Summary of Index Daily Closings for Week Ending November 19, 2004

| Date | DJIA | Transports | S&P | NASDAQ | Jun 30 Yr Treas Bonds |

| Nov 15 | 10550.24 | 3611.74 | 1183.82 | 2094.09 | 112^19 |

| Nov 16 | 10487.65 | 3572.19 | 1175.43 | 2078.62 | 112^15 |

| Nov 17 | 10549.57 | 3600.46 | 1181.94 | 2099.68 | 113^09 |

| Nov 18 | 10572.55 | 3612.22 | 1183.55 | 2194.28 | 113^21 |

| Nov 19 | 10456.91 | 3567.65 | 1170.34 | 2070.63 | 112^23 |

| SHORT TERM FORECAST (Next Two Weeks) | ||||

| TREND | PROBABILITY | Legend | ||

| Substantial Rise | Low | |||

| Market Rise | Medium | Very High | 80% | |

| Sideways | Medium | High | 60% | |

| Market Decline | High | Medium | 40% | |

| Substantial Decline | Medium | Low | 20% | |

| Very Low Under | 20% | |||

| INTERMEDIATE TERM FORECAST (Next 12 Weeks) | ||||

| TREND | PROBABILITY | Substantial | 800 points+ (DJIA) | |

| Substantial Rise | Low | Market Move | 200 to 800 points (DJIA) | |

| Market Rise | Medium | Sideways | Up or Down 200 (DJIA) | |

| Sideways | Medium | |||

| Market Decline | High | |||

| Substantial Decline | High | |||

This week the Dow Jones Industrial Average closed down 82.10 points, in line with last week's Short-term TII reading of negative (6.50). The DJIA hit a high for its rally from October 25th on our two Fibonacci phi turn dates, November 17th (intraday) and November 18th (closing) at 10,602 and 10,572 respectively. November 18th is 1,219 trading days from the January 14th, 2000 grand cycle top for the Dow Industrials. November 18th's phi mate is January 14th, 2003's top. That top was 753 trading days from January 14th, 2000, and the number of trading days from 1/14/03 to 11/18/04 was 466. This Fibonacci Golden Ratio comes by dividing 466 by 1,219 (a perfect Fibonacci .382 ratio), and by dividing 753 by 1,219 (a perfect Fibonacci .618 ratio).

The Dow declined from its intraday high Wednesday, through Friday, in submicro degree waves 1 down, 2 up, and 3 down. With equities overbought, it looks as though they are beginning a multi-week decline. This decline is critical to both the intermediate-term Bullish and Bearish cases. It will tell us clearly whether we have completed minor degree wave 5 of intermediate degree C of primary degree (2) from the October 2002 lows, or whether there will be a substantial intermediate-term rally into late winter/early spring 2005. Here's how we'll know: If prices (the DJIA) fall below October 2004's 9,708 low, then it is gang way below - we are deep into primary degree wave (3) down. If not, should prices not break below 9,708, then primary degree wave (2) is not over and 11,749 could be challenged. Should January 14th, 2000's 11,749 grand top be taken out, it would then mean grand cycle degree wave {IV} from the start of the Bull back in the eighties completed with the January 14th, 2000 to October 9th, 2002's decline, and the rally since then has completed primary degree waves (1) up (into February 2004) and (2) down (through October 25th, 2004). The move up from October 2004 through yesterday would then be minor degree 1 up of primary degree (3) up of grand cycle degree {V} up.

