Soft money works. Just ask the Swiss central bank...

Time was, the past was another country, as L.P.Hartley wrote in The Go-Between. Because "they do things differently there."

Thanks to the shipping container, fast-food, Facebook and the academic conference circuit, however, foreigners all do and think and wear pretty much the same things these days. Whereas the past has jumped into a parallel universe...

"No central banker could regard as successful a year in which the value of money fell by as much as 8% in terms of what it will purchase at home, and by 10% in terms of overseas currencies."

So wrote the governor of the Bank of England, then Robin Leigh-Pemberton, in 1990. Ain't it sweet?! Central-bank chiefs everywhere, it seems, would now give their left arm to bring about such a disaster today. Indeed, Leigh-Pemberton's current successor, Mervyn King, managed a 24% drop in Sterling's trade-weighted value in 2008. But still King couldn't get domestic inflation above 6.2% at its peak that year. It's taken until now, spring 2011, for record-low interest rates to get retail-price inflation - excluding housing - up to nudging 6.3% annually.

What's a policy-wonk got to do to beggar his countrymen, let alone his country's neighbors?

"At full employment, a strong Dollar is good for standards of living...But in a depressed economy, it isn't so clear that a strong Dollar is desirable."

Yes, Christina Romer may not be chair of the president's Council of Economic Advisers anymore. But writing here in the New York Times, the Berkeley economics professor is still making plain Washington's aims.

"A weaker Dollar means that our goods are cheaper relative to foreign goods. That stimulates our exports and reduces our imports. Higher net exports raise domestic production and employment. Foreign goods are more expensive, but more Americans are working. Given the desperate need for jobs, on net we are almost surely better off with a weaker Dollar for a while."

Trouble is, everyone else wants a weak currency too. Or at least, everyone with their mitts on the levers and dials of monetary policy. Savers, retirees...even wage-earners - apparent beneficiaries of the Soft Money Consensus - are all beginning to wonder what good is inflation if your income doesn't inflate faster still.

No matter. "The Euro, which has too weak [economic] growth, is at too high a level," declared French president Sarkozy at a dinner in London in March 2008, taking his cue from the Airbus aerospace giant's constant carping. The single currency had just hit record highs at $1.60, but even down at $1.43 some 20 months later, the Euro still needed "a strong[er] Dollar" said Eurozone central-bank chief Jean-Claude Trichet. That was "very important" - almost as important as knowing that "the Euro is too strong today" at $1.40 as the currency zone's finance-group chairman, Jean-Claude Juncker, said in Oct.2010.

Roll on another 3 months to Jan. 2011, and guess what? Trading down at $1.30, "it is still too high," said Sarkozy, again citing Airbus and vowing to beat "monetary dumping" during his presidency of the G20 economic meetings. Whipping back through $1.40 again this month, however, "the Euro is too strong" said European Union president Herman Van Rompuy in May 2011.

You might, therefore, expect Eurozone politicians to welcome the latest phase of the currency union's rolling crisis. Last spring's disaster took the Euro down to 4-year lows beneath $1.19, and we can't recall anyone saying the Euro was too strong back then. With Greece, Ireland, Portugal and now Greece again lining up for injections of central-bank and taxpayers' cash, any further rate hikes by the "inflation vigilantes" of the European Central Bank would be suicidal (literally so if the executive plan any holidays to Greece or Iberia this summer). Even the worms and vultures of the financial markets are to be thanked, you'd think, for helping drive the single currency lower by selling it for Dollars, Sterling, Yen and - tastiest of all - Swiss Francs.

"The Swiss National Bank's hands are tied," reckons one forex trader interviewed by the Wall Street Journal. "They were heavily criticized for their [2010] interventions and so fresh interventions are very unlikely."

Fill your boots, in short. Because there's to be no repeat of Berne creating Francs and dumping them into the currency market. Well, not unless "the situation in the currency markets leads to deflationary risks," as SNB deputy-chief Thomas Jordan assured Swiss radio listeners yesterday. "Monetary policy must always respond to the inflation outlook," he repeated on Swiss TV's Eco show later on Tuesday.

"If inflation risks are on the rise, we will have to raise interest rates more quickly," Jordan added. (That sloshing noise you can hear is yield-starved investors salivating the world over.) But "if the situation is such that inflation risks are low, then interest rates can stay low relatively long."

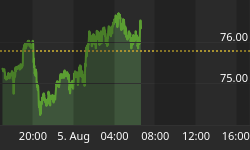

Still, the Franc today hit new Euro highs - breaking the €1.23 mark and perhaps heading for "verbal intervention" by the Swiss National Bank, according to forex pundits - after the Organization for Economic Cooperation and Development backed the sometime-in-2011 rate hike mooted recently by SNB president Phillip Hildebrand.

"Monetary policy rates will have to rise gradually from 2011 onwards to damp inflationary pressures from domestic demand growth," said the OECD, "but most importantly [wait for it...] to avoid overheating in the housing market." Hildebrand himself warned in April month of "imbalances with serious repercussions" if interest rates stay at a "very low level for a long time." The month before, the SNB said real-estate prices deserved their "full attention".

Even the government has hinted that a rising Franc might not warrant quantitative easing, Swiss-style, part deux. The SNB's forex intervention of spring 2009 to summer 2010 quadrupled the central bank's balance-sheet to $207 billion. (That includes the outright loss of $15 billion on selling the rising Franc to buy a falling Euro.) But economy minister Johann Schneider-Ammann told business leaders at last week's Swiss Economic Forum in Interlaken that "The strong Franc is creating many concerns, but we have to learn to live with it, want to live with it."

Of course, raising interest rates "would [only] be the beginning of a normalization," as one Zurich wealth manager puts it. Rates are sitting at 0.25% per year after all, and Swiss savers might not even get to 0.50% if the nation's exporters get their way. Total Swiss exports rose almost 10% in the first quarter from the same period last year. Machinery and electrical engineering sales leapt by 27%. But "many companies have already started to implement measures against the strong Franc," warns industry-group Swissmem's spokesman Ivo Zimmermann. "The renewed rise could prompt some companies to cut jobs or move investments out of Switzerland."

Soft money works...or so the Swiss example will no doubt be taken to prove...just as policy-makers in Italy, Spain, Portugal and Greece kept repeating throughout the 1970s, and then kept practising for 20 years after. Euro accession put a stop to that (as London had long guessed, staying well out of monetary union) but even the European Central Bank in Frankfurt must see the 21st century spin on the devaluation trick: If you want to roar back out of recession, make sure your money is softer than everyone bar the US and Japan first. (You can't be softer than them, because they're stuck at zero.)

At least, that's the lesson which central bankers will take from a baby-step hike - or the mere refusal to actively devalue the Franc by printing and selling it - by the "hard money" Swiss National Bank. Truly a world upside down, and hardly a race away from the bottom just yet.