Summary of Index Daily Closings for Week Ending January 21, 2005

| Date | DJIA | Transports | S&P | NASDAQ | Jun 30 Yr Treas Bonds |

| Jan 17 | M A R K E T S C L O S E D F O R M A R T I N L U T H E R K I N G'S B I R T H D A Y | ||||

| Jan 18 | 10628.70 | 3589.22 | 1195.97 | 2106.64 | 113^29 |

| Jan 19 | 10539.97 | 3552.48 | 1184.63 | 2073.59 | 113^31 |

| Jan 20 | 10471.47 | 3513.42 | 1175.41 | 2045.88 | 114^05 |

| Jan 21 | 10392.99 | 3471.17 | 1167.87 | 2034.27 | 114^12 |

| SHORT TERM FORECAST (Next Two Weeks) | ||||

| TREND | PROBABILITY | Legend | ||

| Substantial Rise | Low | |||

| Market Rise | Medium | Very High | 80% | |

| Sideways | Medium | High | 60% | |

| Market Decline | Medium/High | Medium | 40% | |

| Substantial Decline | Medium | Low | 20% | |

| Very Low Under | 20% | |||

| INTERMEDIATE TERM FORECAST (Next 12 Weeks) | ||||

| TREND | PROBABILITY | Substantial | 800 points+ (DJIA) | |

| Substantial Rise | Low | Market Move | 200 to 800 points (DJIA) | |

| Market Rise | Medium | Sideways | Up or Down 200 (DJIA) | |

| Sideways | Medium | |||

| Market Decline | High | |||

| Substantial Decline | High | |||

This week the Dow Jones Industrial Average hit a new closing low for 2005, down for the third week in a row, down 165 points after rising 70 points on Tuesday. This is about as we expected as our Short-term TII indicator was positive 29.00 last Friday, but with the caveat that "a weak up move is probable." That we got. And brief too. The rally from Thursday January 13th's low capped an a-up, b-down, c-up minor rally on the first of our four possible Fibonacci turn dates identified for this week. Tuesday's top came on the 1,259th trading day from January 14th, 2000's all-time high in the DJIA. Thus January 18th, 2005 becomes the phi mate of December 14th, 2001's minor low (which came the 482nd trading day from January 14th, 2000). The ratio of 482/1,259 = .382. Once again another Fibonacci phi mate date marks a turn in the DJIA. Since 1/14/2000, there have been no exceptions. The DJIA plummeted 236 points from this latest phi turn date, closing below its December 2004 low, which is Bearish. Today's close in the DJIA wipes out all the gains of 2004, thus validating our perpetually negative Intermediateterm TII readings over the past year. Technical Analysis works.

Effective March 1st, only paid subscribers will have exclusive access to these reports.

| Equities Markets Technical Indicator Index (TII) ™ | ||||

| Week Ended | Short Term Index | Intermediate Term Index | ||

| Sep 24, 2004 | (52.25) | (42.02) | Scale | |

| Oct 1, 2004 | 25.50 | (37.23) | ||

| Oct 8, 2004 | (58.50) | (35.56) | (100) to +100 | |

| Oct 15, 2004 | (24.50) | (35.48) | ||

| Oct 22, 2004 | (15.00) | (36.93) | (Negative) Bearish | |

| Oct 29, 2004 | 39.50 | (40.06) | Positive Bullish | |

| Nov 5, 2004 | 5.50 | (35.28) | ||

| Nov 12, 2004 | (6.50) | (27.63) | ||

| Nov 19, 2004 | (50.00) | (23.18) | ||

| Nov 26, 2004 | (54.25) | (26.88) | ||

| Dec 3, 2004 | (56.25) | (30.50) | ||

| Dec 10, 2004 | (88.25) | (42.42) | ||

| Dec 17, 2004 | (37.00) | (44.25) | ||

| Dec 22, 2004 | 26.25 | (46.17) | ||

| Jan 7, 2004 | (13.50) | (37.75) | ||

| Jan 14, 2004 | 29.00 | (29.17) | ||

| Jan 21, 2004 | (25.50) | (21.83) | ||

This week the Short-term Technical Indicator Index comes in at negative (25.50), indicating a sideways to declining move is probable. This indicator is a useful predictor of equity market moves over the next two weeks, both as to direction and to a lesser extent strength of move. For example, readings near zero indicate narrow sideways moves are probable. Readings closer to +/-100 indicate with a higher degree of confidence that an impulsive move up or down is likely over the short run. Market conditions can change on a dime, or the Plunge Protection Team can come in and temporarily stop market slides, so it may be unwise to trade off this weekly measured indicator.

The Intermediate-term Technical Indicator Index is useful for monitoring what's over the horizon - over the next twelve weeks. It serves as an early warning system for unforeseen trend changes of considerable magnitude. This week the Intermediate-term TII comes in at negative (21.83).

