Is the $60.3 billion November trade deficit now "paid for" as recent foreign capital-inflow numbers ($81 billion) suggest? Is the dollar's bear market over? Are we in a gold-holding pattern again?

The Dollar: Turning on a Dime

Without any change in fundamentals or even news about exchange rates the dollar turned on a dime as soon as the new year hit. On Friday, December 31, the dollar still fell to an all time low of 1.36 to the euro. On Monday, January 3, the rebound started without any advance notice whatsoever.

What caused that?

Manipulation? Investor psychology? A technical rebound? An "oversold condition"? Which is it?

Forex news reports cited all of the above in one instance or another, but what was the real reason? Are there any "real reasons" for anything anymore in financial-land?

We got a sudden repeat performance of the 2003 dollar collapse during September last year without any fundamental change in financial news or economic outlook from the earlier month dollar rebound and gold stagnation period. Now we get a sudden change back to the dollar-upside without any fundamental change in outlook. Fed rates had been rising and had been expected to rise further throughout the September-December dollar collapse, but as soon as New Years Eve revelers had slept off their hangovers, the dollar began to climb again.

Where are these things coming from? What is happening?

Who cares anymore? There's only one thing that seems to be certain: when the dollar is falling, the Dow goes up. When the dollar stabilizes, the Dow stagnates. When the dollar rises, the Dow falls.

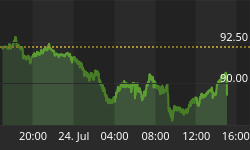

Such has been the case since September 2003 with mind-boggling accuracy - and such is still the case now. The dollar-Dow inversion is alive and well, and is best depicted by looking at a chart showing the Dow and the dollar's main "foe": the euro:

Why does this happen?

The ordinary thinking goes that a low dollar is good for US exporting companies because their products become less expensive abroad. But the effects of this usually lag by at least a matter of months, if not an entire year or longer. So, how come there is this uncanny, almost instantaneous inverse relationship? What accounts for that?

There are no textbooks on this subject. You will find nothing online or in your local library. Ask your College economics professor, and he will be stumped for an answer. So, what's up?

Since September 2003, it almost appears as if the dollar now has the same adverse relationship to the Dow as it has to gold itself. Why is that so? What changed from before 9/03?

If so, what does that say about the current stock rebound? Is it just a reflection of the falling dollar, and no more? If this is so, then investors in US stocks should take note: if they are still skeptical of gold because the current gold-bull is "just the shadow of the falling dollar", then their cherished Dow Jones average has recently fared no better.

Here is another thought: what does that say about the confidence foreign investors have in US stocks? If they only buy them when the cheaper dollar makes them more affordable, then a stronger dollar becomes an economic no-no for US policy makers. If this is the perception of US markets, the US cannot afford a strong dollar policy any longer, any comments from the administration through it's snowy mouthpiece notwithstanding.

If this is true, then the situation we face also instructs us that the dollar has become adverse to even the confounded, rigged, and artificial representation of economic value we all call "the US stock markets." In short: the dollar is now absolutely value-adverse. An increase in the price of anything that has any kind of value to Americans now has to be purchased at the expense of a falling dollar!

The evidence appears striking. There seem to be no two ways about it. It's not so much that a strong dollar is bad for US assets, as it is that only a weak dollar can induce foreign investment in US or dollar-denominated assets anymore.

Or, seen the other way around: if higher prices for US assets can only be bought at the expense of a lower dollar, then we simply have a wash. We are treading water. We are going nowhere. The only thing we have is an illusion of an increase in the value of US assets tailor made for the domestic US population.

At least one thing still remains of the old pillars of economic reality: There is at least that one perception of "value" left in investors' minds. At least they still do buy US assets (or dollar-denominated assets) when the dollar tanks. If and when that ever stops, if and when the international estimation of the value of US assets sinks so low that they won't even consider buying them when they are cheap, that is going to be the day when US economic supremacy is simply over.

How does all of this jibe with today's report of the huge November rise in net foreign investment?

It jibes perfectly.

Even if the figures are correct and not skewed at all, the dollar-Dow scenario explains perfectly why foreign investment has increased so much. Look how the Dow shot up after the election. Look how the dollar dived during the same time. If foreigners are simply scavenging for cheap US assets, then this points to one sad but undeniable truth: they will only continue to do so when the dollar is falling, making US assets cheaper for them.

