbs 21:30,31

Special Note: Be sure to register under the subscribers' section at www.technicalindicatorindex.com for e-mail notifications and password access of our new mid-week market analysis, usually available on either Tuesdays or Wednesdays. These midweek updates are only available via password access when posted on the web.

| Key Economic Statistics | ||||||||

| Date | VIX | Mar. U.S. $ | Euro | CRB | Gold | Silver | Crude Oil | 1 Week Avg. M-3 |

| 4/30/04 | 16.69 | 90.76 | 119.70 | 270.75 | 387.5 | 6.07 | 37.38 | 9171.5 b |

| 5/07/04 | 18.13 | 91.30 | 118.83 | 270.40 | 379.1 | 5.58 | 39.93 | 9230.2 b |

| 5/14/04 | 18.47 | 91.81 | 118.69 | 267.00 | 377.1 | 5.72 | 41.38 | 9232.3 b |

| 5/21/04 | 18.44 | 90.53 | 120.05 | 268.75 | 384.9 | 5.87 | 39.93 | 9278.0 b |

| 5/28/04 | 15.52 | 88.98 | 122.10 | 276.25 | 394.0 | 6.11 | 39.88 | 9251.6 b |

| 6/04/04 | 16.57 | 88.50 | 122.93 | 274.75 | 391.7 | 5.81 | 38.49 | 9255.6 b |

| 6/11/04 | 15.10 | 89.23 | 121.01 | 269.25 | 386.6 | 5.78 | 38.45 | 9265.9 b |

| 6/18/04 | 14.95 | 89.41 | 121.17 | 267.75 | 395.7 | 5.98 | 39.00 | 9305.7 b |

| 6/25/04 | 15.19 | 89.22 | 121.41 | 270.75 | 403.2 | 6.12 | 37.55 | 9281.0 b |

| 7/02/04 | 15.15 | 88.18 | 123.09 | 265.50 | 398.7 | 6.01 | 38.39 | 9308.3 b |

| 7/09/04 | 15.78 | 87.41 | 124.10 | 269.00 | 407.0 | 6.46 | 39.96 | 9244.0 b |

| 7/16/04 | 14.43 | 87.12 | 124.36 | 271.50 | 406.8 | 6.72 | 41.25 | 9239.4 b |

| 7/23/04 | 16.50 | 89.23 | 120.88 | 269.50 | 390.5 | 6.33 | 41.71 | 9260.5 b |

| 7/30/04 | 15.27 | 90.12 | 120.10 | 267.00 | 391.7 | 6.56 | 43.80 | 9273.0 b |

| 8/06/04 | 19.34 | 88.45 | 122.69 | 268.25 | 399.8 | 6.77 | 43.95 | 9266.9 b |

| 8/13/04 | 17.98 | 87.97 | 123.68 | 269.19 | 401.2 | 6.62 | 46.58 | 9248.9 b |

| 8/20/04 | 16.00 | 88.22 | 123.03 | 279.50 | 415.5 | 6.87 | 46.72 | 9260.3 b |

| 8/27/04 | 14.74 | 89.80 | 120.20 | 275.00 | 405.4 | 6.58 | 43.18 | 9296.5 b |

| 9/03/04 | 14.28 | 89.56 | 120.66 | 275.25 | 402.5 | 6.59 | 43.99 | 9286.1 b |

| 9/10/04 | 13.75 | 88.60 | 122.61 | 272.50 | 403.8 | 6.16 | 42.81 | 9278.4 b |

| 9/17/04 | 14.03 | 88.10 | 121.76 | 275.75 | 407.6 | 6.28 | 45.59 | 9273.5 b |

| 9/24/04 | 14.28 | 88.59 | 122.57 | 278.50 | 409.7 | 6.42 | 48.08 | - |

Note: VIX complacent, Oil heads for a new high