The Dow Theory has come under attack from perma-bulls who have little respect for any stock index that isn't the S&P 500. One neo-enlightened intellect actually sent me three emails over the past two weeks saying that the Dow Theory is not even a technical analysis tool. Really? In this issue I want to cover this technical tool (make no mistake it is a relevant and terrific technical analysis tool - ignore at your own peril).

The theory was founded around the turn of the twentieth century by Charles H. Dow, then editor of the Wall Street Journal. As part of his studies, he "invented" the concept of tracking segments of the stock market separately as "averages" or indices. The theory was initially documented by him in a series of editorials published by the financial paper he ran. His view of the theory at the time was more as a barometer of business conditions which he believed would be helpful for investors. After his death in 1902, his successor as editor for the Wall Street Journal, William Peter Hamilton, took the theory to a new level of application, defining the science of the theory and applying it as a forecasting tool with considerable success from 1902 to his death in December 1929, only six weeks after arguably the worst stock market crash of all time, surely so in its repercussions.

The original indices were set up by Charles Dow in 1897 (which is why the data only goes back that far). He set up two averages. One was the rail averages (which has since migrated to the Transports) and consisted of 20 stocks. Today the Trannies still have only 20 stocks. The second average he set up was the Industrials average which at the time consisted of only 12 stocks. It was increased to 16 stocks in 1916, and 30 on October 1st, 1928 - the number of Industrial stocks in the average today. The specific stocks change from time to time due to their market capitalization and to so as to fully represent the major market segments. General Electric is the only stock that has been in the Industrials from day one through now. In 1929, the Utility stocks were pulled out of the Industrials and a separate Dow Utilities index was established which now consists of 15 stocks.

Dow Theory only concerns itself with the Transports and the Industrials. It assumes that the averages discount everything known to man. The Dow Theory sees market movements occurring at three different waves of time frames all at the same time. The Primary Trend is the broad long-term up or down movements in prices, lasting a year or more. Inside the Primary Trend is the Secondary Trend which can either interrupt the Primary Trend's progress or push it forward, depending upon whether this intermediate-term price trend is going with the grain or against it, lasting typically from a few weeks to several months or occasionally more than a year. Then there are the Minor Trends, short-term, lasting anywhere from a few days to a few weeks. Again, the Minor trend can move prices either in the same or opposite direction as the Primary or Secondary trend.

The predictive value of the Dow Theory aims at defining Bull and Bear markets. There are several tools to size up the present investing environment and forecast the future. First is values. Dow Theory believes market valuations swing from too high to too low like a pendulum, and that until Price/Earnings ratios get to overvalued extremes, something along the lines of PEs over 20, the Primary Bull trend may not be over. Conversely, Bear markets do not typically end until PE ratios become undervalued, something along the lines of under 10. Valuations are also measured by looking at the Dividend Ratios of a stock versus its long-term historical mean. Typically, Primary Bull markets are not likely to be complete until dividend ratios drop below 2 percent or so. Bear markets are not likely over until dividend-to-stock-price ratios are over 6 percent or so. These measures are not hard and fast, which is where the art meets the science. But these are general guidelines that have worked for over a century.

The other key tool that gives the Dow Theory its predictive value is the principle of Confirmation and Non-confirmation. This principle says that the two averages, the Transports and the Industrials must confirm each other. Here's how this works and why. The thinking is that in the economy, goods produced must be shipped. To gage an accurate read on the economy, production should move hand in hand with shipping. If industrial production is rising, then it stands to reason shipping should be on the rise as well. If industrial production is rising, but shipping is slowing, then it signals something is wrong with the normal flow of the markets. Perhaps excess product has been manufactured, but sales (as measured by shipping) are lagging. If goods are being shipped at a rising clip, but production is falling off, it signals something is wrong with the economy, that perhaps shipping is soon going to follow production lower since there won't be as much product to ship. If the decision-makers who produce goods based upon orders, or expected orders, are Bearish, it will be reflected in a declining Dow Industrials index. So, for a healthy economy, both the Industrials and the Transports should rise in sync.

Applying the philosophy to the averages, a change in the Primary trend of stocks must and only occurs when the two averages confirm each other. If the Primary trend in stocks was down, a change in trend to the upside is only valid if both the Industrials and the Transports rally to new highs. Should one index rally to new highs, but the other fail to do so, then the new rising trend is suspicious, and should not be trusted with your investment capital. The same applies in reverse. If stocks are in a confirmed Primary rising trend, and then one index declines to a lower low, but the other fails to do so, marking only a higher low than before, then the move down becomes suspicious, is not to be trusted, and it is assumed that the Primary rising trend remains in force. Non-confirmations also apply to Secondary stock movements.

Frequently non-confirmations occur during a Primary or Secondary trend in the same direction as the trend. For example, in a rising trend the Transports may make a higher high, but the Industrials fail to do so. That non-confirmation does not signal a trend change. It only gives pause for concern. The rising trend is assumed to remain in force since it is not necessary for confirmations of an ongoing trend to occur on the same day. Confirmations may lag, but still keep the trend in place. It can be said, however, that the longer it takes for one index to confirm the other in an ongoing trend, the more suspicious that trend becomes. It could signal that the trend is running out of gas. You like to see the two indices confirm soon to add confidence to the ongoing trend. Still, until such time as a confirmed reversal has taken place, the assumption is that the ongoing trend remains in force.

