You may panic.

You could drown.

Or you can ride them out through the breakers.

Appropriate for the season - the rip currents have been everywhere this summer. The only part of the analogy that doesn't fit for me is they typically form after the storm has passed.

Was that it?

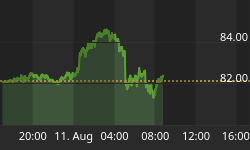

If the proxy horseman of Apple is any indication of what's to come in the overall equity markets (i.e what looked like a major distribution was actually just another consolidation) - well then Mr. Soros cash hoard may prove to be a rather atypical contrarian indicator. I suppose if this proves prescient, the recency effect will be seen to not discriminate its prejudice of perspective, even with the macro-guru billionaire crowd - and especially during a precursory round of sovereign debt travails.

Of course as indicated by the ever resourceful hand of sentiment and data mining extraordinaire, Jason Goepfert, the last time in the past 15 years that Apple closed at a 52 week high on earnings was October 23, 2007. Slim pickens with the data set - but that year keeps coming back around in haunting echos...

What has caused great confusion and debate in the macro community is the perception that the US dollar looks to be basing nicely and poised to run higher - perhaps substantially so. How that dynamic and kinetic relationship will fit into the equity and commodity markets will be a key component in getting the second half right.

Looking at a few dollar correlation charts from the data sculptor, David Stendahl, you may just find some clues.

One possible scenario based on these correlation charts is the dollar's inverse relationship to the equity markets will weaken - allowing the dollar to rise in concert with the market. The inverse would likely manifest in the precious metals markets with a strengthening degree of influence by the US currency.

This has long been my standing opinion in my notes - the question was how turbulent the equity markets would be affected by this changing dynamic.