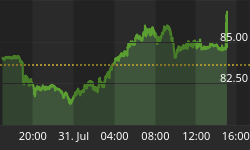

Last we visited a topic of discussion was broiler prices, or the prices for table chicken. At that time broiler prices had thus far in 2012 experienced the largest price increase of the major Agri-Commodities we follow. As the chart below portrays, from the lows of last Fall broiler prices are up more than 50%. Some chickens in the back yard would have provided a nice return.

Reasons for the rally in broiler prices are the standard ones for price cycles in Agri-Commodities. In the case of chickens, years of generally low grain prices and strong growth in the demand for chicken allowed producers to eke out a small per bird profit that was magnified by high volumes. In the recent years, that model failed.

Grain prices, as we know, have not been low for sometime. Producers of broilers, however, failed to revise their operating models and stuck to the old strategy of pursuing high volumes. High grain prices made producing chickens under the historic model unprofitable. The financial agony of the industry was intense. PPC paid the price with bankruptcy. Firm was reborn with financing from JBS of Brazil, the world's largest animal protein producer in 2009. More recently, Cagle's of Georgia filed bankruptcy.

Gradually, after all that financial agony, chicken producers began to rationalize production and demand better prices from their customers. Lower grain prices, and better management policies, have led to the industry's return to profitability in the fourth quarter of last year. Another classic Agri-Commodity cycle had run its course in broilers.

In Agri-Commodities, prosperity leads to excessive production, and ultimately lower prices. Those lower prices then punish producers until production cuts are initiated, and prices recover. Prosperity leads to low prices, and low prices lead back to prosperity. A similar cycle is likely to develop in corn with profitability of corn likely to be severely tested in 2013 with prices as low as $5.

Investors, when faced with an opportunity such as now developing in broilers have some difficulty taking advantage of the changed environment. Direct investing in chickens is largely impractical for most. That leads to the use of Agri-Equities of producers or ETFs with exposure either to Agri-Equities or Agri-Commodities. However, ETFs investors need to remember that "looking under the hood" is still important.

ETFs or similar collective investment structures, generally speaking, create an index, or list, of investments in which it intends to invest. The investor thus knows what those investments will be. In considering these investment vehicles, the investor needs to answer two questions.

-

In what does the ETF invest?

-

In what does the ETF NOT invest?

For this discussion we considered three major indices of Agri-Commodities. All three are names well known, and of sufficient size to be meaningful alternatives to investors. Our first goal was to identify the largest investments of the ETFs, or what they do invest in. The second goal was to identify the important Agri-Commodities in which they do not invest. Results of that analysis are presented in the following chart. Plotted in that chart is the average investment of the Agri-Commodity component of these three funds in six important Agri-Commodities.

As is readily apparent from the chart, wheat, corn, and soybeans are major investments of these indices. Roughly half of the investment exposure is to these three Agri-Commodities. That concentration suggests that the returns on these indices will be heavily influenced by the price of just three commodities. An investment in these ETFs is essentially a decision to invest heavily in these three Agri-Commodities.

Investors should consciously decide that this is the desired exposure. That decision is especially important with wheat in a bear market likely to last til 2014 and corn likely to see $5 in 2013. Should that set of price scenarios play out, these ETFs could substantially under perform the global Agri-Commodity market.

On the right of the chart three important Agri-Commodities are also shown. Rice, for example, is perhaps the most important staple food in about half the world. Two of the three funds had no exposure to rice. Is that appropriate and desirable from the view of the investor?

Chickens and palm oil are non existent investments in these indices. Palm oil is the most important vegetable oil in Asia. In the West, soybean, corn, canola, and other vegetable oils dominate. Is ignoring the importance of palm oil to Asian consumers appropriate and desirable, or an indication of Western-centric investing?

Considering these last two comments might suggest a conclusion that these indices are of Western eating habits, and do not reflect the true global Agri-Commodity market. Excluding rice and palm oil from these indices creates a Western bias that does not reflect the Agri-Commodity consumption of the world. In short, these are indices of the Western world's Agri-Commodity market.

Finally, where's the chicken? At the beginning of this discussion we noted the dramatic increase in broiler prices. That return has been excluded by most commodity ETFs. The implications of this exclusion should not be ignored. Recently, give the strong move by broiler prices, these ETFs have likely underperformed the true Agri-Commodity market due to structural design biases. In short, structural issues may prevent the ETFs from earning the return of the market in some periods which means investors should inquire before they buy.

AGRI-FOOD THOUGHTS is from Ned W. Schmidt,CFA,CEBS, publisher of The Agri-Food Value View, a monthly exploration of the Agri-Food grand cycle being created by China, India, and Agri-Energy. To contract Ned or to learn more, use this link: www.agrifoodvalueview.com