Dow Theory only considers closing prices for each day. My only comment here is that this has stood the test of time.

All of which brings us to now. The last Primary trend reversal occurred in 1999, and it was a sell signal. This has not been reversed, therefore the rally from October 2002 through December 2004 has been a Secondary rising trend inside a Primary declining trend. That signal occurred because after both the DJIA and Trannies hit confirmed all-time highs on May 12, 1999 and May 13, 1999, the Trannies failed to confirm the DJIA's higher high in August 1999. That higher high non-confirmation was then followed by confirmed lower lows in both indices in September 1999. Primary Sell Signal. This sell signal was confirmed in 2000 when the DJIA went on to reach a higher all-time high January 14th, 2000 that the Trannies failed to confirm. That non-confirmed top was then followed by confirmed lower lows in February 2000. Thus the Primary Sell signal was confirmed. The averages have not been able to give a Primary Buy signal since.

Recently the Trannies - after five years - hit a new all-time high. But the DJIA has failed to confirm, establishing a major Primary degree non-confirmation that dates back for five years. That is a very long time for a non-confirmation. Back on January 14th, 2000 the Industrials hit an all-time high of 11,722.98. The Transports hit their all-time high five years later on December 28th, 2004 at 3,811.62. This is far too long for a confirmation to the upside, and instead is a major league nonconfirmation requiring the Dow Industrials to confirm the Trannies new all-time high with a new alltime high of their own. The Industrials must now top 11,722.98 for a Primary Buy signal. That is a long-shot as they now sit 1,329.99 (11.3 percent) below that task. Worse, the Trannies have fallen below their December 2004 low and the DJIA confirmed that downside action Friday January 21st, closing below their December 10,440 low at 10,392.99. This confirmed lower low after a non-confirmed higher high is very Bearish.

Non-confirmations are essentially saying something is seriously wrong with the economy and markets, so be careful. The way Edwards and Magee put it in their outstanding technical analysis tome is, "The fact is that, in Dow Theory, the refusal of one Average to confirm the other can never produce a positive signal of any sort. It has only negative connotations," (Technical Analysis of Stock Trends, eighth edition, edited by W.H.C. Bassetti, St. Lucie Press, 2001).

The above chart shows divergences between the Dow Industrials and the Dow Transportation Averages over the past five years. What is fascinating is that every single time there was a nonconfirmation of one average by the other, a stock market crash followed shortly thereafter. Every time! This just adds to the body of evidence suggesting that equity markets sit at enormous risk of a major stock decline during 2005 and into 2006.

Why should Dow Theory be trusted? Does it work? Edwards and Magee in the above noted book point out brilliantly that had you invested in the Dow Industrials in 1897, and bought and sold based upon Dow Theory buy and sell signals for 103 years, by the year 2000 you (or your deserving heirs) would have had nearly ten times the money than had you stuck the money in the Dow Industrials and held it 103 years, with no intervening buy and sell transactions. I recommend you buy this book. The first five chapters deal with Dow Theory.

Since William P. Hamilton, other noted Dow Theorists have included Robert Rhea, and Richard Russell (www.dowtheoryletters.com). I also find Tim W. Wood's commentary valuable at (www.cyclesman.com).

Analogs are snapshots that compare current price patterns with those times of the past that we suspect are being replicated. Of particular concern to equity investors at this time are those secular (major) Bear markets of the past that we may be mirroring now. Our suspicions are high because we entered the winter period of the Kondratieff Wave back in September 2000, which is expected to last at least through 2010. It is the longest of cyclical waves. Winter is the bad season for equities. Previous winters occurred from 1835 to 1844, 1875 to 1896, 1929 to 1949, and 2000 through likely 2010.

So, we want to measure investor psychology today with that of past major Bear markets that fostered crashes in order to determine when the risk is highest of another crash. We in effect use the past as a blueprint of the future because the past patterns continue to repeat themselves. This week we highlight five different analogs of the past. 1) The DJIA from 1972 to1973 with 2004 to 2005 2) The average of the DJIA in 1929-1936 and 1968 to1975 Bear markets with the DJIA in 2000 through 2005, 3) Japan's Nikkei from 1985 to 1998 with the DJIA from 1996 to 2005, 4) The S&P 500 from May 1998 to October 2002 with the S&P 500 from October 2002 through January 2005, and 5) the DJIA from 1928 to1929 with the S&P 500 from 2004 to 2005.

In every single instance, each analog of past investor psychology is suggesting that a major stock market crash is upon us, that it has already started the slow, gradual decline phase, and that it is expected to pick up vertical speed by late February and plummet into March 2005.

