The Bank of England meets tomorrow morning, with rates already sitting at 0.50%. The ECB also meets, with the policy rate at 1.50%. Today, the Swiss National Bank got a jump on both of those bodies by cutting the National Bank Libor target from 0.25% to "as close to zero as possible" (sub-zero rates are possible, but policymakers usually ignore the messy reality that conflicts with theory), and also increased the amount of reserves independently fromthe rate move.

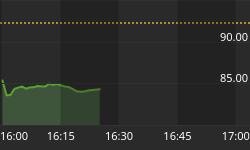

This move was undertaken partially to weaken the Swiss Franc, which as a safe-haven currency has been screaming higher against both the Euro and the dollar. It worked - slightly. What"s 25bps compared to the prospect of losing everything?So the Swissy bounced, but as the chart below shows it was less than impressive.

The Swiss National Bank ease caused a tiny bounce in Euro/Swiss.

Incidentally, I wasn"t kidding about sub-zero rates. When the alternative is a large capital loss, investors will willingly accept negative rates. In the credit crisis, T-Bill rates went negative partly because large investors who were not covered by FDIC insurance preferred to own bills at negative rates rather than risk losing money in bank depository accounts. The SNB could offer negative interest rates (you pay us to keep your money here) and money wouldstill flow into the franc. And it should do so.

It"s hard to believe that the ECB has recently been in tightening mode, but indeed at the very last meeting that august body (which probably had a very different feel from the body this August) actually hiked rates. I screamed and kicked my feet in July when they did so, protesting (in one of my favoriterecent passages):

"However, a worrier doesn"t have to look very far to find worries (and a bull doesn"t have to look very far to find a wall to climb). Rate hikes into a sovereign debt crisis would be a good place to start, although at the same time the ECB suspended its minimum credit-rating requirements for Portugal so it is strangely being both tight and loose at the same time.

"The general loss of ECB credibility could be a worry, although to me the whole institutionalized crazy routine makes me think more of the scene in Blazing Saddles where the sheriff pretends to be taken hostage by his own split personality, in order to manipulate the crowd. I don"t think the manipulation routine in this case is working very well, but I just prefer to believe that over the alternative that Trichet has simply gone mad. Today he insisted that the Irish government, which recently has threatened to force senior bondholders in the country"s banks to take losses as a way of 'sharing the burden," should instead respect prior agreements. "All the plan, nothing but the plan including all what has been said at the time of the approval of the plan," quoth Trichet expansively, apparently numb to the dramatic irony of demanding utter fidelity to precedent on one hand while rewriting collateral guidelines with the other hand."

I can hardly imagine that the ECB would seriously consider hiking rates again, although it is true that they can raise rates all they want if they splash the world with liquidity at the same time. But the ECB has already demonstrated a certain ... how do you say ... sangfroid? A misplaced and dangeroussangfroid, indeed, but style counts for something, right?

Assuming that the ECB joins the SNB, BOJ, BOE, and Fed back in the easy-money fold, it has implications for inflation even if it has scant implications for the deferral of the crisis. Inflation, after all, doesn"t just come from the Fed. It comes significantly from the existence of too much money globally. Much of domestic inflation in the U.S., the U.K., Europe, or any of the major connected countries is sourced from these global factors. Only the ECB hasn"t been blatantly easing recently (and even there I guess it is hard to argue it is being terribly tight since after all it is lending moneyagainst Greek debt and baseball card collections).

Here"s an interesting note for U.S. readers who may have been myopically focused on the debt ceiling negotiations. Notes from dealers in Europe today described in various ways the "extreme risk aversion" that is starting to take place. I can"t describe anything we have seen here in the U.S. as "extreme risk aversion" (a 7% equity selloff, even concentrated in 2 weeks, doesn"t exactly qualify as "extreme" anything). On these shores, at least for those of us not working directly for a Wall Streetbank, we don"t yet get the growing sense of panic over there.

But it is beginning to be felt. The chart below shows 1-month LIBOR marks. Notice that the scale tends to exaggerate the move, which has only been so far a couple of basis points - but it is a turn higher and something to keepan eye on.

One-month LIBOR may be on the move, signaling funding pressure growing inthe U.S.

Volume is also sometimes a measure of stress. Today"s equity volume was again heavy (by 2011 standards). Actually, it was heavier than yesterday"s, although that is largely because of the trading before lunchtime when the S&P had broken through important support on a surge in volume. Equities managed an0.50% gain, and nominal bonds were unchanged.

There was talk that equities rallied because the Fed might be considering QE3. But TIPS and commodities were both weaker, TIPS significantly so as 2-year TIPS yields rose 18bps and 10-year TIPS yields rose 9bps to 0.35%. Thus, the talk that the market rallied because the Fed might do QE3 sounds hollow to me - if investors thought the Fed was readying QE3, wouldn"t commodities and TIPS improve? So I"m skeptical (quite aside from the improbability of a meaningful QE3). I think the equity bounceis just that: a bounce.

The data today, in fact, was less than a disaster. It wasn"t great, to be sure, but the ADP figure was a teensy bit above expectations at +114k and while the ISM Non-Manufacturing number slipped to 52.7 from 53.3, that wasn"t nearly as bad as the Manufacturing ISM on Monday. It"s not like we"re out of the woods, but after doing significant technical damage this morning on heavy volume itisn"t a shock to me to see a lower-volume bounce.

But the technical damage is significant. While I covered about 40% of my short positions (long put options) today, I expect to see lower equity prices in the near future. A weak Initial Claims figure tomorrow (Consensus: 405k from 398k) could be the catalyst, since traders tend to exaggerate the Claims figure that comes out right before Employment. But the piper is still calling the tune from Europe, and with two monetary policymaker meetings scheduled the tone for trading is more likely to be set before the New York open.