For the week, the S&P500 slipped 0.3% (up 5.6% y-t-d), while the Dow was little changed (up 6.9%). The Banks were unchanged (up 0.4%), while the Broker/Dealers declined 0.8% (down 0.4%). The Morgan Stanley Cyclicals dropped 1.7% (up 5.2%), and the Transports sank 2.6% (up 2.4%). The Morgan Stanley Consumer index added 0.2% (up 1.1%), while the Utilities were unchanged (up 1.8%). The S&P 400 Mid-Caps declined 0.9% (up 8.9%), and the small cap Russell 2000 dipped 0.7% (up 7.3%). The Nasdaq100 fell 0.9% (up 4.7%), while the Morgan Stanley High Tech index added 0.1% (up 2.6%). The Semiconductors rallied 2.4% (up7.6 %). The InteractiveWeek Internet index was little changed (up 3.4%). The Biotechs gained 1.0% (up 6.6%). With bullion surging $46 to a new record high, the HUI gold index jumped 6.4% (up 5.7%).

One-month Treasury bill rates ended the week at one basis point and three-month bills closed at 4 bps. Two-year government yields added one basis point to 0.81%. Five-year T-note yields ended the week up 7 bps to 2.31%. Ten-year yields rose 13 bps to 3.58%. Long bond yields ended the week up 16 bps to 4.64%. Benchmark Fannie MBS yields were 10 bps higher to 4.37%. The spread between 10-year Treasury yields and benchmark MBS yields narrowed 3 bps to 79 bps. Agency 10-yr debt spreads were little changed at negative 3 bps. The implied yield on December 2011 eurodollar futures slipped 2 bps to 0.59%. The 10-year dollar swap spread was little changed at 10 bps. The 30-year swap spread declined one to negative 23 bps. Corporate bond spreads were mixed to narrower. An index of investment grade bond risk was little changed at 94 bps. An index of junk bond risk fell 5 bps to 433 bps.

Investment grade debt issuers included GE Capital $1.5bn, Hormel Foods $250 million, and Raymond James $250 million.

Junk bond funds saw inflows of $1.0bn (from Lipper). Issuers included Liz Claiborn $1.25bn, Aramark $600 million, Penn Virginia $300 million, DJO Finance $300 million, and Stewart Enterprises $200 million.

Convertible debt issuers included Fifth Street $150 million.

International dollar debt issuers included BNP Paribas $3.0bn, National Bank of Australia $2.2bn, Hungary $1.25bn, RCI Banque $1.25bn, Banco Votorantim $1.25bn, Deutsche Telekom $1.25bn, Pernod-Ricard $1.0bn, Woolworths $850 million, Woori Bank $500 million, Sappi Papier $350 million, Fufeng Group $300 million, and Navios Logist $200 million.

U.K. 10-year gilt yields rose 9 bps this week to 3.81% (up 21bps y-t-d), and German bund yields jumped 11 bps to 3.48% (up 41bps). Ten-year Portuguese yields rose 14 bps to 8.55% (up 183bps). Spanish yields declined 5 bps to 5.25%. Irish yields sank 71 bps to 9.06% (up 72bps), while Greek 10-year bond yields rose 8 bps to 12.46% (up 21bps). The German DAX equities index gained 0.5% (up 4.4% y-t-d). Japanese 10-year "JGB" yields added 4 bps to 1.315% (up 15.5bps). Japan's Nikkei increased 0.6% (down 4.5%). Emerging markets were mixed. For the week, Brazil's Bovespa equities index declined 0.8% (down 0.8%), and Mexico's Bolsa fell 0.8% (down 2.8%). South Korea's Kospi index added 0.3% (up 3.8%). India's equities index increased 0.2% (down 5.2%). China's Shanghai Exchange jumped 2.1% (up 7.9%). Brazil's benchmark dollar bond yields rose 8 bps to 4.68%, and Mexico's benchmark bond yields rose 7 bps to 4.53%.

Freddie Mac 30-year fixed mortgage rates added one basis point to 4.87% (down 34bps y-o-y). Fifteen-year fixed rates increased a basis point to 4.10% (down 42bps y-o-y). One-year ARMs were down 4 bps to 3.22% (down 92bps y-o-y). Bankrate's survey of jumbo mortgage borrowing costs had 30-yr fixed jumbo rates down 4 bps to 5.45% (down 50 bps y-o-y).

Federal Reserve Credit jumped $22.2bn to a record $2.620 TN (22-wk gain of $339bn). Fed Credit was up 2121bn y-t-d and $339bn from a year ago, or 14.4%. Elsewhere, Fed Foreign Holdings of Treasury, Agency Debt this past week (ended 4/6) dipped $224 million to $3.407 TN. "Custody holdings" were up $383bn from a year ago, or 12.7%.