This is not coincidence. This is the price pattern of the common investor psyche during Bear markets. A crash is in all probability beginning right now.

Let's explore why all these analogs are warning of an impending surprise equity slide. If you recall, back in our discussion of Dow Theory, we mentioned that one of the tools used to alert the Dow Theorist is stock valuation. We indicated that when price/earnings multiples reached historically high levels, market tops were in place and therefore equities were set to decline. For equities not to decline, the "E" portion of the equation, earnings, must grow at least as fast as the "P," Price. Well, corporate profits were actually down 27.6 billion in the third quarter of 2004 according to the Bureau of Economic Analysis, a government agency (no, you didn't hear that number in the mainstream financial press). So we cannot count on earnings to fuel further equity price growth. That leaves us with the reality of current Price/Earnings ratios in their historical context. A hard look at "P."

The following is some interesting analysis reproduced courtesy of Chris Ciovacco, Registered Investment Advisor, Ciovacco Capital Management, LLC (www.ciovaccocapital.com - visit their site for an outstanding slide show far superior to the bits and pieces I've chosen to present below), based upon historical data courtesy of Charlie Minter, Comstock Partners (www.comstockfunds.com).

Looking at 75 years of market history, the average Price/Earnings ratio for the S&P 500 for the last nine major market tops (excluding 2000's) was 18.55. The average PE ratio for the S&P 500 for the last nine major market bottoms (excluding 2002's) was 9.39. That gives us a mean PE of 13.97. PE's above the mean indicate markets are at risk of decline. PE's below the mean indicate equities are poised to rally. What do you think the PE ratio was at the so-called Bear market bottom in October 2002? Answer, a historically ridiculous 28. Does that sound like a Bear market bottom to you? Earnings grew substantially since October 2002, however the PE ratio as of December 29th, 2004 was still an outlier 20.15. How does this PE compare to other major tops in equities?

Just before the stock market crash of 1929, the market topped at a PE of 21. In 1946 it topped at 22. Just before the stock market crash of 1987 it peaked at 23. In 2000, just before the two-year, fifty percent crash, the S&P sold at a PE of 32. None of the other six major equity market tops over the past 75 years had a higher PE than now. Today's 20.15 PE in the S&P 500 certainly supports a stock market crash at this time. It ties in with the Dow Theory non-confirmation and Primary Sell Signal in force. It ties in with the analogs. Chris points out that should the S&P 500 decline to a level where its PE reaches the historical average, it would have to crash 30 percent from current levels. Should the S&P decline to its average trough PE seen at market bottoms, it would have to crash 53 percent from here. For the DJIA to fall to its historical average PE seen at market bottoms, it would have to crash 48 percent from here.

The NASDAQ sat with an obscene PE of 53.54 on December 29th, 2004. The DJIA sat at a PE of 18.11. Should anybody really listen to the perma-bulls and buy stocks for the long haul now? Yikes.

Here's the raw data: | ||||||||||

| 1929 | 1937 | 1946 | 1961 | 1968 | 1973 | 1976 | 1981 | 1987 | Average | |

| Market Tops | 21 | 18 | 22 | 19 | 19 | 19 | 13 | 10 | 23 | 18.55 |

| Market Bottoms | 8.5 | 7 | 6 | 16 | 13.5 | 7 | 7 | 7.5 | 12 | 9.39 |

The above analysis compares the number of Dow Jones Industrial Average Stocks that are sitting above their 10 Day Moving Average with the future price action of the Dow Industrials. The correlation is terrific. Whenever the percentage rises above 80 percent, the Dow Industrials are overbought and a short-term trend reversal to the downside is probable. Whenever the percentage above their 10 DMA falls below 15 percent, the Dow Industrials are oversold and a short-term upside reversal is probable, though not necessarily imminent. Friday, January 21st's reading was 10.00 percent, indicating at least a short-term bottom is near.

The top chart on the next page is a contrary sentiment indicator, the 10 Day Moving Average CBOE Call/Put Option ratio. No buy signal yet. Significant bottoms occur when this ratio falls to 1.00, then turns decisively up. We currently sit at a 1.15 reading, meaning the sell signal generated December 2nd, 2004 remains in force.

The chart below shows a measure of Bullish/Bearish sentiment, the SPX to VIX ratio. It is a contrary indicator under the theory that once the pendulum swings from over-pessimism to overoptimism, the pendulum is about to swing back again the other way. This has implications for stocks. Whenever this ratio rose above 68, the S&P 500 not just fell, but crashed. Whenever this ratio fell below 35, nice rallies started. Two exceptions. Back in 1998/1999 we saw a long-term pattern that led to an extreme peak. Because it took so long to develop, the subsequent crash was the start of a massive Bear market. Same pattern has showed up again from 2003 into 2004, meaning another major Bear is about to start, or may in fact be starting. Note the similar upside down "V" patterns evidencing the pinnacles. Friday's reading sits at a Crash-warning level of 81.33.

