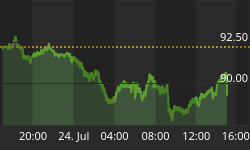

Well, what else am I going to write about today? Markets got to react to the EU deal announced late last night, and went predictably bonkers. Stocks rallied 3.4% to the highest level since August 1st. Note yields also rose to the highest level since early August, up 17bps at the 10-year point to 2.37%. TIPS held up well, as 10-year real yields rose only 7bps (implying that inflation swaps and breakevens were about 10bps wider). The dollar plunged, to its lowest level since early September (see Chart) and falling against every major currency in the process: Euro, Sterling, Yen, Aussie and Canadian Dollars, Brazilian Real..

Rough times for the dollar recently. If there's no safe-haven bid, it seems there isn't much bid!

Commodities, as a result of the sharp dollar move and the general feeling that economic disaster has been averted, rallied sharply. The DJ-UBS was +2.5%, with Copper up 6%, Silver up 5%, Crude and Wheat up 4%, and only Nickel and Nat Gas down by more than 1%.

The catalyst, obviously, was the EU deal. The basic elements of the deal are:

- The banking lobby has agreed, with no binding commitment, that private banks will take a voluntary 50% writedown on their holdings of Greek debt. It appears that this will be done through a complicated as-yet-to-be-devised structure, with the EU kicking in some kind of 'incentives.' It is all very murky.

- The EFSF will be leveraged, probably 4-5 times, by providing first-loss guarantees on primary debt through a SIV that is funded by private investors (crazy ones), sovereign wealth funds (none has yet committed), and maybe the IMF, although the UK is already moving to block the IMF from using cash sourced from England.

- The EU will restore guarantees for bank issuance, and require Tier One capital to be raised up to 9% by June 2012. No mention is made of how banks which have just taken billions of Euros in write-offs will raise so much private capital. Details, details.

The effect of the grand bargain will be to reduce the Greek debt burden all the way down to - drum roll, please - 120% of GDP by 2020, a level typically associated with unsustainable debt dynamics and eventual default. So you can see, it's a big improvement!

Still, given that the EU did manage to produce some pyrotechnics, it is incredible that Greek bonds aren't doing better. The Greek 5y note rallied all of 4 points, to about $44. The yield fell to 25% or so. Considering that this deal is supposed to put the country on the path to sustainability..and presumably, that means the bonds should be paid off at maturity..it seems to me as if they should be doing better. I would understand if there was some overhang from dealers selling around a price of 50, where they're theoretically going to have to take losses anyway, but shouldn't buyers be willing to pay at least that much? It seems to me that bank bond holders should be dumping bonds at 55 or 60 to non-bank holders who plan to hold and be paid par. I suppose if I was the non-bank investor (and I am) I might be skittish at paying very much even given the EU promise. They might have made the promise with their fingers crossed.

Other PIIGS country debts improved as well, but again the rally was surprisingly delicate. Portuguese 5y bonds rallied 93bps to 13.8; Spanish 5yrs rallied 16bps; Italian and Irish bonds only 6bps.

In case my sarcasm isn't plain enough, I'm not very impressed by this deal. I was pretty sure that something would be announced, and I was pretty sure it would have no substance, but I guess I was expecting something a little more. Even if you believe their numbers, it doesn't get Greece to sustainability!

Moreover, I continue to be truly amazed at the complete misunderstanding of leverage by politicians and their advisors. Here's an insight: if you have $400bln of capital and you lever it four times, you don't have $1.6 trillion of buying power. You have $400bln of buying power. It merely gets spread out over a larger face amount of bonds - now, a 25% move will wipe you out with (ta-da!) $400bln in losses. No amount of leverage changes the fundamental equation of how much of a loss you can absorb. It only changes how many bonds you can spread the loss over. It frustrates me to see such a primitive understanding of markets, market structures, and leverage among the very people who are supposed to be saving us all. At least a banker understands that leveraging up isn't a solution to a lack of m arket power.

Well, except apparently for John Corzine, whose MF Global has now been downgraded to junk and about whom, as I write this, Bloomberg is printing headlines saying "MF Global is said to have drawn down credit lines this week." MF Global is no Lehman, but it's a significant firm with some very good people..and cavalier leadership, apparently. Still, MF Global was managed better than Greece was. I wonder if they'll get a SIV to support them.

I don't think the Greece drama is over. I hate to say that, but I really don't. Perhaps this buys a few days before skeptics dissect whatever details there are, or some sovereign legislature votes the deal down, or a consortium of banks splinters off from the main deal, or a supranational backs away. Contributing to that pressure will be the other PIIGS at the trough, who will want deals at least as good as the one Greece got (and reasonably so). On the other hand, the Fed meets next week and some observers expect a gesture towards QE3..especially if the European drama doesn't fade quickly. I don't expect the Committee to do something that contrasts so directly with what some members of the FOMC want, especially while stocks are up and commodities are also.

Yes, they will be aware too of the next big deadline - in late November, if the so-called 'Supercommittee' does not agree on concrete steps to cut the deficit (and there is no sign of any agreement yet), substantial mandatory spending triggers will be enacted. I am sure QE3 remains in the quiver in case it is needed, but I doubt they'll be pulling it out just yet.

One of my criteria for getting back involved in stocks was that the VIX break appreciably below 30. Well, it has done so by trading down to 25 today. Unfortunately, the decline in the index was mainly due to the directional move (the VIX usually declines in rallies and rises in selloffs, because the index methodology weights strikes according to moneyness, and so when prices are falling the higher-volatility puts gain weight compared to the lower-volatility calls), and the market valuation is too rich for my blood. I participated in today's rally through my bond short (TBF rallied 3.4% today, keeping pace with stocks) and my commodity index long, but there's no doubt my performance trails the equity market this month!