Given the stark contrast between asset class performance before and after the implied announcement of QE2, the Fed's statements related to quantitative easing in the coming weeks will have a significant impact on the outlook for stocks and the relative attractiveness of asset classes, market sectors, and subsectors.

The Fed is scheduled to issue statements on March 15 and April 27, 2011 with the following concerns as a backdrop:

- Higher food and oil prices.

- Unemployment hovering near 9%.

- Turmoil in the Middle East.

- Devastation and ongoing uncertainty in Japan.

With QE2 set to end on June 30, the natural questions for market participants are:

- Should we be concerned?

- Did QE1 and QE2 impact asset prices?

- Is QE3 a possibility?

We believe the answers to all three questions are "yes". The chart below shows the very uncomfortable transition from QE1 to QE2.

For those market participants who doubt whether QE3 hints by the Fed will have an impact on asset prices, the chart below shows the S&P 500's performance after Ben Bernanke's August 27, 2010 Jackson Hole speech, which basically told the markets QE2 was on the way.

The role of asset prices, balance sheets, and 'full employment' in the Fed's decision-making process are often underestimated by those who focus primarily on inflationary pressures. Consequently, many investors and economists are forecasting the U.S. Federal Reserve will raise rates sooner than history would suggest. The chart below was published by Bloomberg on February 9, 2011.

Bloomberg's commentary related to the chart above:

After the past two U.S. recessions, the Fed didn't start raising policy rates until joblessness had fallen about three- quarters of the way back to the full-employment level, the CHART OF THE DAY (above) shows. To satisfy that requirement, the jobless rate would need to be 6.5 percent, compared with today's 9 percent.

Just as the chart above implies rates may stay lower longer than most believe, it is also possible the market may be underestimating the odds of the Fed bringing QE3 to life in the coming months. If any portion of the March 15 and/or April 27, 2011 Fed statements leave the door open to QE3, the impact on the markets could be significant. We recently studied the performance of ninety-two assets classes/sectors/investment options when:

- QE1 Was Not In Play: Between April 23, 2010 and August 26, 2010.

- QE2 Was In Play: Between August 27, 2010 and March 9, 2011.

The results of the study will help us focus on different areas of the market based on the Fed's statements related to quantitative easing. The table below summarizes our findings when looking at the top eighteen performers under the two scenarios. The very limited overlap in asset class performance between the left and right sides of the table below highlights the importance of the Fed's stance on quantitative easing relative to the outlook for both defensive and inflationary/economically-sensitive assets.

The investments that provided the detail behind the summary table above are shown in the colored tables below. Notice only two investments, silver (SLV) and agriculture (RJA), performed well in both QE environments. The investments highlighted in blue below recently showed improving relative strength which supported raising some additional cash in the last week.

If the Fed leans toward more quantitative easing, we will focus on assets on the right side of the tables above and below, including expanding our search to similar inflationary options. If the Fed leans toward wrapping up quantitative easing in June, we will consider the relative merits of the defensive assets on the left side of the tables above and below.

All bull markets have backing from market participants based on both speculation and fundamentals. Speculators are a normal part of functioning asset markets since they provide needed liquidity. A healthy and sustainable bull market has a reasonable balance between its reliance on fundamentals and speculation.

The rally off the 2010 summer lows, in our opinion, was based heavily on speculation. On August 27, 2010 with the financial markets teetering on the deflationary abyss, Ben Bernanke signaled QE2 was on the way in his Jackson Hole speech.

The speculative bent to investing since the summer 2010 lows has many market participants, including us, concerned that an end to quantitative easing could usher in a repeat of the sharp declines in asset prices seen between April 23 and August 26, 2010. If this scenario plays out, we will monitor the relative strength of the defensive assets and inflationary assets listed above in order to make more informed investment decisions.

As we await the Fed's statements due on March 15 and April 27, we should keep in mind Federal Reserve Chairman Ben Bernanke's response, while recently at the National Press Club, to a question about the potential for QE3:

"In the end, we'll just ask the same questions. Where's the economy going, and what do various inflation indicator look like? We'll ask those questions. If unemployment is still too low, then we may continue. If we're moving towards full employment, then we won't need to stimulate more."