Here's how things are shaking out. The Dow Jones Industrial Average shown above (courtesy www.stockcharts.com) has confirmed that a Head & Shoulders Top is in place - meaning the probability of it reaching its minimum downside target is high - with the decisive break below the neckline Thursday and Friday of this week. Momentum is down hard as Minuette degree wave iii unfolds. The minimum downside target is 10,100 per the H&S pattern, which could very possibly be the bottom for Minuette iii. By then this market should be oversold at which time we'll get a small bounce, Minuette degree iv up. Then one final panic selling drop for the bottom of Minor degree wave 1. If the analogs are correct, and this is a multi-month crash unfolding, then once the oversold condition gets worked off with a Minor degree 2 retrace rally, that should set the stage for one very nasty decline from late February into March, Minor degree wave 3 down. By then, the Fed should be dropping money from cargo planes all across America. By then, Bulls should know something is very wrong, that this is different than they expected for 2005, and Bearish sentiment should rise fast. The VIX will likely be headed toward 30 by the middle of March 2005.

Unannounced, the DJIA blew through its 50 day moving average support this week and is making a beeline for its 200 day MA. The DJIA was the lone major average that had not broken below its December 2004 low - until Friday. It took a while to break under strong support at 10,500, but once it did, buyers ran. New lows are rising. Once both new lows and new highs exceed 90, it will be a crash signal. Watch for this sign carefully.

Back on December 3rd, 2004, in issue no. 104 (available in the archives at www.technicalindicatorindex.com) we wrote, "The Dow Transportation Average has risen 25 percent since August 2004 without a correction - which meets the criteria for a Parabolic Spike. The PE for this index is over 90x. What we have here is a manic bubble. Parabolic Spikes do not have soft landings. Once the air comes out of this balloon, this index is going to crash and burn."

Since December 30th's 3,823.96 intraday top, the Trannies have plummeted 352.79 points (9.2 percent) in just 15 Trading days. This was predicted perfectly by the patterns on the chart above. It looks like a five-wave impulse wave down completed Friday, January 21st, the bottom of Minuette degree wave i down. The RSI is oversold - although it could go lower - and the MACD is very oversold and should soon curl up. However, that said, we haven't really seen a selling panic yet, so either prices could continue to crash from here, or more likely, prices could retrace into a Minuette degree wave ii rally. Then, once conditions are no longer clearly oversold, a devastating decline, Minuette degree wave iii should unfold. Prices should eventually return to the start of the Rising Bearish Wedge - to around 2,750.

It is normal for the Trannies to lead the Industrials on the way down during major declines. Happened in 1999/2000. Could be happening again now.

The S&P 500 is in big trouble. There is no other way to put it. The Elliott Wave count shows that prices are now declining in a Micro degree wave 3 down of a larger degree Minuette degree iii down. This should have the power to push prices down to the minimum downside target of a now confirmed Head & Shoulders top pattern, confirmed because prices fell decisively below the neckline this week.

The pattern that clued us into the current decline is the Rising Bearish Wedge shown in blue converging lines above. The bad news for the SPX is that this pattern indicates prices should return to the base of the pattern, in this case to 1,090ish.

Momentum is down, but approaching oversold levels. The RSI is also at oversold levels. However, during crashes, prices can dwell in oversold territory for a while. A clear sign of an imminent retracing correction would be if we saw panic selling where breadth is just simply horrible. That would temporarily exhaust the selling and allow some bottom fishing buying. However, the Analogs and longer-term Elliott Wave count warn that this Bearish environment is going to be around for a while.

The Economy:

Leading Economic Indicators rose 0.2 percent in December 2004, according to the Conference Board, a private research group. This is the second increase in a row after five straight months of decline. The problem with this month's reading is that the huge post-election rally was a key reason for the increase. With January's sharp decline, how "leading" December's number is becomes questionable. The capital goods and manufacturing components did poorly.

The Federal Reserve bank of New York reported that Manufacturing Activity fell twenty-five percent in January 2005 to 20.1 from 27.1 in December. New Orders fell 41.8 percent. The headlines reported that activity "slipped." That's polite.

The Commerce Department announced that Housing Starts rose their highest monthly amount in seven years in December. Hope there will be folks to buy those buildings.

The Labor Department reported that the Consumer Price Index fell to practically nothing, to 0.1 percent in December, down from November 2004's 0.2 percent. Yep, nothing is going up in price. Have you noticed? Stick that in your vinyl wallets, dear Social Security recipients. Ah, who knows, maybe it was all those Christmas discounts at Wal-Mart that got Secretary Chao's attention. Socks, underwear, DVDs in the big bins. Yeah, that's probably what happened. More than enough to offset that tuition bill, that car insurance premium, that home-equity line-of-credit payment. If only there was Wal- Mart University, or Sam's Financial Corporation. If only.