Global central bank "international reserve assets" (excluding gold) - as tallied by Bloomberg - were up $1.592 TN y-o-y, or 20.3%, to a record $9.447 TN.

M2 (narrow) "money" supply slipped $1.1bn to $8.897 TN. "Narrow money" has expanded at a 2.8% pace y-t-d and 4.6% over the past year. For the week, Currency increased $1.9bn. Demand and Checkable Deposits rose $10.0bn, while Savings Deposits fell $12.0bn. Small Denominated Deposits declined $3.7bn. Retail Money Funds increased $2.7bn.

Total Money Fund assets rose $8.3bn last week to $2.743 TN. Money Fund assets were down $66bn y-t-d, with a decline of $220bn over the past year, or 7.4%.

Total Commercial Paper outstanding jumped $11.8bn to a 21-wk high $1.093 Trillion. CP was up $124bn y-t-d, although it was down $4bn from a year ago.

Global Credit Market Watch:

April 8 - Bloomberg (Sapna Maheshwari): "Relative yields on U.S. corporate bonds fell to the lowest level in more than three years, showing growing confidence the economic recovery is back on track..."

April 8 - Bloomberg (Maria Petrakis): "With markets indicating Portugal may be the last euro country to need a bailout, investors are turning their attention to a potential bond restructuring in Greece, whose unmanageable debt load triggered the crisis. Greek bond yields have soared and the nation's credit ratings have been cut since May when the country got 110 billion euros ($157bn) of aid in return for wage and pension cuts."

April 5 - Bloomberg (Jody Shenn): "The biggest year since 2003 for the packaging of U.S. government-backed mortgage bonds into new securities has extended into 2011, bolstered by banks seeking investments protecting against rising interest rates. Issuance of so-called agency collateralized mortgage obligations, or CMOs, reached $99 billion last quarter, following $451 billion in 2010..."

Global Bubble Watch:

April 5 - Bloomberg (Patricia Kuo): "ING Groep NV, the top arranger of buyout loans in Europe this year, sees a 'liquidity bubble' building as lenders forego protection and accept lower fees. 'There is a liquidity bubble in the European leveraged loan market at the moment, driven by institutional fund liquidity,' said Gerrit Stoelinga, global head of structured acquisition finance at... ING, which toppled Lloyds Banking Group Plc as no. 1 loan arranger to private-equity firms..."

April 7 - Bloomberg (Bob Ivry): "A European bank that received the most Federal Reserve discount window help during the financial crisis also took $381 billion in aid from its home countries... Details of Fed lending released last week show that Dexia SA, based in Brussels and Paris, borrowed as much as $37 billion... 'If Dexia went bankrupt, it could have been a catastrophe for municipal finance and money funds," said Matt Fabian... senior analyst and managing director at Municipal Markets Advisors... Dexia... said its loans from the European Central Bank peaked at 122 billion euros ($173 billion) in October 2008. That month, it also received about $200 billion in debt guarantees and $8 billion in cash infusions from Belgium, France and Luxembourg. The bank availed itself of other Fed lending programs too. Its total borrowings from the U.S. central bank's Commercial Paper Funding Facility ranked third among users of the emergency program... Dexia used the program 42 times for a total of $53.5 billion... Dexia also tapped the Term Auction Facility, the lending mechanism the Fed established in December 2007 to augment the discount window. Dexia received 24 TAF loans totaling $105.2 billion..."

Currency Watch:

The U.S. dollar index dropped 1.3% to 74.86 (down 5.3% y-t-d). On the upside for the week, the Brazilian real increased 2.4%, the New Zealand dollar 2.0%, the Norwegian krone 1.9%, the Swiss franc 1.9%, the Danish krone 1.7%, the euro 1.7%, the Australian dollar 1.7%, the British pound 1.7%, the Swedish krona 1.5%, the Taiwanese dollar 1.1%, the Mexican peso 0.9%, the South African rand 0.9%, the Canadian dollar 0.8%, the South Korean won 0.8% and the Singapore dollar 0.3%. On the downside, the Japanese yen declined 0.8%.

Commodities and Food Watch:

April 8 - Bloomberg (Whitney McFerron and Jeff Wilson): "Corn stockpiles in the U.S., the world's largest grower, are plunging to a 15-year low and may be smaller than the government forecast last month as rising demand from makers of feed and ethanol drive prices higher... About 40% of the crop is used to make ethanol as the government subsidizes the fuel additive and retail gasoline nears $4 a gallon."

