Do you want the full "Gold - The Weekly Global Perspective"? If so,

| In the FULL version of this publication, we include price support/resistance levels alongside expected price action - short-term. Subscribe - www.authenticmoney.com " Global Watch - The Gold Forecaster" [The full version plus GOLD SHARES,OIL, TREASURIES, DOW and much more: www.goldforecaster.com |

That was the week that was

The Funds ruled the roost during the holidays until last Wednesday. Then came the explosive news that took Technical features out of the picture and reminded us all that gold is moving as a currency, and driven by structural decay in the global economy. The Trade deficit came in at $60.3billion in November. The Euro leapt up away from the $1.30 area in minutes, taking gold with it up to $427. But how important it was that the funds did what they did, by taking the quiet holiday period to play with the Technical structure, press the price down $36, clearing out major speculative positions in the process, removing that awful feeling that one was buying at the top, and bringing the price to levels all present buyers feel comfortable with. The made the professional gold market players happy, as well as helped all to realise that the fundamentals weigh heaviest when they kick in hard, like the Trade deficit. Our forecast of 2005 being a year of 'volatility' is already being proved correct, but brace yourself for much more this year.

The Euro price of gold moved down to Euros 319, but held around 320, before steadying and building a foundation at the Euros 322+ level. This all happened because the opportunities the Technical picture offered, resulted in the huge fund liquidation taking net long positions to 249 tonnes from the peak last year of 610 tonnes and from a level of 516 tonnes in November. This leaves little room for them to push the price lower, so we expect consolidation for a while.

We have also established as fact our forecast and many statements that we have made over the last year that a strong U.S. economy sucks in imports and exacerbates the Trade deficit.

The weaker bias, we forecast last issue, appears, at first sight, to have been dismissed, being replaced by a period of consolidation. It is now for the market to decide whether the U.S. Administrations words, claiming yet again that they favour a strong $, in the face of action that says the opposite, hold any more water than they did the last time! This will decide the near term direction of the Euro/$/Gold.

The Indian market saw strong buyers of gold through London, in the last quarter of 2004.

The wave we now see in the gold market should take it further up the beach than the last one did, as the tide pushes harder.

Latest

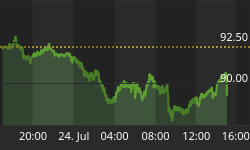

At the time of writing, gold stood at $422.70 and in Euros 322.770. The Euro is worth $1.3096.

The Dollar - Is the rally over? Or is the future better for the Greenback? - The U.S. $ Index

Fundamental Features:

In 2005 the $/ started the year holding tight to the gold price. The jump in the Euro on the publication of the startling deficit number of $60.3 billion in November, sent the $ down rapidly. It had rallied to just below the $1.30 level, but then leaped to $1.32 almost immediately on the press release. This has brought a new feature to the surface one that is critical for us to assimilate. We can discard the thought that there is a link between the Dow and the gold price. Both fell and both rose together during the last week. On the interest rate front the picture starts to break away from the apparently sound concept of a 'return' on your money. The interest rates available on the $ have been higher than on the Euro, so if return on investments were what counted [and several Central Bankers have trumpeted this as justification for turning from gold] there should have been a major capital flow from the Euro to the $. But there has not been. What has grown in importance is the concept of the capital value of a currency. The longer term prospects of the value of the $, irrespective of the return one can get, is now more important to investment managers. This is a departure that we have been waiting for. It reflects dropping confidence, a main driver of gold. Gold gives no interest rate return of its own, but does have great capital gain prospects. With the market showing a move away from the return concept, gold will hold its own by comparison to currencies in this changed 'climate'.

France is not selling Germany's 'option' to sell 120 tonnes in 2005!

Until an announcement to the effect that France has taken over the option to sell Germany's 120 tonnes in the year Sept 2004 to Sept 2005, we do not accept that it has. One of the foundations of the Central Bank Gold Agreement was to provide "Transparency" to European Central Bank sales in the future. Such actions would go directly against that objective.

Ceilings not sales!

We must remind ourselves that the 2004 Central Bank Gold Agreement only set "ceilings" on sales of gold by the signatory Central Banks; it did not state that these amounts would be sold. To date the evidence of Central Bank sales confirms that far less than the ceiling limits have been sold.

G.F.M.S. and our Track record!

The latest survey from the reputable consulting firm G.F.M.S. has just been released reviewing 2004. Their fact-gathering abilities, forms the foundation of an accurate global gold picture. We attempt to forecast the next period ahead and rely on such firms to lay the foundation for our future forecasts and to establish our forecasting track record. We are happy to say that the record we have established has been sound. We dislike the concept of bragging, but realise that you the readers and Subscribers need to know whether you are getting your money's worth. In a nutshell, what we forecast has been accurate on the supply side, and the demand side, but more importantly, our reading of the monetary scene and its impact on the gold price and attitude of the leading market players to gold has been absolutely correct.