Coming Soon, in 2005, "Trader's Corner," a special feature for traders.

| Equities Markets Technical Indicator Index (TII) ™ | ||||

| Week Ended | Short Term Index | Intermediate Term Index | ||

| July 23, 2004 | (59.00) | (49.98) | Scale | |

| July 30, 2004 | 46.25 | (52.18) | ||

| Aug 6, 2004 | (38.00) | (50.40) | (100) to +100 | |

| Aug 13, 2004 | (15.75) | (49.03) | ||

| Aug 20, 2004 | 9.25 | (43.82) | (Negative) Bearish | |

| Aug 27, 2004 | 9.25 | (39.81) | Positive Bullish | |

| Sep 3, 2004 | (39.25) | (40.06) | ||

| Sep 10, 2004 | (49.25) | (45.78) | ||

| Sep 17, 2004 | (69.00) | (44.73) | ||

| Sep 24, 2004 | (52.25) | (42.02) | ||

| Oct 1, 2004 | 25.50 | (37.23) | ||

| Oct 8, 2004 | (58.50) | (35.56) | ||

| Oct 15, 2004 | (24.50) | (35.48) | ||

| Oct 22, 2004 | (15.00) | (36.93) | ||

| Oct 29, 2004 | 39.50 | (40.06) | ||

| Nov 5, 2004 | 5.50 | (35.28) | ||

| Nov 12, 2004 | (6.50) | (27.63) | ||

| Nov 19, 2004 | (50.00) | (23.18) | ||

While this latter scenario is possible, we don't believe that is what is happening here because primary degree (4) that would have ended October 2002 under that Bullish scenario didn't bottom with PE's under 10x - which has been the historical norm. Didn't even come close. Plus, the extraordinary pairings of phi mate tops and bottoms since January 14th, 2000 lends validation to the importance of that top. Should prices fail to drop below 9,708, but also fail to exceed 11,749 at the next rally, then the most likely scenario is we are completing primary degree (2) up, primary (3) down is next, and the grand top of January 14th, 2000 remains intact - we are in a grand cycle Bear market.

This week the Short-term Technical Indicator Index comes in at negative (50.00), indicating a decline is probable. Note: Black Friday's are usually up days. This indicator is a useful predictor of equity market moves over the next two weeks, both as to direction and to a lesser extent strength of move. For example, readings near zero indicate narrow sideways moves are probable. Readings closer to +/-100 indicate with a higher degree of confidence that an impulsive move up or down is likely over the short run. Market conditions can change on a dime, or the Plunge Protection Team can come in and temporarily stop market slides, so it may be unwise to trade off this weekly measured indicator.

The Intermediate-term Technical Indicator Index is useful for monitoring what's over the horizon - over the next twelve weeks. It serves as an early warning system for unforeseen trend changes of considerable magnitude. This week the Intermediate-term TII comes in at negative (23.18).

Getting back to our Fibonacci phi mate turn dates, the chart below shows that the next significant top or bottom is scheduled for February 13th, 2005. That date is 1,280 trading days from the validated important 11,722 closing price top in the Dow Industrials of January 14th, 2000. Every single top or bottom since that date - every one - has been either a .382 or .618 ratio of trading days from another significant top or bottom and January 14th, 2000. February 13th, 2005 is 489 trading days from the significant 3/11/03 bottom (a Fibonacci .382 relationship to 1,280 total trading days), while 3/11/03's bottom is 791 trading days from 1/14/00 (a Fibonacci .618 relationship to 1,280 total trading days).

What is interesting for the short and intermediate-term, is that the next turn date - February 13th, 2004 - is pretty far off, almost three months away. That doesn't mean we cannot see minor tops or bottoms along the way between now and then, but it does say the coming trend is strong. It could be that this next decline is a crash scenario, taking the majority by surprise - given the incredible bullish consensus right now - or perhaps the next decline will be shallow and short-lived, fail to take out October 2004's 9,708 bottom, and that the trend will be up through February 2005, wrapping up primary degree (2) up within the context of a Bear market that started in January 2000.

The Dow Industrials turned down like they meant business Friday after peaking Thursday 150.78 points below their 2004 high of 10,753.63. What is interesting here is that the DJIA has failed to confirm the recent 2004 higher highs of other major indices such as the S&P 500, the Transportation Average, and the NASDAQ 100 ($NDX). Of particular note is that the NASDAQ Composite ($COMPQ) - like the DJIA - also failed to make a higher high this past rally, diverging with its sister index, the $NDX. Such divergences amongst major stock indices are not the material longlasting Bull markets are made of.

