Before we review current bull/bear signals from silver, Bloomberg had an on the money comment relative to the efforts in Europe:

"Recapitalizing the banks is not the solution," said Justin Bisseker, who helps manage 205 billion pounds as a European bank analyst in London for Schroders, Britain's largest independent money manager. "Sovereign risk is the principal concern. Once investors' confidence in sovereigns returns, then confidence in the banks will follow."

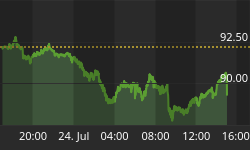

You do not need to know anything about technical analysis to conclude the two charts below of the silver ETF (SLV) look similar in many ways. The first chart is from August 2008 and the second from the present day (compare points A through H).

How can these charts help us with stocks, commodities, and precious metals? Silver tends to be in greater demand when (a) the economy is expected to grow, and (b) when inflation expectations are high. According to the Silver Institute:

Silver has a number of unique properties including its strength, malleability and ductility, its electrical and thermal conductivity, its sensitivity to and high reflectance of light and the ability to endure extreme temperature ranges. Silver's unique properties restrict its substitution in most applications.

When silver is weak it is logical to question (a) the expectations for future economic growth, and (b) if investors are concerned about future inflation. If inflation is not a concern, then deflation fears are most likely increasing.

If we assume silver continues to trace out a similar path to what transpired in 2008, which may or may not happen, what are the possible implications for stocks, bonds, currencies, commodities, and precious metals? The first silver chart above shows the period September 29, 2007 through August 29, 2008. The charts below show asset class performance from August 29, 2008 through November 21, 2008, allowing us to answer the question, "What happened next in the 2008 deflationary period?" The key for the charts below: (SPY) S&P 500, (EEM) emerging markets, (FXA) Australian dollar, (UUP) U.S. Dollar Index, (DIA) Dow, (DVY) dividend stocks, (TLT) Treasuries, (SH) short S&P 500, (GDX) gold stocks, (GLD) gold, (SLV) silver, (DBC) commodities, (DBA) agriculture, (EWG) Germany, (PFF) preferred stocks, (XLU) utilities, (XLP) consumer staples, (XLY) consumer descretionary, and (JJC) copper. Symbols and descriptions are shown in the upper-left corner of each chart below.

What happened next in 2008?

If the silver ETF can fill the gap in the chart below (between 32.54 and 34.51), it increases the odds of bullish outcomes for stocks and commodities. The longer SLV can hold above 32.54 the better for the bulls. If SLV fails to clear 32.54, the odds increase of an August 2008 scenario occurring again, similar to the outcomes shown in the charts above. An intraday move in SLV below 27.41, and more importantly, a weekly close below 27.41, increases the odds the deflationary trio of shorts (SH), the dollar (UUP), and bonds (TLT) will perform well.

Other bull/bear considerations beyond silver:

- On October 7, we outlined the case for a strong bear market rally similar to March 2008 - May 2008. The bullish set-ups in this video still need to be respected.

- On October 11, we showed how weekly moving averages have served as a bull/bear market demarcation line since the late 1990s. This video outlines the case for sellers to become active between 1,209 and 1,260 on the S&P 500. The strongest resistance lies between 1,209 and 1,249. While not highly probable, a case can also be made for a rally back to 1,260ish (neckline of head-and-shoulders pattern).

The markets may be underestimating the challenges and dollar amounts that lie ahead in Europe relative to bank recapitalizations. We mentioned on October 5 a quick fix in Europe is a tall order. Below are comments from the Wall Street Journal relative to the first bailout (Dexia):

Dexia's French operations needed more liquidity than they could access, and over the weekend the governments of France, Belgium and Luxembourg agreed to break up the bank and either nationalize or attempt to sell off the assets. That's going to be expensive: Belgium's promised portion of the funding guarantee alone will leave its taxpayers on the hook for the equivalent of 15% of gross domestic product, on top of their existing government debt of 96.6% of GDP.

As of this writing, we continue to give the bearish/deflationary case the benefit of the doubt, understanding strong and gut-wrenching countertrend rallies are part of any bear market. Our portfolios continue to contain a mix of cash, shorts (SH), bonds (TLT), and the dollar (UUP). The deflationary/bearish case will take a hit if the S&P 500 trades between 1,250 and 1,260 for more than three or four days. The past two bear markets (tech bust and mortgage crisis) were primarily set in motion by events in the United States. Since the current state of affairs is primarily linked to Europe, the S&P 500 could surprise on the upside for a few months, although that remains a relatively low probability outcome.