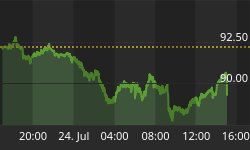

The CRB index jumped 2.0% (up 10.8% y-t-d). The Goldman Sachs Commodities Index surged 3.9% (up 20.3%). Spot Gold jumped 3.2% to a record $1,475 (up 3.8%). Silver rose 7.6% to $40.61 (up 31%). May Crude jumped $4.85 to $112.79 (up 23%). May Gasoline gained 3.5% (up 33%), while May Natural Gas dropped 7.4% (down 8%). May Copper rallied 5.7% (up 1.4%). May Wheat jumped 5.0% (up 0.4%), and May Corn rose 4.3% (up 22%).

China Bubble Watch:

April 5 - Bloomberg: "China raised interest rates for the fourth time since the end of the global financial crisis to restrain inflation and limit the risk of asset bubbles in the fastest-growing major economy. The benchmark one-year lending rate will increase to 6.3% from 6.06%... The one-year deposit rate rises to 3.25% from 3%."

April 5 - Associated Press (Kelvin Chan): "When millions of workers didn't return to their southern China factory jobs after Lunar New Year holidays, a turning point was reached for foreign manufacturers scraping by with slim profit margins. Companies were already under pressure from rising raw material costs, restive workers and lower payments for exports because of a stronger Chinese currency... Some 30 to 40 percent of migrant workers didn't return to their factory jobs in Guangdong province's Pearl River Delta manufacturing heartland after the annual Lunar New Year holiday in February, said Stanley Lau, deputy chairman of the Hong Kong Federation of Industries. Typically the proportion is 10 to 15%. That was despite Guangdong authorities raising minimum wages by up to 20% in March."

April 7 - Bloomberg: "Shanghai's population reached 22.2 million people in 2010, the Shanghai Population and Family Planning Commission said... Shanghai had 19.2 million residents in 2009..."

April 8 - Bloomberg: "Walt Disney Co. and its state-owned China partner will invest about $4.4 billion building a resort in Shanghai, the entertainment company's second amusement park in the world's most-populous nation."

Japan Watch:

April 7 - Bloomberg (Kana Nishizawa, Satoshi Kawano and Masaki Kondo): "Japan's bond market has ground to a halt since the March 11 disaster devastated the nation's northeast, as relative borrowing costs more than doubled. Only one company... tested the market in the last three weeks."

April 7 - Bloomberg (Mayumi Otsuma): "The Bank of Japan unveiled a lending program to help companies in areas affected by the nation's record earthquake, while voicing concern the disaster may depress economic growth in coming months. The BOJ unveiled the 1 trillion yen ($12 billion) facility as board members downgraded their economic assessment for the first time since October."

Asia Bubble Watch:

April 5 - Bloomberg: "Vietnam will increase the minimum wage by 14% next month, raising concern that higher labor costs may fan inflation that is already at a 25-month high."

Latin America Watch:

April 4 - Bloomberg (Frederik Balfour): "Embraer SA, the world's fourth- largest planemaker, expects China's private-jet fleet to expand 10-fold in a decade driven by economic growth, increasing numbers of millionaires and eased regulations. 'There is a huge growth engine for business-jet demand,' Luis Carlos Affonso, the planemaker's executive vice president...jets... The number of business jets in China will rise to 500 from about 50 in 10 years, he said... Makers of business jets, super cars and luxury yachts are all boosting their presence in China as the nation's about 10% economic growth rate spurs demand for high-end goods."

April 7 - Bloomberg (Eliana Raszewski): "Argentina's central bank is stepping up sales of peso-denominated bonds to slow money supply growth and curb inflation that economists say will quicken to 30% this year."

U.S. Bubble Economy Watch:

April 8 - Bloomberg (Ilan Kolet): "U.S. pet owners beware: the cost of feeding your animal is set to surge in coming months, following the rise in your own food bill. ... changes in the food component of the consumer price index have led movements in pet food costs since 2006. In 2008, pet food prices jumped by 16% after human food inflation reached 6%."

Real Estate Watch:

April 7 - Wall Street Journal (Kris Hudson and Miguel Bustillo): "Even as the economy picks up steam, many of the nation's malls and shopping centers are suffering a hangover due to changing consumer habits and the fallout from a massive building boom. Mall vacancies hit their highest level in at least 11 years in the first quarter, new figures from... Reis Inc. showed. In the top 80 U.S. markets, the average vacancy rate was 9.1%, up from 8.7%. The outlook is especially bad for strip malls and other neighborhood shopping centers. Their vacancy rate is expected to top 11.1% later this year... the highest level since 1990."