The decline from Wednesday's intraday high is impulsive and we count submicro waves {1} down, {2} up, and {3} down complete or nearly so (not shown). We expect another up-down {4}, {5} sequence to complete micro degree wave a down (of an a-down, b-up, c-down) of minuette degree ii down, probably in the middle of next week. The larger decline-pattern unfolding should take prices down to a common Fibonacci retrace before equities attempt to turn up and continue their trek higher. Targets would be a .382 retrace of the rally from 10/25 through 11/17 - 10,258, or even as low as 10,155, 10,050, or 9,900. This all assumes the rally up from October 25th was a minuette degree wave i of a larger i-up, ii-down, iii-up, iv-down, v-up of minor degree 5 of intermediate C sequence that should wrap up primary degree wave (2) in early 2005.

Should this decline get serious legs, and take prices below October 25th's 9,708 bottom of the trend-channel, then primary degree (2) topped on November 17th intraday, and a swift, powerful, ominous decline with several crashes along the way - primary degree wave (3) - has begun, with the current decline likely minor degree 1 of intermediate degree 1. In either case, unless prices rise above January 14th, 2000's high of 11,749, the primary Bear market from 2000 lives.

We have been monitoring two key contrary sentiment gauges for sell signals. It would seem that both the 10 Day Average Call/Put ratio and the SPX/VIX ratio are now warning that a decline - possibly quite sharp - is imminent.

Friday, November 19th's 10 Day Average Call/Put ratio registered an overbought 1.47 reading. Historically, ratios over 1.40 indicate a significant top is at hand - sentiment is too Bullish - and ratios under 1.00 indicate a bottom. Yesterday's reading was even higher, at 1.49. These are extremely high readings. The last time we got this high was the top at the beginning of 2004. The last three times prior to then that we received a ratio this high, the DJIA crashed, plummeting over 15 percent within a few months, each time. So this reading is a serious problem for the Bulls.

The SPX/VIX ratio also registered an extreme overbought reading this week - 91.18 on Thursday, November 18th - our Fibonacci phi turn date. This was the highest - and most Bearish - reading in six years. It was about the same as was registered just after the grand cycle top in 2000, which was followed by a two and one-half year 50 percent decline in the S&P 500. Friday's reading came in at a crash-warning 86.69. A sustained Bull market is unlikely until this ratio falls to below 35.00. Readings over 68.00 have warned of imminent crashes. The time taken to develop this top - about a year - is reminiscent of the time taken above 68.00 to warn of the grand cycle top back in1999/2000.

What to make of these two ratios? One thought is they are warning that primary degree wave (3) - the most furious and awful Elliott wave for a Bear market - is about to begin, be that now or in a few months. The correlations are terrific for these contrary sentiment indicators.

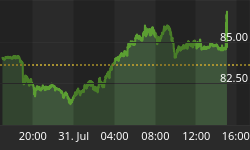

The above chart (courtesy of www.stockcharts.com) shows the S&P 500 has hit new highs for the rally that began in October 2002. We believe the rally since then is a corrective A-B-C rally inside primary degree wave (2) up. The decline from March 2004 through August 2004 was minor degree wave 4 of intermediate degree wave C up. The thrust since August is minor degree wave 5 which is close to completion. The decline from November 17th is likely a minuette degree wave iv down with one more push up to about 1,220 possible to complete minuette degree v of minor degree 5 of intermediate degree C of primary degree (2). There is the possibility that this final wave 5 will truncate. A Bearish Broadening Top "Megaphone" pattern is pressing for the end of primary degree (2) now. Supporting that view is an MACD that is rolling over and an RSI that is turning down from overbought levels last seen in January 2004, just prior to the minor degree wave 4 decline.

The S&P 500 remains a considerable 24 percent below its March 24, 2000 all time high of 1,553. It's PE never came close to falling below 10x - the historic norm for primary Bear market bottoms. Therefore, we believe a new primary Bull market has not started in this index.