The Fed jawboned its deep rooted concerns about the accommodative levels of short-term interest rates. Philadelphia President Santomero painted a rosy picture for the economy in 2005, hap-haphappy times are on the way. Trade deficit's gonna shrink, inflation will remain tame (of course as long as Labor calculates the number, that's no stretch Anthony), lots of folks going back to work, 4 percent GDP growth. Is it true he also proclaimed that lawyers will be doing more pro bono in 2005, teachers unions will be disbanding because, well, they just love kids, and baseball is rolling back ticket prices?

Not knowing quite how to make the seasonal adjustments for the "quirks" around the holidays (I'm not making this up - the article was reported at www.cnnmoney.com Wednesday, January 19th) , the Labor Department decided to take a wild guess that Jobless Claims fell 48,000 last week. Not sure if they used darts or some high-tech, taxpayer funded, random number generator. Maybe somebody at CNBC will ask the Secretary next time she comes on - and of course totally approve.

And the sum total of all of this is that January's University of Michigan Consumer Sentiment Index fell to 95.8.

Money Supply, the Dollar, & Gold:

M-3 fell 8.7 billion for the latest week, but it isn't the third week yet. The Fed likes to raise M-3 by huge $50 billion chunks in stealth fashion about every three weeks when it tries to support equity markets during high crash-risk periods like now. That's what it did back in April/May 2004, successfully staving off a crash. Look for M-3 to jump next week. Still, M-3 is up $63.9 billion over the past month, an annualized rate of growth of 8.8 percent. That's not the sort of growth rate in money supply a Federal Reserve worried about inflation tolerates. It is a unique approach to Money Supply management. Raise short-term interest rates, jawbone your concerns about inflation, promise you'll be vigilant to fight inflation and then print as much money as you can. Leak to the mainstream financial press that, hey, you really don't control money supply (which of course is pure and utter hogwash). The goal, I suppose, is to fake out the Bond market, hoping to keep long-term rates tame while supporting equities. Sooner or later the truth always comes out and markets respond accordingly. If M-3 is truly going up 8.8 percent, then look for the Dollar to continue its descent and for Gold to climb.

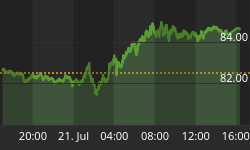

We tweaked the Elliott Wave count on the Trade-Weighted U.S. Dollar to reflect a cleaner Minor degree wave 4 up that may have finished this week. Friday's intraday high was a Fibonacci 38.2 percent retrace of Minor degree wave 3 down, and so could very well represent the top of Minor degree 4. While Minuette c up this week looks small in relation to wave a up, that's okay as it is essentially a Fibonacci 61.8 percent of Minuette a, further supporting a short-term top. The Dollar fell impulsively Friday from its 84.00 intraday high, further adding to the evidence that Minor degree wave 5 down has started. Our belief is that the Dollar has one more leg down to go, Minor degree wave 5, that should take prices back down to the lower boundary of its downward trend-channel, into the high 70's. This count looks the most proportional to us at this time, an important component of accurate EW labeling. An alternate count is that the U.S. Dollar bottomed Friday December 31st, and that the rally to today's high is wave 1 up of Intermediate degree A of Primary (2) up. While we fully expect a strong rally in the Dollar sometime in 2005, an A-B-C primary degree (2) up move to correct the two year decline, we believe the start of that rally is a few weeks, or at most, a few months away. The RSI turned down Friday, as did the MACD. Momentum may be turning down.

Gold finished its Bearish Flag pattern shown two weeks ago, at the bottom boundary of the Ascending Bullish Triangle pattern, completing Minor degree corrective wave 4 down. Next should be a decent rally that has the potential to reach 500 over the next three to six months, a fifth of a fifth wave to complete primary degree (1) up in this Bull market in Gold. This target is calculated by taking the widest distance of the Ascending Triangle and adding that to the point of the upside breakout. Both the RSI and the MACD have reversed up from oversold levels. If the Fed is going to pump M-3 like we think they will, Gold will benefit.

It looks as if the Gold Bugs Index ($HUI) is going to get caught in the downdraft of the general equity market slide now underway. There is a difference between Gold stocks and Gold the metal. The metal is above ground, supply certain and limited, and is a monetary store of value. The Gold stocks are managed companies subject to risks of any company - legal, regulatory, operational, managerial, production, research and development, resource availability and cost, etc... The bulk of its Gold inventory is underground, quantity and extraction uncertain. This puts the $HUI in the unique category of a hybrid, subject to occasional general equity market influence. Now is one of those times.

The first leg down inside the C wave down of an an A-down, B-up, C-down corrective Intermediate degree wave 2 looks complete, with Minuette degree ii up underway. Given the negative technical big picture for stocks, we don't believe this countertrend rally will carry much force, possibly lifting prices to the 218 area, a 38.2 percent retrace of the decline since November 5th's 248.18 high, which has essentially been a 19.3 percent crash. A rally from here is not starting anywhere near the previous lows for the MACD, nor RSI, a clue that once the corrective Minuette degree wave ii is complete, more strong downside action is likely.

