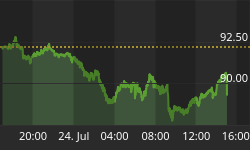

After a reasonably long period of sustained and occasionally dramatic escalations, commodity markets in general, and precious metals markets in particular, have declined. This is normal and healthy behavior, even if it is uncomfortable for some market participants. Readers with a long memory will remember the 1970s gold bull market, where the gold price advanced from $35 to $850 per ounce – though in 1975, in the middle of that epic bull market, the gold price declined by 50%. While a 50% decline is a near-religious event for many market participants, particularly those on margin, it is instructive to note that at the bottom of the retrenchment the gold price was up threefold from its $35 low, and that gold went on to increase eightfold in price after the bull market resumed. It is thus important to recognize that cyclical retrenchments are a normal and healthy feature of a secular gold bull market.

Readers should consider whether the reasons for the gold market are intact. Has gold's decline made it more likely that sovereign debts can be serviced or that unfunded obligations can be met? Does it mean that insolvent banks are now healthy? Does it mean that creating trillions of unbacked dollars and euros and renminbi will have no consequences? Of course not. We are simply uncomfortable with volatility.

Gold's Current Weakness

Let's examine some factors that may have contributed to gold's current weakness and think about the probabilities of those factors contributing to further weakening in the gold price.

For the past ten or twelve years, the gold price has been in a steady state of advance. In the near term, some participants probably took some profits, and high prices also probably contributed to demand destruction in industrial fabrication and jewelry demand. A softening of the gold price is likely to reverse the effects of price-induced conservation and substitution, even while investment demand, measured by gold funds and the ETF industry, continues to be strong.

Equity and debt markets appear to be stabilizing as a consequence of quantitative easing in Europe, the US, and China, and the apparent easing of concerns in Greece. This flood of liquidity has forced interest rates down as well as bond and deposit yields, pushing savers into longer durations and riskier instruments – including equities – and lowering servicing costs for debtors, which in turn has lowered perceptions of default risk. The markets appear more confident, and hence gold's attractiveness as insurance is fading. Some of us believe that the root word of confidence is "con," just as I believe the correct phrase for quantitative easing is "counterfeiting." It would appear that in excess of $4 trillion of new currency units have been introduced into the system, with no concurrent increase in underlying wealth in the form of goods or services. This does not make me find gold less attractive relative to fiat currencies or sovereign debt. How about you?

Physical demand in India and Vietnam has been constrained by excise and import taxes on gold in the case of India, and increased regulation in Vietnam. The constraints on physical demand in India has had an important impact on overall gold demand, and has become a hot political issue in India. Gold merchants were on strike concerning the excise tax, further constraining demand. It is worthy to note that South Asian societies have a deep-seated, cultural attraction to gold, and that the fairly recent removal of the taxes they just reinstated was a consequence of widespread smuggling and informal trading in gold. I suspect that central government interference in the Indian gold market will be ineffective and ultimately inconsequential.

Small, commodity-oriented institutions such as hedge funds have experienced strong outflows of equity capital and constrained access to debt financing, which has caused them to engage in forced liquidation of precious metals holdings. This is true, and in my opinion will continue. I believe, however, that if black swan style events destabilize other markets, the gold ETF industry and gold trusts like Sprott Physical Gold will easily absorb the remaining institutional bullion hoards. Further, Sprott has firsthand knowledge of the strong interest among sovereign wealth funds in increasing their bullion holdings.

Gold Equities

Since late 2010, gold equities have underperformed the commodity, and this underperformance has continued, and perhaps increased, as the gold price has declined. These twin trends are uncomfortable to participants in the gold equities markets. Let's examine some of the factors that may have contributed to the underperformance of gold equities relative to gold, and the probable consequence of current market conditions.

It is important to remember that for much of the last decade gold equities outpaced gains in the metals. In fact, the escalations in gold equities pricing became so acute that Canadian analysts were describing companies selling at premiums to their net asset value as "undervalued," because their premium to net asset value (i.e., what they are worth) was less than the industry standard. Always remember, markets work! This prior overvaluation was an important cause of the sector's subsequent undervaluation. The expectations built into gold equities valuations, even relative to gold, were simply unsustainable. In particular, the valuations accorded the junior gold sector were best described as "a bubble in search of a pin." The pin was found. History has shown that markets cure periods of overvaluation; and I suspect that they will also solve this period of undervaluation, relative to bullion, as well.

The emergence of bullion-linked equity instruments like the Sprott Physical Gold Trust and the various Gold ETFs allowed securities investors a new, low-cost, convenient way to participate in the gold markets. These developments at once spurred demand for bullion to back these equity-like instruments and constrained demand for gold equities as investors switched from traditional gold equities to bullion-like equities. I believe this phenomenon was particularly evident as a consequence of the relative overvaluation of gold equities described in the preceding paragraph. Given that the relative attractiveness of bullion-like equities to traditional gold equities was greatest when the gold equities were overpriced relative to bullion, I suspect this attractiveness will lessen now that gold equities are more attractive relative to bullion.