The Conference Board's Index of Leading Economic Indicators has now declined for five straight months by a cumulative total equal to the decline back in 2000 when this Bear market began. This is an extraordinary decline for this index. The last time we saw this, the S&P 500 plummeted 50 percent over the next two years. At no time over the past 8 years has the S&P 500 been able to muster a significant intermediate-term rally when Leading Economic Indicators had fallen by more than 0.8 over more than 4 months. Never. This LEI decline poses a major obstacle for the Bullish case.

The Dow Transportation Average appears to have completed primary degree Elliott Wave (2). This terminal occurs with declining volume as several patterns signal a top is in. Trannies' rally finished with two Rising Bearish Wedge patterns (Ending Diagonal Triangles) - one for minor degree 5, and one for minuette degree v inside minor degree 5. These patterns are common terminations for primary degree waves. What's happening here is that demand is being met with stronger and stronger supply as prices creep higher. The reversal will be confirmed once prices break below the bottom boundary line of the Wedge. There may be some back and forth as prices attempt to bust back above the Wedge, but these patterns - once broken down - become formidable resistance.

Also marking the end of the ride is a Parabolic Spike noted with the red rising arc. These patterns are outgrowths of Rounded Bullish bottoms that have reached mania. Prices get to the point where they go straight up - vertical. While it is sometimes difficult to know how high "up" is, we have help this time as the MACD has crossed over and momentum is down. The RSI has also turned lower from overbought territory, and of course the terminal Ending Diagonal Triangles clue us that the Parabolic Spike has topped and a trend reversal has begun.

Here's the bad news for this index: Parabolic Spikes do not have soft landings. The next move after this pattern is hard down, often a crash. This is because PEs have gotten out of hand (over 90x), and earnings cannot live up to the hoopla. These are buying panics - a greater fool's game. Declining volume supports this expectation.

The Economy:

The Conference Board reported that U.S. Leading Economic Indicators fell 0.3 percent in October to 115.1, the fifth consecutive monthly decline. Does that sound Bullish? This is not a government produced number.

Now that the election is over and next year's fixed social security increase has been set, the Labor Department announced that - gee wiz - energy costs are up, so the PPI that was up "only" 0.1 percent in September was up 1.7 percent in October. That is the single largest admitted jump in wholesale prices in a decade and a half. Hmmm. Oil was 48 bucks a barrel in September, and $43 in August, but the increase didn't really show up until October. Yeoman's job. Consumer Prices were reported by the Labor Department to be up 0.6 percent in October - a 7.2 percent annualized rate. How's this for a consumer tax?

The Mortgage Bankers Association informed us that Refinancings are up and New Mortgage Demand is down - down a hefty 0.6 percent for the week ended November 12th.

Greenspan warned that a weak dollar and high trade and budget deficits could produce economic problems for the U.S., according to a story at www.cnnmoney.com This came on the heels of the U.S. Dollar hitting a record low versus the Euro this week. The Fed Chair's remarks also came as the U.S. Debt Ceiling was raised by $800 billion to $8.2 trillion.

Jobless Claims came in at 334,000 for the week ended November 13th, an increase over the initially reported figure for the prior week, which was of course revised higher by Labor Department.

The Secretary of State pre-softened Americans to the idea that Iran could be the next Iraq. Get ready. Let's review. Pre-war, the market declines. Once the bombs fly, equities rally.

Money Supply, the Dollar, & Gold:

M-3 sits almost exactly where it was on August 23rd, 2004. That's no growth over three months. Our research indicates that whenever M-3 plateaus or declines over two or more months, equities subsequently decline.

The trade-weighted U.S. Dollar remains on its track for a primary degree Elliott Wave (1) bottom. It is in the latter stages of this quest, finishing off an intermediate degree wave 5 down of (1) down. Inside that wave, the Dollar has completed minuette degrees i through iv, and is wrapping up v of minor degree 3. There should be a bit more decline followed by a small minor degree wave 4 rise and then one final descent to a bottom - minor degree 5 of intermediate degree 5 of Primary degree (1).