April 6 - Bloomberg (Hui-yong Yu): "U.S. apartment vacancies dropped to the lowest in almost three years in the first quarter as the weak homebuying market fueled demand... according to Reis Inc. The vacancy rate declined to 6.2% from 8% a year earlier and 6.6% in the fourth quarter..."

April 5 - Bloomberg (Hui-yong Yu): "Office vacancies in the U.S. dropped for the first time in more than three years in the most recent quarter and rents climbed, signaling the market is beginning a recovery as the economy improves. The national vacancy rate fell to 17.5% in the first quarter from 17.6% in the previous three months, Reis Inc. said..."

April 5 - Bloomberg (David M. Levitt): "Manhattan office leasing reached a four-and-a-half-year high in the first quarter as tenants sought to complete deals before rents climb further, according to... Cushman & Wakefield Inc... Rents sought by landlords rose for the second straight quarter after more than two years of declines, to an average of $54.73 a square foot."

Central Banking Watch:

April 5 - Bloomberg (Monika Rozlal): "Poland's central bank raised interest rates for the second time this year to damp inflation expectation... The Monetary Policy Council lifted the... rate by a quarter-point to 4%..."

Diverging Monetary Policies, Again

The ECB raised rates 25 bps this week to 1.25%, their first rate increase since July 2008. ECB President Trichet cited heightened inflation risk as justifying the move. At 2.4%, Eurozone inflation has meaningfully surpassed the disciplined ECB's 2.0% threshold. Crude ended the week near $113 and Gold closed at a record $1,475. With the Goldman Sachs Commodities Index already up 20% in 2011 (trading back to the highest level since 2008), there's little doubt at this point that inflation pressures are building up throughout the pipeline.

Our central bank is content to disregard energy and commodities prices. The plan, appearing at this point rather carved in stone, is to dismiss the "transitory" nature of current inflationary pressures, while sticking steadfastly to further accommodation for an "extended period." "Unacceptably high unemployment," "dual mandate," "low resource utilization," and so on. And the so-called "hawks" can squawk about until the cows come home, as markets pay heed only to Team Bernanke/Dudley.

Many - including individuals within the Fed - have criticized the ECB's move to tighten (to 4.25%) in the summer of 2008. Some have gone so far as to argue that the ECB tightening helped to precipitate the global financial crisis. Yes, the ECB tightened with crude oil about $140 a barrel (and 4% consumer price inflation)- and within weeks oil and commodities markets were in free-fall. The consensus view is that the Fed was on the right side of divergent monetary policy in 2008, having aggressively slashed rates to 2% by April. Our central bank was certainly emboldened by the whole experience.

With the ECB signaling a rate increase and Chairman Bernanke fully committed both to "QE2" and an "extended period" of extreme monetary accommodation, for some weeks now the markets have been grappling with divergent monetary policies. Reminiscent of 2008 dynamics, the markets view easy "money" from the Fed trumping all efforts by others to pour a little less of the good stuff in the punchbowl. And, really, with most global central bankers around the world at least attempting to return to a more normalized monetary stance, today's policy divergence is essentially between the U.S. and the rest of the world.

Markets, however, are keen to maintain their one dimensional focus on aggressive Fed accommodation - and the outpouring elixir of dollar weakness - as the key mechanism ("Monetary Process") spewing finance out to further inflate global asset/commodities prices. In the current configuration of global financial flows and speculative dynamics, there is no real tightening with the Fed locked at zero. China, Brazil, and India, for example, can hike rates - and then rush to sound the hot "money" tsunami alert.

The need these days for the ECB to adjust its level of accommodation seems obvious (although the majority of analysts would disagree). Appreciating that analysis is much easier in hindsight than it is in real time, I do believe the ECB made the right call at the time to slightly firm its policy stance in 2008. Akin to this week's move, it wasn't a big deal. Besides, both market environments beckoned for a show of restraint. And, importantly, when circumstances changed, the ECB adjusted. European central bankers began cutting rates aggressively in early October and had reduced the target rate to 1% by May 2009.

Monetary policy tightenings are easily reversed - and an aggressive easing is easily implemented. But the "asymmetrical risk" issue is alive and well. As we are witnessing - once again - with our central bank, it becomes extremely difficult to reverse course away from loose policy. Any aggressive move away from accommodation is completely out of the question. And, to be sure, the lower and the longer the price of finance is held down, the more problematic the inevitable readjustment.