At this point, it's time to make a prediction: If this explanation is correct, then the December TIC figures to be released in February should show a far lower net increase in foreign capital inflows. And if the dollar keeps climbing during January and boasts a significant increase at the end of the month, then we should see a reversal of net inflows during January when those figures are released in March.

Now, if this scenario holds true, then how far can the dollar rise?

Better question: how far can the dollar-faction afford to let the Dow to fall (as a result of the rising dollar) before foreigners will jump off the train and look elsewhere for bargains? A rebounding dollar will act like insect-repellant for foreign investors. They simply won't go anywhere near US assets if a rising dollar makes these assets smell bad' (more expensive) to them.

And that means that the trade deficit will continue to loom large on the investment horizon, no matter what these (now no longer so surprising) capital inflow figures showed in November. Only a seriously falling dollar can attract enough foreign investment to "pay" for the US trade deficit. That means a rising dollar will simply crush the US equities markets.

There is another possible explanation for this upward explosion in foreign asset inflows:

I have seen people talking about covert US Fed buying of longer term treasuries to keep long rates manageable so that consumers won't get scared out of their pants by the two-prong pinchers of rising US prices and the rising cost of debt-repayments. Some astute analysts have observed that there is a lot of activity in the bond market coming out of the Caribbean money centers. These same traders have observed that an unidentified but huge entity acting through the Caribbean money centers keeps coming in to buy treasuries as soon as a sell-off begins to develop. Could that be the Fed?

Is it possible that the Fed is making good on Bernanke's threat and is buying long term treasuries? Are those the "foreign investment inflows" we have been told about today so boisterously? Here is a snippet from a Reuters article of today:

Michael Woolfolk, senior currency strategist at Bank of New York, reckoned however that much of November's asset inflow was speculative, given an increase in investments from Caribbean money center banks. These banks are known to be financing channels for most hedge funds, which have become major players in the daily $1.3 trillion turnover of the global foreign exchange market.

Looks like they may also be financing channels for the US Fed.

A rising dollar's seemingly inevitable negative effect on the Dow will force US insiders to do whatever they need to do to prop up their beloved stock-market con game. As the Dow goes, so goes investor psychology. When the Dow finally folds, we will get Prechter's predicted (but so far not occurring) deflation scenario. Individuals and businesses will pull in their horns. Credit will contract, not because rates are high but because everybody gets scared. Then, the Fed may be forced to reverse course and drop its interest-rate pants again, exposing the nakedness underneath for all the world to see.

But the above still doesn't explain why the dollar turned on a dime in the new year.

What we have witnessed so far does not appear to be a major dollar support action by anyone - unless it's an act of covert dollar-buying by the ECB and/or euro-zone member nations. If I were to go way out on a limb I'd say that, just as the US is trying to undermine the euro by dropping the dollar too far too fast, the euro-members may have figured out they can "mess" with the US by covert dollar-support. In doing so, they can apply a fair amount of pressure on the Dow, as is evident from this chart:

Funny world, isn't it, where nations and power-blocs now appear to try and hurt each other by supporting the opponent's currency?!!!

But it doesn't have to be covert EU dollar-support that drove this reversal. It may very well be that Japan is finally acquiescing to longstanding EU demands to stop selling yen to buy dollars, which in the past forced the euro to take the brunt of the ongoing dollar-depreciation.

It is too early to tell whether this represents a definitive policy shift by the Japanese, but it is interesting to note that, although the dollar bounced against both the euro and the yen in early January, its bounce against the euro has been sustained and continues, while it fell back against the yen to levels that are now lower than they were at the beginning of the bounce. And that despite the lift it got from the foreign capital inflows data.

So, is gold "on hold" again? Yes, for the time being - but that's a good thing if you are consistently buying and saving gold (as the Chinese and other Asians do) to align yourself with the coming changes in the world monetary system. Those changes are detailed only in the Euro vs Dollar Currency War Monitor.

If you are only trading gold or gold shares for paper-profits, your long-term priorities may be a bit off. If you end up selling gold in the face of a sustained rise in the dollar, you will be doing those who truly save gold a huge favor. They'll be glad to buy it from you - for even less paper cash than it takes to do that now!

Got gold?