The entire decline to the primary degree (1) should hit at least 82 - perhaps lower - and we are close to that target now. We know this from the Head & Shoulders Top pattern formed by intermediate degree Elliott Waves 4 and the first half of 5. This pattern is confirmed by the decisive break below the neckline - below 87 - which increases the probability of the minimum downside target of 82 being reached. Prices remain inside the long-term downtrend.

After a bottom is reached, look for a pretty strong A-B-C rally inside primary degree wave (2) that retraces a Fibonacci percent of primary (1) down's carnage - either .382, .500, .618, or .786. It is a rally that could consume a huge chunk of 2005. Then an awful primary degree wave (3) down.

Here's the problem with a falling dollar. As the value of our currency declines - due to too high budget and trade deficits, and too much printing press action - the appeal of holding U.S. dollar denominated assets by foreigners diminishes. The longer foreigners hold assets of a deteriorating currency, the lower the value of those assets. So, foreigners become disinterested in buying new U.S. assets and develop a growing disdain for depreciating U.S. stocks and bonds. The risk here is that foreigners start dumping our financial assets. The problem from their perspective is, once they dump our stocks and bonds, what do they do with the money? And that is a real issue which is why so far they haven't dumped. But if they can find an acceptable alternative investment, selling pressure could annihilate our stock and bond markets. This, in effect, is what Greenspan was saying this week - only in Maestro-talk. Just speculating, but world instability could strengthen the U.S. Dollar - for example a Middle East event - perhaps the catalyst to primary degree wave (2) up. In that case Gold may not act inversely. Just a thought.

Gold continues to hit new rally highs with renewed upward momentum this week. Prices remain solidly inside their long-term upward trend-channel. Near term, the RSI is overbought and there is a Bearish Rising Wedge pattern with a common "throw-over," indicative that Gold's advance may need to correct a bit soon. However, the dominant pattern is a Bullish Ascending Triangle which portends continued upward advance for Gold intermediate-term. This pattern is suggesting Gold should approach a target of 500. That is arrived at by taking the distance of the widest part of the triangle and adding it to the spot of the breakout. Last week we noted Gold had hit its highest level since 1988. This week add another 10 points to that statement. Helping demand for Gold - through liquidity and convenience - is the commencement on Thursday of the first and long awaited exchangetraded fund for Gold, traded on the NYSE.

The chart on the next page shows that the HUI is in a long-term Bullish trend. The question is, where does it stand in the intermediate trend? The Elliott Wave count is ambiguous and can be interpreted three different ways. The top count we have labeled requires prices to decline soon from here - a minor degree B top. A move above 258 would mean one of the two other counts are in play. If the above count is correct, wave C down of corrective wave 2 down would likely take prices to a Fibonacci retrace of intermediate degree wave 1 up - for example, .786 would target 138ish.

Should prices move decisively higher, a second possibility is that where we have labeled minor degree wave A would in reality be minor degree wave 4 of the rally from October 2002. That would mean we are rallying inside minor degree wave 5 up, completing intermediate 1 up. That would likely complete over the next two months, to be followed by a huge decline - corrective intermediate degree wave 2 down, lasting half of 2005. A third possibility is that should prices rise decisively from here, corrective intermediate degree wave 2 completed where we labeled wave A down, and we are off to the races for a wondrous intermediate degree wave 3 up to the stratosphere. Given the overbought conditions, this is the least likely scenario in our view. The RSI has formed a Bearish Head & Shoulders top pattern, as has the MACD.

Silver (chart not shown) continues its Parabolic Spike pattern and has now retraced .786 of the move down from April's high. The rally since May's low looks like an A-B-C Elliott Wave - a correction - so Silver may be ready to decline. The MACD is slightly down since October, diverging with the rally - which is Bearish.

