The following is part of Pivotal Events that was published for our subscribers March 8, 2012.

Signs of the Times:

Last Year:

"Consumer Confidence in U.S. Increases to Three-Month High"

~ Bloomberg, February 22, 2011

"Investors Jump Back into Equity Markets"

~ Financial Post, February 24, 2011

"Get Ready For a Growth Super Cycle"

~ Wall Street Journal, March 2, 2011

"Farmland Booms Again"

~ Financial Post, March 4, 2011

"Rush to Use Crops as Fuel Raises Food Prices and Hunger Fears"

~ The New York Times, April 12, 2011

This Year:

"[Credit card holders] tried to reduce debt last year, but some are falling back into their old ways."

~ New York Post, February 26

"Investors are set to increase their exposure to commodities."

~ CNBC, February 26

This was from Barclays review of fund managers.

"The Conference Board Consumer Confidence Index increased to the highest level in a year."

~ Bloomberg, February 28

"Fannie Asks Government for Almost $4.6 B After 4Q Loss"

~ Washington (AP), February 29

Perspective

Recent positive headlines seemed familiar, and in looking back to the same time last year we found the examples posted above. What happened in between - oh, just a huge loss of confidence on the European Sovereign Debt Crisis. That panic ended in late September when we concluded a choppy rally out to January was possible. In mid-January the time for the top was pushed out to February.

Back in early October, we were confident in the indicators that were for calling the rally. We had no way of knowing that another speculative surge would erupt. But for many years now every move ends in drama - up or down.

The drama is a form of financial hysteria featuring "This time the stimulus works!", eventually followed by "Get me out!".

Last year, our Momentum Peak Forecaster called for a speculative surge to become outstanding by around April. This "Forecaster" does not register very often, but if the hot action includes commodities it usually indicates the end of a business cycle. We had thought that a US recession might have started around mid-2011. That it started in the U.S. then is not known--the Oracle of NBER has yet to speak. It usually announces a year after it actually started. What could be a global recession seems to have started in Europe last summer.

Commodities

This remains to be determined and recent action in commodities is telling an interesting story. The CRB reached 474 with the 2008 boom, with an outstanding lift from crude oil. In that fateful June as crude's rally registered a weekly Upside Exhaustion we concluded that a cyclical bear was possible and pointed out that if the monthly reading was accomplished it would suggest a secular bear. That reading occurred at the end of June. We are staying with this outlook - particularly with the revolution in oil and gas shales - around the world.

The ChartWorks has been making some good calls on crude and it has further to run.

In the meantime, base metals (GYX) rallied with the revival from 350 in October to 428 in early February. That level recorded enough momentum to end the move. The test at 427 was not robust and the chart seems to be rolling over. The high last April was 503, which we considered as a cyclical peak (with our Forecaster). At 403 today, taking out 395 would set the downtrend.

It is worth emphasizing that copper's real price, as deflated by the PPI, has been uniquely high for a long time. Copper theft is becoming so prevalent that there is a website www.coppertheft.info (The Growing Epidemic) that reviews the problem. On the supply-side, the exceptional real price is prompting massive mine expansion. As with the highs in 2007, the turn down in real and nominal prices will be forced by the next liquidity crisis.

As we have been noting, the action in agricultural commodities has been disappointing. GKX accomplished a modest rally from an interim low of 398 in December to 450 a week ago. Grains were a strong participant in the speculative surge that concluded in April last year. Enthusiastic quotes from then are listed above. While there is little excess in the chart, the sector is vulnerable.

On their own, soybeans enjoyed a strong rally - strong enough to register an Upside Exhaustion.

Agricultural stocks (COW in Toronto) rallied from 17.43 in October to 22.72 a couple of weeks ago. This recorded a big swing in the RSI from very oversold to almost as overbought. The index has drifted down to 21, and taking out 20.50 would set the downtrend.

Crude oil has set the biggest swing in the RSI from exceptionally oversold in October to 80 a couple of weeks ago. Seasonally, the next rally could carry well into April. Support at 102 is critical. Quite likely firmer action in crude will sustain speculative interest in the general stock markets. We don't subscribe to the recent notion that high gasoline prices cause recessions. The 3 to 4-year business cycle has been evident from as early as the 1500s. There was no gasoline then and the record is that most commodities rise with the business cycle and go down in the recession.

One commodity, by itself, doth not make or break the business cycle.

Credit Markets

Credit spreads have changed from "risk on" to a loss of momentum and some apprehension. That's in corporate bonds and the Ted-spread. The long end and the short end.

Over in sovereign-debt land, the talk is about Greece bondholders taking a negotiated hit from par down to 53. That's a whack, but in a real bond market the issue should be trading at 20, or less. (Mister Market would laugh at a negotiated hit.) Similar Greece bonds are already trading at 19. Definitely on the way to much lower prices. That 19 is a percent of par, or per hundred, PPH. In a real panic they could trade down to parts per million - PPM for abbreviation.

STOCK MARKETS

We have reviewed that the stock markets are up when they should be, and have reached momentum and sentiment readings associated with important tops.

This week the report on insider selling is right up there with last April's top. Most such tops are more of a process than an event.

Currencies

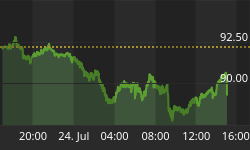

Over the past two weeks, the US dollar index enjoyed a rally from 79.1 to resistance at the 80 level, and is taking a little rest. This is setting up a double bottom and rising through 80 would indicate that the karma of the marketplace is again overwhelming the dogma of policymaking.

Our next target is in the low 90s. Recall how much trouble there was in August and September when the DX was at 81.

"Risk On" is Losing Momentum

The linked article reviews

"Hoarding of Cash":

Subject: Capitalism On Strike - Why Corporations Are Hoarding Cash: Mark Spitznagel | Economy Watch

Link to March 9, 2012 'Bob and Phil Show' on TalkDigitalNetwork.com: http://talkdigitalnetwork.com/2012/03/happy-birthday-bull-market