Remarks from William Dudley, President of the Federal Reserve Bank of New York, during a recent speech at New York University may also provide some insight to the Fed's stance:

"The economy can be allowed to grow rapidly for quite some time before there is a real risk that shrinking slack will result in a rise in underlying inflation."

The recent drop in the unemployment rate may also factor into the Fed's decision-making process. Caroline Baum noted in a recent opinion piece:

In the last two months, the civilian unemployment rate plummeted from 9.8 percent to 9 percent. While payroll growth, derived from a separate survey of businesses, was tepid, history suggests such steep falls aren't a drop in the bucket. Large month-to-month declines in the unemployment rate are rare and "usually signal the start of a very strong upturn in growth," says Joe Carson, director of economic research at AllianceBernstein in New York.

With a weak stock market, high unemployment, and recent events in Japan, comments made by Charles Evans, President of the Federal Reserve Bank of Chicago, during a recent interview with the Financial Times may foreshadow Fed statements in March and/or April geared toward accommodative policy:

"The message that comes out of what I think of as high-quality research on this subject is that policy ought to remain accommodative for really quite a while, even a while after conditions start to improve."

A March 2 BusinessWeek/Bloomberg article covering the possible continuation of the Fed's asset purchase program stated:

A third round of purchases "has to be a decision" of the Federal Open Market Committee, and "it depends again on our mandate" for stable prices and maximum employment, Bernanke said in response to Texas Representative Jeb Hensarling, the House panel's vice chairman and a critic of QE2.

Responding to a question from Representative Nydia Velazquez, a New York Democrat, Bernanke said the Fed's policy of keeping its benchmark rate near zero for an "extended period" helps provide support to the economy, "which in our judgment, it still needs. The economy's recovery is not firmly established, and we think monetary policy needs to be supportive," he said.

Looking at the case for ending QE2, Bloomberg noted on March 4:

Economists such as Joseph Lavorgna say the Fed should stick to its commitment to end the program in June. "What markets would like are clear rules," said Lavorgna, chief U.S. economist at Deutsche Bank Securities Inc. in New York. "If they said they are going to end in June, they should end in June." That's a view shared by the Philadelphia Fed's Plosser, who is also a voting member of the FOMC this year.

Regardless of whether it is embedded in the March 15 or April 27 Fed statement, based on the remarks from the Atlanta Fed's Dennis Lockhart, we can expect some direction from the Fed relative to where they are headed with quantitative easing:

"It is important that we communicate so we don't surprise markets, regardless of the chosen path of that particular policy," he told reporters after a speech in Tallahassee, Florida.

An AP article from March 14 does a good job summing up the situation as the Fed heads into their March 15 meeting:

The Fed chief and a majority of his colleagues argue that the economy still needs support from the bond purchases, especially with unemployment still high and home prices in many areas depressed. But a vocal minority on the Fed has raised concerns that the bond purchases, combined with higher prices for food, fuel and other commodities, will spread inflation through the economy. They also say they worry that the purchases could feed speculative buying that could inflate new bubbles in the prices of stocks or other assets.

We believe the key portions of the AP statement above are the "Fed chief and a majority of his colleagues" versus "a vocal minority". The history of the Fed in recent years is that the Chairman tends to set policy. Since Ben Bernanke remains at the helm, we will remain open to the possibility of a third quantitative easing program (QE3), which could significantly alter the market's general outlook and relative performance of asset classes. Another scenario, a stronger than expected economy, could discount the need for QE3, but under those conditions inflationary assets will most likely outperform defensive assets.

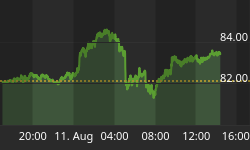

Some anecdotal evidence that traders positioned themselves for the possibility of inflationary statements from the Fed comes via the relative strength charts below. The charts show Monday's trading session. Notice how defensive assets weakened relative to the S&P 500 in the afternoon.

Inflationary assets drew more interest from buyers late in the day. These charts mean little except that the expectation on the street is leaning toward inflationary rather than deflationary statements from the Fed on March 15.

Monday's market action did contribute to our decision to take no further defensive actions near the close. We will wait for the Fed's statement and monitor the market's reaction both on Tuesday afternoon and Wednesday morning.