Richard Bove says Bank of America Has 'No Reason' to Raise Capital

Bank of America Corp. (BAC), the U.S. lender that lost half its market value this year, has sufficient capital to weather mounting costs tied to souring loans, said Richard Bove, an analyst at Rochdale Securities.

"Bank of America has so much cash on its balance sheet that it could pay back all of its short-term debt and a big chunk of its long-term debt," Bove said in an interview today on Bloomberg Television's "InBusiness With Margaret Brennan." "There's no reason for the bank to have to go out and raise capital whatsoever."

The firm fell as much as 6.4 percent in New York trading today and the cost to protect its debt from default surged to a record before retreating. Henry Blodget, the former Internet stock analyst turned blogger, wrote today on Business Insider that charges and loan costs may force the bank to raise as much as $200 billion.

"Mr. Blodget is making 'exaggerated and unwarranted claims,' which is what the Securities and Exchange Commission stated publicly when he was permanently banned from the securities industry in 2003," the Charlotte, North Carolina- based bank said today in an e-mailed statement.

Blodget, a former Merrill Lynch & Co. analyst, was banned for life from the securities industry after regulatory inquiries into how analysts touted stocks during the Internet boom. He was hit with $4 million in fines and repayments after watchdogs including the SEC faulted his reports on companies including go2.com. Merrill was acquired by Bank of America in 2009.

Fairest of the Fair Weather Fans

I am the fairest of the fair weather fans, in sports and in stock analysts. I like sports teams and stock analysts when they make the right plays and calls, and I criticize them when they don't.

When it comes to analysts, I do not care so much for the call itself as opposed to the reasoning behind it.

It takes time to rebuild teams and reputations. In my opinion, Henry Blodget has done just that. However, my opinion can change tomorrow because I appreciate common sense more than platitudes.

In this case, I side with Blodget and common sense. Reasonable opinions are by definition reasonable. Words and actions of 11 years ago must be discounted.

Bove attacks Blodget for things he said 11 years ago. I attack Bove for pathetic analysis today.

Which is more important?

Bank of America Tier One Capital Ratio 6 Percent

While pondering the above question, let's continue reading Bloomberg.

Bank of America had a Tier One capital ratio of about 6 percent as of June 2011 under the new rules recommended by the Basel Committee on Banking Supervision, according to an Aug. 9 note from Jonathan Glionna of Barclays Plc. The bank probably has until 2019 to reach 9.5 percent, the level required of the world's largest banks. That's enough time to bolster capital by selling assets deemed risky, Moynihan has said.

Lovely.

Bank of America is undercapitalized by huge amount by its own admission. It just wants until 2019 to straighten things out.

Moreover, Bank-of-America is counting on delays after delays after delays in rules requiring assets be marked-to-market.

Flashback March 29 2009: Mark-to-Market Lobby Buoys Bank Profits 20% as FASB May Say Yes

Four days after U.S. lawmakers berated Financial Accounting Standards Board Chairman Robert Herz and threatened to take rulemaking out of his hands, FASB proposed an overhaul of fair-value accounting that may improve profits at banks such as Citigroup Inc. by more than 20 percent.

The changes proposed on March 16 to fair-value, also known as mark-to-market accounting, would allow companies to use "significant judgment" in valuing assets and reduce the amount of writedowns they must take on so-called impaired investments, including mortgage-backed securities. A final vote on the resolutions, which would apply to first-quarter financial statements, is scheduled for April 2.

FASB's acquiescence followed lobbying efforts by the U.S. Chamber of Commerce, the American Bankers Association and companies ranging from Bank of New York Mellon Corp., the world's largest custodian of financial assets, to community lender Brentwood Bank in Pennsylvania. Former regulators and accounting analysts say the new rules would hurt investors who need more transparency, not less, in financial statements.

Officials at Norwalk, Connecticut-based FASB were under "tremendous pressure" and "more or less eviscerated mark-to- market accounting," said Robert Willens, a former managing director at Lehman Brothers Holdings Inc. who runs his own tax and accounting advisory firm in New York. "I'd say there was a pretty close cause and effect."

Mark-to-market rules were supposed to go into effect in 2007. Those rules were twice suspended. Now it seems they have been postponed indefinitely, if not scrapped altogether for the benefit of Citigroup and Bank-of-America.

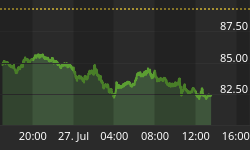

Where's There's Smoke There's Fire

Forget all that. It is irrelevant. Share price alone says bank of America is is deep s***.

Bank stocks do not plunge 58% in six months for nothing. They just don't. You are delusional if you think otherwise.

That chart says there is smoke somewhere, and fire underneath.

Bove Says Share Price Irrelevant

In a bloomberg interview Bove says ...

"There is no impact whatsoever on Bank of America's balance sheet, based upon the price of its stock in the open market. If the price of the stock goes to a penny a share, it has no impact on the balance sheet of Bank of America. Bank of America sells the stock to the public, it takes in the money, and that is the end of the transaction as far as Bank of America is concerned. If you're going to break a bank, you're going to have a run on its deposits. That's not happening. Exactly the opposite is happening...Deposits are pouring into Bank of America."

Technically that is an accurate assessment. Fundamentally it is nonsense. Deposits are flowing in everywhere because of what I call a "mad dash for cash".

I commented on that phenomenon in Bank of New York Mellon to Slap Fees on Big Deposits Following "Global Dash For Cash"; When was Hyperinflation Supposed to Start?

To equate deposits, which are actually a balance sheet liability, to fiscal strength is sheer incompetence, at best.

Moreover, I stand by my statement that bank stocks do not plunge 58% in six months for no reason. Thus Bove is in FantasyLand.

Will Bank of America Survive?

I said in 2007 that Citigroup would not survive in one piece, that dividends would be sliced (well before Meredith Whitney), and that it may not survive at all. It did survive but only because of a massive rescue effort by the Fed and taxpayers.

The same applies to Bank of America today. It will not survive in one piece, and that is not just my opinion, that is what the market implies.

I am willing to take a contrary position for a while as I have done many times regarding the stock market and treasuries. However, a 58% decline in share price of a bank stock is well beyond any reasonable contrary opinion.

Sadly Richard Bove attacks the messenger instead of paying attention to the message.

Richard Bove Calls

As long as Dick Bove is willing to dig into the distant past of Blodget, let's dig into the more recent analysis of Dick Bove.

- June 19, 2009: Citi 'too big to fail', will hit $12 a share: Richard Bove

- September 30, 2010: Dick Bové Gives Citi's Balance Sheet Two Thumbs Up

- May 5, 2011: Citigroup to Triple By 2013: Bove

In a perverse sense, Dick Bove was correct. Citigroup wildly exceeded his $12 price prediction. Sadly, I must point out that it did so after a 10:1 reverse split.

Split adjusted, on June 19, 2009, Bove predicted a share price of $120. On May 5, 2011 Bove called for Citigroup to triple. Let's take a look at how he did.

C - Citigroup Weekly Chart

Bear in mind, I am just investigating nonsense by Bove on Citigroup. Time does not permit investigation of other Bove fantasy predictions.

To be fair, I fully understand how difficult predictions are. However, Bove's Citigroup predictions are both wildly and consistently wrong in terms of both magnitude and direction.

Regardless of what you think about year 2000 calls, the far more important present shows that Richard Bove is a "bullshill" selling "bullsheet". Bove's credibility is zero.