Based upon the Elliott Wave count, a 38.2 percent retrace of Intermediate degree wave 1's rally from 35.31 on November 16th, 2000 to 250.59 on January 6th, 2004 suggests a bottom from the current Intermediate degree wave 2 decline of 168.35. A 50 percent retrace takes prices to 142.95. A 61.8 percent retrace drives prices to 117.55 before the next major intermediate Bull run gets started. We favor the 38.2 percent or 50 percent retrace scenarios because in addition to the EW count, a Bearish Head & Shoulders pattern also suggests more significant downside is probable, that once prices break decisively below 200, a minimum downside target could drive prices to as low as 152ish. Interestingly, should Minor degree C end up equal to Minor degree A, that would suggest a bottom of 154, very near the H&S target. After the carnage, we should be at the bottom of Minor degree C of 2, to be followed by a powerful rally for several months or even years, Intermediate degree wave 3.

Silver (chart courtesy of www.stockcharts.com) has formed an unconfirmed Bullish Head & Shoulders bottom. A decisive rise above 7.00 portends at least 7.50 short-term. It looks as if the Bearish Flag pattern pointed out a few weeks ago accurately forecast further decline, but failed to hit its targeted minimum low. Such failures with Flag patterns are rare.

The charts on the next page examine Light Crude ($WTIC). No change from last week. Long-term, prices remain nicely inside their rising Bullish trend-channel. The Elliott Wave count for the rally since 2001 suggests there is one more multi-month meaningful increase in Crude prices coming, once Intermediate degree wave 4 completes. It is possible wave 4 finished in December '04 and that a higher thrust is just getting started. A move to the upper trend-line would make sense as the other four turns bounced off upper and lower boundaries. That portends Oil rising to $60/bbl over the next 3 to 6 months, which fits with the Bearish stock charts. However, there is also the possibility that Oil is forming a Bearish Head & Shoulders pattern that portends prices declining to $27. For that to happen, prices must soon break below $41/bbl.

Bonds and Interest Rates:

Bond Prices broke higher as we expected per our Elliott Wave count last week. This is instructive for those who suggest that EW doesn't work. The only way we could have known Bond prices would rise was the EW count. Both the RSI and the MACD were neutral. The EW count needed a Minuette fifth to complete and that is what we based our forecast upon. This week Bonds broke higher from their Minuette degree wave iv bottom.

The long-term Head & Shoulders top is still in play, and unless prices blast past the top of the Head, above 121.45, the pattern will remain in force. It is a massive creature with ominous repercussions should the highly reliable pattern be confirmed. To confirm, prices would have to drop decisively below the neckline, below 100. If that were to occur, the minimum downside target would be 79- ish. The Elliott Wave count we believe to be most accurate at this time has prices completing the first three waves of a five-wave impulse rally that will wrap up Minuette degree v of corrective Minor degree c of an a-b-c retrace. From there we expect the Trade Deficit and Dollar damage to catch up to Bond prices as they head lower hard and fast. The only thing delaying this would be a massive deflationary Recession. But even then, the Fed would likely pump so much money into the system, Bonds would tank anyway. This rise in long-term rates that we expect may not begin for another few months, but when it comes, it should spell disaster for the Real Estate Bubble.

This chart shows the short-term Elliott Wave structure for Minuette degree wave v, the final wave before a Top is reached in Bonds for a very long time.

The count shows that we are in the third wave up of a five-wave impulse rally. Inside that third wave (micro degree wave 3 up), we have completed three waves of a five-wave up sequence. Next, prices should decline as Submicro degree wave {4} down, then rise as {5} up to complete larger degree Micro 3 up. Then one more down-up sequence to bring Bonds to an Intermediate term top.

It seems to us that Bonds smell an equity market crash and a consequent recession, thus they are rallying in spite of the falling Dollar and record Trade Deficits. However, the Fed will most likely have to abandon its interest rate tightening program, and instead flood the system with liquidity to stop an equity calamity. All that additional money supply will lead to a sell-off in Bonds, a massive decline in Bond prices, and substantial increase in long-term interest rates in fulfillment of the Massive Long-term Head & Shoulders top pattern.

Bottom Line: If you consider all the evidence, it is at best a time for the sidelines. There are so many ominous technical signs right now. Caution remains warranted.

"But you shall receive power when the Holy Spirit

has come upon you; and you shall be My witnesses

both in Jerusalem, and in all Judea, and Samaria,

and even to the remotest part of the earth."

And after He had said these things, He was lifted up

while they were looking on,

and a cloud received Him out of their sight.

And as they were gazing intently into the sky while

He was departing, behold two men in white clothing stood beside them;

And they also said, "Men of Galilee, why do you stand looking

into the sky? This Jesus, who has been taken up

from you into heaven, will come in just the same way

as you have watched Him go into heaven."

Acts 1: 8-11

Our Paid Subscriber base is growing rapidly, this past week especially. Many thanks to those of you who have joined our Paid Subscriber family, enjoying the Early Bird 32 percent discount of $169 per year for a minimum of 80 issues, plus access to Trader's Corner, our Proprietary Short-term and Intermediate- term TII indicators and Archives.