These were the highlights of the G.F.M.S. report: -

- Official Sales: - Constrained selling by the signatories to the Central Bank Gold Agreement (CBGA) was the prime cause of the decline in "Official" sales for the year as a whole, though quite numerous purchases by others, most obviously Argentina, were significant. We at G - AM have specialized in this aspect of the gold market and will continue to do so over 2005 and onwards.

- De-Hedging: - The report singles out the major importance of producer de-hedging, which is estimated to have risen by over 50%. G - AM have forecast that de-hedging will continue to occur until the level of hedging is consistent with levels which provide financing for the mines, no more.

- Mine production: - Was also, and slightly unusually, said to have been a contributor to price strength in that it fell unexpectedly by a sizeable amount of 110 tonnes or 4%.

- Exchange Traded Funds: - The report this year devotes a greater amount of space to investment, partly to accommodate an analysis of a relatively new area, exchange traded funds or E.T.F. 's. G.F.M.S. noted, "the E.T.F. 's, especially New York's streetTRACKS, are looking quite exciting at the moment. Their combined holdings after all aren't that far off the 200 tonne mark".

- Acceptance of higher prices: - The consultancy lastly feels sentiment was critical. This is normally seen in the context of where western investors and the major mining companies think the price is going but on this occasion the report ranks of similar importance the growing acceptance by the traditionally price sensitive countries of prices above $400 as fair and sustainable. G - AM will continue to focus on the relationship between the global macro-economic and Monetary scenes, the global gold markets in different currencies and the gold price.

International Gold Prices in their Currencies:

London. Euro €: $1.3096

London dominates the physical market in gold. The Comex market exercises a primarily short-term surface action for gold. We expect in 2005 the London Fix will exercise even greater dominance over the daily prices than it did in 2004. Whilst the $ is still the prime currency in which the gold price is made, its relationship with the Euro is the one that has defined it most as a currency, over the last year. The gold market keeps a very close eye on the Euro price, which defines the real price of gold presently.

London dominates the physical market in gold. The Comex market exercises a primarily short-term surface action for gold. We expect in 2005 the London Fix will exercise even greater dominance over the daily prices than it did in 2004. Whilst the $ is still the prime currency in which the gold price is made, its relationship with the Euro is the one that has defined it most as a currency, over the last year. The gold market keeps a very close eye on the Euro price, which defines the real price of gold presently.

Euro Fundamentals:

The Euro appears little changed since our last report, with it still standing above 320 at Euros 322 for an ounce of gold. It has held steady at these lower levels since the recent correction from Euros 336.

As we pointed out last issue gold is below its long-term level of Euros 330. Euro interest rates are on a par with Euro-zone inflation at 2%, which is why the Euro interest rates was held at 2% this week. U.S. $ rates are higher, which is why there is the struggle going on, on the exchange rate front. Question is, is the total return on the $ worth more than the total return on the Euro. The answer to this question will point the Euro's direction. Are interest rate increases enough to give true value?

India:

Rupees: ($1: Rupees 43.60)

Present Price [excluding duties, etc] Rs.18,429.72 per ounce [last week: Rs.18,685]

Key Fundamentals for the Indian Market.

The harvest was not bad at all. It was sufficient to remove the past economies of Mothers sacrificing their gold for their daughter's dowry and their financial security. We expect the acceptance of $400 and above as an acceptable price to pay, to continue. With approximately 600 tonnes purchased last year, we expect this year to see a similar performance.

South Africa:

South African Rand ($1: R6.0465)

Key Fundamentals for the South African Market

Some relief on the Rand exchange rate front, but expected to be short lived as the Rand weakened through the R6.00 level to the $ in a reaction to the strength in the $. But then the deficit saw the Rand leap to R5.94 to the $ before weakening to R5.99: $1. Now it is weaker and above the R6.03 level again, while the $ consolidates.

There is an expectation that interest rates in South Africa, will be cut again. However, the country is enjoying a structural boom presently, and there is a fear that if rates are cut it will inspire over-spending and excessive stimulation. This is a weak argument against the continuing stress to exporters, including the gold mines. The sustained pressure on exporters eventually leads to them disappearing off the South African scene. In the latest issue of "Global Watch - The Gold Forecaster", we take a close look at the South African gold and Gold share prospects [Subscribe below].

[The South African Rand is the price paid to the Gold Mines. With South Africa producing 11% of the world's new gold, and some leading Mines operating there, the balance of future gold supplies is directly affected by the strength or weakness of the Rand, so the Gold Price in Rands is a key one to the gold market.] Last week the gold price, per ounce was R2,583.75, today it is R2,555.86.

Silver $6.585 [Euros 5.028]

The future for Silver in 2005 is favouring a similar market to the one it saw in 2004. Industrial demand is strong enough to absorb any selling from the photographic industry. Chinese sales were down 22 % last year. The same sort of reduction should occur this year. The funds will continue to sit like vultures over this market playing it both ways to give a far greater volatility than gold in 2005.

The London Gold Fix

13th January a.m. $421.70 € 321.442

13th January p.m. $422.50 € 322.224

Current London Fix: Latest London Fix

For Online Subscriptions go to: www.authenticmoney.com

For more details contact us at: gold-authenticmoney@iafrica.com