However, we see a classic Rounded Bottom formation which is a Bullish pattern of accumulation. Inside this large Bullish pattern can be a series of smaller Parabolic Spikes where prices get ahead of themselves - all the while pushing Silver higher and higher. . The RSI is not overbought - is neutral. Should prices continue to rise and take out the April 2004 highs, Silver would be poised to move higher.

30 Year U.S. Treasury prices are forming a small Bearish Head & Shoulders pattern for the Right Shoulder of a massive long-term Bearish Head & Shoulders Top pattern that started in 2002. Bonds should break lower from the neckline of the smaller H&S pattern, perhaps as low as the neckline of the larger H&S pattern. Both H&S patterns will confirm once prices drop decisively below their necklines, below 110.5 for the smaller one and below 101.5 for the larger. Once the larger H&S neckline is breached, the minimum downside target will be the low 80s.

Looking at the Elliott Wave count that we believe to be most accurate at this time, minor degree wave c of intermediate degree wave 2 up looks to have completed at a Fibonacci .786 retrace of intermediate degree wave 1 - a common retrace point for wave 2s. Both the RSI and the MACD have formed Rounded Bearish Top formations and are headed lower.

Bonds are one of the key problems for the Equity Secular or Intermediate-term Bull Market argument at this time. Bonds are at risk of decline just as equities try to fly, and ensuing rising interest rates will snuff out the fundamental earnings and spending necessary to fuel higher PEs. Bonds are a governor over equity irrational exuberance. The twin deficits will keep pressure on the Dollar and that will also tend to push Bonds lower, keeping a lid on equities.

Should equities fall sharply, we would expect an initial flight to quality, pushing Bond prices higher. But in that event, the Master Planners would no doubt flood markets with liquidity, and Bonds would fall.

Bottom Line: The intermediate-term equity picture will clear up once we know the extent of the current decline. A drop below 9,708 in the DJIA will signal a sharp drop in stocks for an extended period of time. Failure to take out that low will signal that equities are in an intermediate-term, secondary Bull market run - a final Elliott Wave 5 of C of primary degree(2) up of the Bear Market that began in 2000. The extent of this topping rally is unknown as 5th wave terminations can truncate. Assuming it doesn't truncate, the top would likely occur about two months from now. Deficits, unfunded liabilities, failure of PEs to correct to historic lows, extraordinary high Bullish sentiment patterns in the SPX/VIX ratio and the 10 Day Average Call/Put Ratio, major equity averages divergences, Bearish topping patterns in Bonds (portending rising interest rates), the threat of war with Iran, flat M-3 growth, declining Leading Economic Indicators all warn that any rally from here is unsustainable and serves the purpose of luring in more innocent for the next bloodbath from the Bear. You can chase a possible - but by no means certain - 10 percent rally by going long here, however risks are high that you get trapped in a shocking downdraft. Wealth preservation objectives argue for conservatism here. Caution remains warranted.

"He gives strength to the weary,

And to him who lacks might He increases power,

Though youths grow weary and tired,

And vigorous young men stumble badly,

Yet those who wait for the Lord

Will gain new strength

They will mount up with wings like eagles,

They will run and not get tired,

They will walk and not become weary."

Isaiah 40:29 - 31

Coming Soon: In early 2005, we will be introducing a new feature for those who are interested in trading. Trader's Corner will document options trades only available on our website at www.technicalindicatorindex.com. Subscribers can contemporaneously follow our purchases and sales based upon what we believe to be high probability trading opportunities in the markets.