Effective March 1st, 2005, McHugh's Financial Forecast & Analysis will only be available exclusively to our Paid Subscriber Members. To subscribe, go to www.technicalindicatorindex.com and click on the Subscribe Today! button. Anyone subscribing before March 1st, 2005 will have their renewal date extended through March 1st, 2006.

2005 Promises to be volatile, with many surprises and opportunities along the way. If this market is crashing, you won't want to be caught without our cut-to the-chase reporting and unique analysis. We hope you will join us for this exciting adventure!

| Key Economic Statistics | ||||||||

| Date | VIX | Dec. U.S. $ | Euro | CRB | Gold | Silver | Crude Oil | 1 Week Avg. M-3 |

| 7/16/04 | 14.43 | 87.12 | 124.36 | 271.50 | 406.8 | 6.72 | 41.25 | 9238.8 b |

| 7/23/04 | 16.50 | 89.23 | 120.88 | 269.50 | 390.5 | 6.33 | 41.71 | 9259.9 b |

| 7/30/04 | 15.27 | 90.12 | 120.10 | 267.00 | 391.7 | 6.56 | 43.80 | 9272.3 b |

| 8/06/04 | 19.34 | 88.45 | 122.69 | 268.25 | 399.8 | 6.77 | 43.95 | 9267.9 b |

| 8/13/04 | 17.98 | 87.97 | 123.68 | 269.19 | 401.2 | 6.62 | 46.58 | 9250.2 b |

| 8/20/04 | 16.00 | 88.22 | 123.03 | 279.50 | 415.5 | 6.87 | 46.72 | 9261.9 b |

| 8/27/04 | 14.74 | 89.80 | 120.20 | 275.00 | 405.4 | 6.58 | 43.18 | 9298.6 b |

| 9/03/04 | 14.28 | 89.56 | 120.66 | 275.25 | 402.5 | 6.59 | 43.99 | 9288.7 b |

| 9/10/04 | 13.75 | 88.60 | 122.61 | 272.50 | 403.8 | 6.16 | 42.81 | 9281.1 b |

| 9/17/04 | 14.03 | 88.10 | 121.76 | 275.75 | 407.6 | 6.28 | 45.59 | 9275.7 b |

| 9/24/04 | 14.28 | 88.59 | 122.57 | 278.50 | 409.7 | 6.42 | 48.08 | 9320.5 b |

| 10/01/04 | 12.75 | 87.77 | 124.07 | 284.75 | 421.2 | 6.94 | 50.12 | 9336.5 b |

| 10/08/04 | 15.08 | 87.55 | 124.13 | 287.60 | 424.5 | 7.29 | 53.31 | 9355.6 b |

| 10/15/04 | 15.04 | 87.20 | 124.73 | 286.45 | 420.1 | 7.11 | 54.93 | 9320.8 b |

| 10/22/04 | 15.28 | 85.97 | 126.46 | 287.00 | 425.6 | 7.33 | 55.17 | 9336.9 b |

| 10/29/04 | 16.27 | 84.98 | 128.85 | 284.75 | 429.4 | 7.30 | 51.76 | 9351.5 b |

| 11/05/04 | 13.84 | 83.89 | 129.46 | 283.00 | 434.3 | 7.50 | 49.61 | 9353.5 b |

| 11/12/04 | 13.33 | 83.71 | 129.85 | 283.50 | 438.8 | 7.62 | 47.32 | 9351.5 b |

| 11/19/04 | 13.50 | 83.32 | 130.13 | 287.25 | 447.0 | 7.60 | 48.44 | 9342.5 b |

| 11/26/04 | 12.78 | 81.81 | 132.93 | 288.75 | 449.5 | 7.59 | 49.44 | 9356.7 b |

| 12/03/04 | 12.96 | 80.98 | 134.53 | 284.75 | 456.0 | 7.99 | 42.54 | 9372.5 b |

| 12/10/04 | 12.66 | 82.59 | 132.36 | 276.25 | 435.4 | 6.74 | 40.71 | 9373.1 b |

| 12/17/04 | 11.95 | 82.20 | 132.90 | 285.25 | 442.9 | 6.80 | 46.28 | 9369.2 b |

| 12/22/04 | 11.45 | 82.01 | 134.06 | 282.50 | 441.4 | 6.93 | 44.24 | 9383.7 b |

| 1/07/05 | 13.49 | 83.72 | 130.62 | 279.25 | 419.5 | 6.44 | 45.43 | 9441.8 b |

| 1/14/05 | 12.43 | 83.13 | 131.03 | 283.22 | 423.0 | 6.59 | 48.38 | 9433.1 b |

| 1/21/05 | 14.36 | 83.34 | 130.60 | 281.85 | 426.9 | 6.81 | 48.53 | - |

Note: VIX, Dollar, Gold, Silver & Oil are up. Gold and Dollar both up.