Monday was another day of feeble volume in the markets, but at least today there was the excuse that there wasn't any important economic data due out until Alcoa's earnings announcement after the close (as expected, they lost money for the quarter but on better-than-expected sales). NYSE volume matched Friday's paltry sum of around 675mm shares.

As the weak volume trend continues, it is growing more remarkable. It implies a lack of conviction, or indecision. How is this likely to resolve? Is it likely to resolve into conviction, and buying, or alarm/concern, and selling? My suspicion is that in the absence of a positive exogenous event, we are more likely to see weak longs get weak-kneed and equities to head lower.

But my personal conviction level on that topic is low. Volumes in other markets are also weak, so applying the same logic as I have just applied to equities would suggest all markets should head lower. While that is possible, it seems unlikely. It may simply be that we are moving to a 'new normal' (pardon the misappropriation of the expression) of lower volume and thinner market conditions. One market participant opined to me that the Fed's recent announcement that it would substantially adopt the Basel III recommendations for bank regulations - it was expected that they would adopt some, but not all, of the restrictive regulations - has caused many banks to re-think the scale and scope of their U.S.-based operations and, in some cases, to pull back from business and market-making. This is not terribly shocking, except that the degree of this effect would be surprising if the current desiccation of volume continues.

Lower liquidity implies lower prices (there is a reason that they call it a 'liquidity discount'), although probably not substantially in any particular asset class. But lower liquidity represents a loss of societal wealth and efficiency. Does this affect a retail investor? Yes, since it implies lower prices overall, but in terms of a noticeable effect on day-to-day trading, not much. But it will affect the retail investor through the return drag that larger mutual funds (for example) will experience. Large institutions already have complicated algorithms to efficiently enter and exit positions while minimizing market impact; less liquidity implies more market impact (which is a cost, although it shows up as return drag rather than a customer fee). None of this will cause retail investors to march on Washington, which is why it is being enacted even though society bears a cost for it.

Again, I don't want to read too much into a few days of low-volume trading, but these are my thoughts as more of these days get strung together.

Heading into a potential crisis, by the way, is a bad time to be sucking liquidity (in the sense of transactional liquidity, not monetary liquidity) out of the market. Today Germany sold €3.9bln of 6-month TBills at a negative yield (-0.0122%); recall that happened in the U.S. in late 2008, so it's not unprecedented. It is even rational: investors are taking a certain loss instead of some unknown probability of a substantial loss they might realize on bank deposits if a bank goes bust, especially if it goes bust in conjunction with a sovereign bankruptcy. The classic argument is that yields cannot be negative because cash has a zero yield, so the worst case is you hold cash. This works for you and me, but not Siemens or another huge company that doesn't want to take hundreds of millions or billions of Euro notes. If such a company sees a 0.5% chance of losing 20% of the money they have on deposit, then they would happily own a German bill that yields as little as -0.10%. Or, if a company sees a 10% chance of losing 1% simply because their cash deposits are tied up in a bankruptcy and not accessible (or earning a return) for a while, the same reasoning applies. So it is not unthinkable that yields can be negative. It is, however, a harsh indictment on the state of the banking sector.

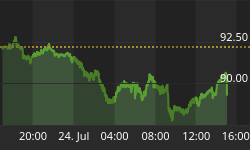

Speaking of Germany, a Barclays analyst appeared on CNBC today actually talking about the fact that inflation expectations are rising in Germany. He pointed to 5- and 10-year inflation breakevens and noted the chance of a 'break higher' in expectations. I don't necessarily read this this chart (see below, source Bloomberg) quite as bullishly as he did, but it's surprising to hear anyone talking about inflation in Europe these days, and no doubt inflation is not expensive, pretty much anywhere.

German 10-year breakevens. Certainly not expensive given the ECB's stance.

That's not to say that I don't think investors should be thinking and bracing for possible inflation. If there is a trade out there that looks relatively easy to me, it is being long breakevens. As I wrote last week,

It is incredible to me that with monetary conditions as accommodative, globally, as they have been in decades, inflation swaps are still nearly as cheap as they have ever been. That's truly striking. What is the 10-year downside to a long inflation position from these levels? One-half percent per annum? Seventy-five basis points per annum? How low can inflation be over the next 10 years, especially with central banks apparently willing (and even anxious) to produce as much liquidity as is needed?

Commodities are still holding in, and that is one way to be long inflation. Commodity indices tend to have a high beta when inflation first begins to rise. However, one can also be long inflation expectations themselves. Institutional investors can do this through inflation swaps or breakevens, but retail investors can do this as well. On Wednesday, I will discuss a new exchange-traded security that allows investors to bet directly on inflation breakevens.

If you have not already done so, would you please help me gather some market information by taking a single-question anonymous poll, about your interest and/or willingness to buy certain kinds of hypothetical inflation-linked bonds linked to different things? The poll will take no more than two or three minutes, and I would really appreciate it. I'd also appreciate it if you would forward the poll link to your social networks and ask them to participate as well, since a bigger sample is usually better! The poll is here. Thank you very much!