Appears Scotty got it wrong again. We said to beam us up, and he beamed us back. All of a sudden we seem to have returned to 2008. Perhaps, though, we should not be so tough on Scotty. The Federal Reserve had a hand on the controls too, continuing the longest running stretch of asset price distortions in all of history. Think of 97-year-old sports team with one winning season, 1953.

All around signs of the reemergence of 2008 are evident in many measures and indicators. (See Alan Abelson, Barron's,11 April 2011.) But the most insidious reincarnation by the Federal Reserve is with hedge funds. Apparently, the only beneficiary of Federal Reserve policy is the workforce at hedge funds. From in "Hedge funds surge to peak of $2,002bn in managed assets," Financial Times by S. Jones & D. McCrum, 20 April 2010, we read,

"Assets under management in the global hedge fund industry soared to an all-time peak, surpassing the pre-crisis high thanks to the strongest investor inflows in years."

"That comfortably exceeds the $1.930bn peak of June 2008, just months before the collapse of Lehman Brothers..."

Per the article, the low point was $1,330bn at the beginning of 2009. In about a year, hedge fund assets have risen ~$700 billion. Note that is billions with a "b". Are your mutual funds and house back to the June 2008 values?

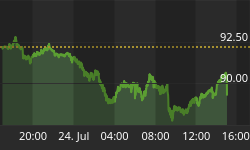

In the speculative era leading up to the 2008 debacle funds bought mortgage and debt bombs before moving on to commodities. This time, they skipped the debt bombs and went right to commodities. Part of the action also includes a massive bet against the U.S. dollar. Yes, we did read on the internet that the dollar was going to zero. We also read there that UFOs are really really real. In the chart below footprints of that massive bet can be observed.

That bet against the dollar has resulted in another massive set of price distortions, Around the world, nations are being punished by the Federal Reserve's irresponsible devaluation of the dollar. Silver has been pushed into a massive speculative bubble. Oil, despite no apparent shortage, continues to trade recklessly higher.

But, note the trend line in the above chart. We know several things about trend lines, especially obvious ones. They do not last forever. All trend lines are broken ultimately. Otherwise, we would still all own railroad bonds.

Dollar will walk through that trend line, as is always the case, and it will do so from one of the most oversold conditions it has ever experienced. When we read, on the source of all truth the internet, that U.S. Treasury debt is worthless, we can safely assume a fantasy induced delusion is widespread. We know not the catalyst for this move. Perhaps it will be the recognition that the reign of economic terror by the Obama Regime will indeed end. Could the Jasmine Revolution spread to China?(See Financial Times, 23 April, "Fuel price strike rattles Beijing", and watch the price of rice.)

How does one protect wealth from Hedge Fund Debacle II, brought to you by the friendly elves in the Federal Reserve tree? While the price of $Gold is at risk due to the massive one-sided bets by hedge funds, it will remain an important core asset in the decade ahead. Non dollar Gold investors will be better served as their currencies will likely depreciate.

Silver, however, is certainly an asset to avoid as it has become the "internet stocks" of 2011. Investing in buckets of white sand stored in the basement might provide a higher return. Going to Las Vegas and betting on red every spin might be an alternative. Better odds, and free drinks.

Switching some of your risky Silver holdings into Rhodium should certainly be considered. Covariance on these two metals should be quite low to negative in the future. See our comments in "Rhodium Trading Thoughts."

Another opportunity that investors may want to consider is one that did not much exist a year ago. Chinese government has been moving persistently over the past year to make the Renminbi more available to non Chinese investors. Increasingly available are means of investing in the Renminbi. In terms of its development curve, China is at about the equivalent of 1915 for the U.S. That was about the beginning for the U.S. dollar's rise to global reserve asset dominance.

When 1971 opened, the Yen/$ ratio was 358:1. In 1995 it was 84:1. That appreciation produced a return in excess of 300% to U.S. dollar-based investors. Similar results seem reasonable for the Chinese Renminbi in the future. See valuation below. We do note that such an investment would not be void of short-term risk. The Chinese economy will have bumps and grinds, as their leaders put their pants on the same way as Westerners.

On another matter, we have noted much discussion on the shape of price curve for contracts for future delivery. Misunderstanding of the meaning of the price curve for contracts for future delivery of a commodity seems high. While the markets for all commodities are somewhat unique, the structure of the price curve for contracts for future delivery possesses mathematical characteristics that produce fairly specific conclusions. Shape of the price curve is not open to creative analysis to support one's investment ideology. For that reason, we have been writing on the subject. That effort can be accessed at: http://valueviewgoldreport.com/files/FUTURES_2011_B.pdf

| US$GOLD & US$SILVER VALUATION Source: www.valueviewgoldreport.com | ||||||

| US$ GOLD | US$ GOLD % | US$ / CHINESE YUAN¹ | CHINESE YUAN % | US$ SILVER | US$ SILVER % | |

| CURRENT | $1,512 | $0.1533 | $48.00 | |||

| SELL TARGET | $1,970 | 30% | $0.5000 | 226% | $35.00 | -27% |

| LONG-TERM TARGET | $1,818 | 20% | $0.3330 | 117% | $33.00 | -31% |

| OVER VALUED | $1,113 | -26% | $20.25 | -58% | ||

| FAIR VALUE | $856 | -43% | $15.60 | -68% | ||

| ACTION | Gold preferred to Silver. | Buy Chinese Yuan | Sell Silver Sell Silver Sell Silver | |||

¹ These estimates are preliminary, and subject to change.

GOLD THOUGHTS come from Ned W. Schmidt,CFA,CEBS as part of a joyous mission to save investors from the financial abyss of paper assets, and the great Silver fiction. He is publisher of The Value View Gold Report, monthly, and Trading Thoughts. To receive these reports, go to: www.valueviewgoldreport.com