Below is an excerpt from a commentary originally posted at www.speculative-investor.com on 21st August 2011.

The world of policy-making is dominated by Mercantilism and Keynesianism.

Under the Mercantilist way of thinking, the greater the level of goods exports relative to goods imports, the better. Or, looking at it from another angle, from the perspective of a Mercantilist a good policy is one that maximises the amount of money flowing into the country by maximising the amount of goods flowing out of the country.

Under the Keynesian way of thinking, spending drives the economy and recessions happen when mysterious forces -- sometimes called "animal spirits" -- cause spending to fall by too much. A great example of the Keynesian way of thinking is Paul Krugman's recent claim that the global economy would be shifted onto a sustainable upward trajectory if the governments of the world began preparing for an alien invasion that never happens. The idea that an economy can be helped by consuming a huge amount of resources in a totally wasteful manner is consistent with Keynesian economic theory.

It's not surprising, then, that a strong currency is anathema to most policy-makers. Currency strength will make life more difficult for goods exporters in the short-term, which is the only term that matters to most politicians, and persistent currency strength will tend to promote saving. In the real world, saving is the cornerstone of economic progress; but in the upside-down world of the Keynesian, more saving is bad because it means less immediate spending.

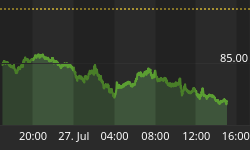

Due to the theories that guide their thinking, policy-makers will often panic if their currency achieves large gains against the currencies of their trading partners. For example, Swiss policy-makers recently began to show signs of panic in response to the Swiss Franc's performance relative to the euro. As illustrated by the following chart, the euro, which had been weakening steadily against the Swiss Franc for more than two years, commenced an accelerated decline at the end of June. At its low point earlier this month, the euro had lost about one quarter of its value against the Swiss Franc (SF) in only 4 months.

In response to the performance depicted above, some Swiss policy-makers and influential business leaders have recommended that the Swiss National Bank (SNB) immediately set a lower limit of 1.10 for the euro/SF rate and then gradually increase this limit over time. In other words, the suggestion has been made that the SNB do whatever it takes to firstly prevent the SF from strengthening any further and secondly reverse the SF's long-term upward trend.

We have some sympathy for Swiss exporters. It must be difficult to remain competitive when the currency in which your exports are priced weakens relentlessly against the currency in which most of your costs are denominated. However, any short-term solution that involves depressing the relative value of the SF is likely to have dire long-term consequences. The reason is that the only effective way to change the SF's trend is to greatly increase the supply of this currency.

The SF's value relative to the euro will fall if the SF supply is boosted to a sufficient extent, but the monetary inflation will promote widespread mal-investment and sow the seeds of an eventual economic bust. It could even sow the seeds of hyperinflation. The reason is that for the SNB to ensure relative weakness in the SF it will have to consistently inflate at a faster rate than the ECB, and the ECB could end up inflating rapidly as it desperately attempts to hold Europe's monetary union together by bailing out banks and other bondholders.

The world's monetary system appears to have degenerated to the point where there are no good options, meaning that economic hardship lies along every possible path. However, policy-makers could minimise the hardship by not entering, or withdrawing, from the 'race to the bottom' in which most currencies are presently engaged. This would be the best way to protect the savings that will be needed to fuel sustainable economic growth in the future.

We advise against holding your breath while waiting for the current gaggle of policy-makers to do the right thing.

We aren't offering a free trial subscription at this time, but free samples of our work (excerpts from our regular commentaries) can be viewed at: http://www.speculative-investor.com/new/freesamples.html