When the Fed unexpectedly slashed the discount rate in August 2007, the markets correctly interpreted the move as the beginning of an aggressive easing cycle. Forget subprime, the faltering mortgage Bubble and housing fragility, there's easy money there for the making. The Goldman Sachs Commodities Index began what would be a fateful 10-month rally that would see an almost 80% price surge, powered by a doubling in the price of crude. Equities rallied strongly around the world, while the dance party took it up another notch throughout M&A and leveraged lending.

It is simply not credible analysis to disregard the role Fed policy had on inciting excesses including a powerful speculative rally encompassing global risk markets. In particular, a liquidity onslaught coupled with a weak dollar fomented a highly speculative and destabilizing market surge. The eventual 2008 bursting of this speculative bubble - with atypically tight loss correlations across asset classes - coincided with the collapse of confidence in structured finance, ensuring the worst financial crisis in decades. In a lesson regrettably left unlearned, policymaking that spurs a cycle of speculative leveraging lays the foundation for eventual de-risking, de-leveraging and liquidity crisis.

So, here we are again. Fed policy has once again proved instrumental in inciting a commanding speculative Bubble throughout global risk markets. One heck of a party has broken out in leveraged finance and global M&A. And, again, there's nothing like bountiful price gains to encourage participants to disregard underlying structural issues and fragile underpinnings. Worse yet, the sophisticated speculators take great comfort that deep structural maladjustment ensures ongoing monetary accommodation. Sure, the ECB lifted rates a little. Yet, everyone knows that European periphery structural debt issues will hold meaningful tightening at bay. Here at home, the unfolding fiscal train wreck guarantees that the Fed perpetually extends the "extended period."

This is a dangerous period. Global liquidity is way too plentiful, while speculation has become too all-embracing and rewarding. Indications of monetary excess are everywhere. Indeed, we're in the midst of the biggest financial Bubble in history (the "Global Government Finance Bubble") - yet everyone seems comfortably oblivious. The Fed will persevere with its doctrine of ignoring asset prices, government borrowing excesses, market distortions and rampant speculation. These don't, after all, even enter into their policy framework. The Fed is also determined to disregard increasingly entrenched inflation dynamics, convinced that its interest rate policy, quantitative easing programs and dollar neglect aren't behind the upsurge in commodities prices. Amazingly, the Fed likes what it sees and, much to the markets' liking, clearly prefers to stay the course.

Throughout the marketplace, few discern inflated asset prices - certainly nothing indicative of some "great" Bubble. Bond prices appear reasonable, at least in the context of perceived benign "core" consumer price inflation and rock-bottom short rates. The collapse in junk and corporate risk premiums is thought justified by the robust corporate sector balance sheet and healthy cash-flows. To many, stock valuations look cheap in relation to buoyant corporate earnings. And, in line with the Fed's viewpoint, rising energy and commodity prices are reflective of the health and ongoing expansions in the "emerging" economies. Others obviously see things differently, but I see trouble all around in the rather covert effects the current Credit Bubble is exerting upon global risk markets and economies.

Where would U.S. incomes, earnings and corporate cash-flows be today if it weren't for the $4.5 TN increase in federal debt over the past 10 quarters? Ponder for a moment the liquidity backdrop in the Treasury market had the Fed not intervened in the marketplace with quantitative easing (#1) and "QE2" - in the process convincing the marketplace that the Fed had committed to operating as a reliable market "backstop bid?" What would be the state of the household balance sheet today if not for the unprecedented fiscal and monetary policy response? Is it sound analysis to trumpet the pristine state of the corporate balance sheet and celebrate the improving household balance sheet - when the Fed is doing unconscionable things to its balance sheet and the federal government is in the process of destroying theirs? How would global markets and economies be functioning these days had it not been for the almost $1.6 TN increase in international central bank reserve holdings over the past 12 months - or the $2.75 TN, 40%, growth in two years, to $9.45 TN?

Today, ECB President Trichet stated that "it is important that the dollar is a strong currency." He also said that "fixing imbalances must focus on deficit countries." To this day, Greenspan argues that foreign central bank Treasury purchases were instrumental for the rate environment that inflated our nation's housing Bubble. And the argument that our trading partners - and their undervalued currencies and steady accumulation of American I.O.Us - are most responsible for global imbalances will not be resolved anytime soon.

Let the world adjust; just ensure that the Fed keeps doing what it's doing. And I just scratch my head in disbelief at how little we've allowed ourselves to learn over a turbulent 20 year period of interplay between "activist" policymaking and serial market Bubbles. After doubling mortgage Credit in seven years, our system is now on track to double federal debt in 4 years. And the markets couldn't be more pleased with it all. It leaves one pondering what type of circumstance will be necessary to finally force us to start getting our house in order - to return to some semblance of disciplined central banking and fiscal responsibility.