Special Note: Be sure to register under the subscribers' section at www.technicalindicatorindex.com for e-mail notifications and password access of our mid-week market analysis, usually available on Wednesdays or Thursdays. These midweek updates are only available via password access when posted on the web.

| Key Economic Statistics | ||||||||

| Date | VIX | Mar. U.S. $ | Euro | CRB | Gold | Silver | Crude Oil | 1 Week Avg. M-3 |

| 5/28/04 | 15.52 | 88.98 | 122.10 | 276.25 | 394.0 | 6.11 | 39.88 | 9251.6 b |

| 6/04/04 | 16.57 | 88.50 | 122.93 | 274.75 | 391.7 | 5.81 | 38.49 | 9255.6 b |

| 6/11/04 | 15.10 | 89.23 | 121.01 | 269.25 | 386.6 | 5.78 | 38.45 | 9265.9 b |

| 6/18/04 | 14.95 | 89.41 | 121.17 | 267.75 | 395.7 | 5.98 | 39.00 | 9305.7 b |

| 6/25/04 | 15.19 | 89.22 | 121.41 | 270.75 | 403.2 | 6.12 | 37.55 | 9296.2 b |

| 7/02/04 | 15.15 | 88.18 | 123.09 | 265.50 | 398.7 | 6.01 | 38.39 | 9327.7 b |

| 7/09/04 | 15.78 | 87.41 | 124.10 | 269.00 | 407.0 | 6.46 | 39.96 | 9273.9 b |

| 7/16/04 | 14.43 | 87.12 | 124.36 | 271.50 | 406.8 | 6.72 | 41.25 | 9238.8 b |

| 7/23/04 | 16.50 | 89.23 | 120.88 | 269.50 | 390.5 | 6.33 | 41.71 | 9259.9 b |

| 7/30/04 | 15.27 | 90.12 | 120.10 | 267.00 | 391.7 | 6.56 | 43.80 | 9272.3 b |

| 8/06/04 | 19.34 | 88.45 | 122.69 | 268.25 | 399.8 | 6.77 | 43.95 | 9267.9 b |

| 8/13/04 | 17.98 | 87.97 | 123.68 | 269.19 | 401.2 | 6.62 | 46.58 | 9250.2 b |

| 8/20/04 | 16.00 | 88.22 | 123.03 | 279.50 | 415.5 | 6.87 | 46.72 | 9261.8 b |

| 8/27/04 | 14.74 | 89.80 | 120.20 | 275.00 | 405.4 | 6.58 | 43.18 | 9298.5 b |

| 9/03/04 | 14.28 | 89.56 | 120.66 | 275.25 | 402.5 | 6.59 | 43.99 | 9288.6 b |

| 9/10/04 | 13.75 | 88.60 | 122.61 | 272.50 | 403.8 | 6.16 | 42.81 | 9280.9 b |

| 9/17/04 | 14.03 | 88.10 | 121.76 | 275.75 | 407.6 | 6.28 | 45.59 | 9275.2 b |

| 9/24/04 | 14.28 | 88.59 | 122.57 | 278.50 | 409.7 | 6.42 | 48.08 | 9319.7 b |

| 10/01/04 | 12.75 | 87.77 | 124.07 | 284.75 | 421.2 | 6.94 | 50.12 | 9335.4 b |

| 10/08/04 | 15.08 | 87.55 | 124.13 | 287.60 | 424.5 | 7.29 | 53.31 | 9294.9 b |

| 10/15/04 | 15.04 | 87.20 | 124.73 | 286.45 | 420.1 | 7.11 | 54.93 | 9259.8 b |

| 10/22/04 | 15.28 | 85.97 | 126.46 | 287.00 | 425.6 | 7.33 | 55.17 | 9280.5 b |

| 10/29/04 | 16.27 | 84.98 | 128.85 | 284.75 | 429.4 | 7.30 | 51.76 | 9297.8 b |

| 11/05/04 | 13.84 | 83.89 | 129.46 | 283.00 | 434.3 | 7.50 | 49.61 | 9303.0 b |

| 11/12/04 | 13.33 | 83.71 | 129.85 | 283.50 | 438.8 | 7.62 | 47.32 | 9300.4 b |

| 11/19/04 | 13.50 | 83.32 | 130.13 | 287.25 | 447.0 | 7.60 | 48.44 | - |

Note: VIX complacent; Dollar down; Gold and Oil up.