Gold equities were punished, both absolutely and relative to bullion, by their relative corporate underperformance. Many analysts, myself prominently among them, were dismayed at the gold mining industry's abysmal corporate performance during the last decade. The industry's operating cash generation in the face of a gold price escalation from $260 per ounce to over $1,200 per ounce was inexplicably poor. The companies' continued equity issuances in the face of these increases in the gold price meant that existing holders were continually diluted, even as their earnings expectations were always disappointed. Investor fatigue – in fact, investor disgust – was the natural and healthy response to this performance.

Now, even though equities prices continue to decline, corporate performance is increasing, and increasing dramatically. A cursory look at producers' income statements tells a dramatic story: earnings and cash generation, on a per share basis, are rising in dramatic fashion. Capital expenditures are increasingly funded with internally generated cash rather than equity issuances or debt. In fact, even in the face of the gold equities decline, many gold producers are generating cash so fast that even after funding hefty capital budgets, they are able to return cash to shareholders in the form of stock buybacks and increased dividends.

The Juniors

The junior gold industry magnified these problems; and the market's response has been proportionately dramatic. It is critical for gold stock speculators to remember that the junior market, in aggregate, is always overvalued. If we were to merge every gold junior in the world into one entity (let's call it Junior Goldco), that company would lose (profits and corporate acquisitions less industry expenditures) somewhere between two billion and eight billion dollars per year. What should we pay for this enterprise – what is the correct price-loss ratio? Should the industry be priced at five times losses? Ten times losses? Higher?

The performance of individual junior issuers often attracts unwitting capital to the entire sector, and that phenomenon never ends well. Many gold bugs decry government-sponsored inflation, the profligate issuance of unbacked fiat specie (quantitative easing), but ignore the fact that the private sector (in this case the TSX Venture Exchange) is better than the government at everything, including counterfeiting. Many speculators hoped that the junior markets would respond the way they did in the late 1970s where a genuine shortage of equity led to amazing share price escalations, but they ignore the fact that the regulatory and industry infrastructure now exists to print away any amount of speculative demand for the sector. Beginning in 2009, the junior industry drowned investor demand in newly issued equities at unsustainable prices. Speculators bought this paper without apparent regard to price or quality.

How do we address this problem? It is already being addressed by price. The price declines in the TSX Venture have been spectacular, and investors who've lost 50% on their portfolios are unlikely to welcome the opportunity buy newly-issued loss opportunities. Just as the unwary speculators previously bought issues without regard to quality or price, they are now selling them without regard to quality or price. Remember that it is the incredible performance of a small number of individual issues that attracts capital to the whole sector, and we see several very promising juniors marked down like so many of the Vancouver frauds. When irrationally exuberant expectations give way to irrationally negative expectations, opportunity is born, and a correction is at hand.

Market Volatility and Institutional Disintermediation

The violent declines we observed in 2008 and the market volatility we experienced last year unnerved investors and speculators. These declines and volatile markets and a contraction in short term credits all contributed to unprecedented investor redemptions at hedge funds and mutual funds. The volatility we experienced has made individual investors cautious, constraining their participation in gold equities markets, and inclining them to "sit on the sidelines." Institutional redemptions (disintermediation) have caused them to be strong net sellers. With constrained buying and forced selling, is it any wonder we experienced declining markets?

It is my belief that this year we will experience much more of the volatility that shook markets last year. In fact, I believe the volatility index will be above thirty for extended periods of time. This volatility will change the dynamics of the markets in important ways, I believe for the better, but more on that later.

Institutional disintermediation will continue, albeit at slower rates, given the smaller amounts of remaining assets. Mutual fund assets across all asset classes (except ETFs) have been static for some years, and other institutional pools outside Sovereign Wealth Funds and pension funds are showing similar declines. These changes in the nature of market participants and shifting market conditions will change the underlying market.

Now the Good News: Discovery And Consolidation

The markets are a lot less expensive than they were, and this can only be good news for buyers. Markets work, as we have said. Expensive markets collapse of their own weight, cheap markets rise as greed overwhelms fear. But I believe even better news is at hand for the intelligent and discerning investor and speculator. All gold equities have gone down, "the good, the bad, and the ugly." But there is no requirement that readers confine their purchases to the bad and the ugly!

One consequence of the long bull market we had in gold equities, in their overvaluations and in their continued equity issuances, is that literally billions of dollars have gone into exploration. While exploration is a risky business, and while most of the money was doubtlessly wasted, a substantial amount was well spent. For this reason I believe we are on the cusp of a very nice "discovery cycle."

As experienced junior gold speculators know, nothing adds to share value like discovery. Speculators will fondly remember hundredfold profits from discoveries like Diamond Fields and Arequipa. We are now truly in a discovery cycle, one fueled by sustained capital investments in unprecedented amounts. Better yet, we have been able to explore frontier terrain that was off limits due to politics or social turmoil. This will add spectacular real value, and this prospectivity is discounted in the current market.

These discoveries will lead to corporate merger activities. The large intermediate and major mining companies need to acquire new economic projects in order to continue to exist. Every day they produce, their business gets smaller. The twenty-year "bear market" in gold equities that ended in 2002 constrained these companies' ability to explore, so now they must acquire. As a consequence of the improved corporate cash-generating capabilities, they can afford to both acquire other companies as well as develop the projects they acquire. They can afford to acquire each other, too, eliminating wasteful duplicate general and administrative expenditures and enhancing shareholders' returns.

Discoveries and takeovers add liquidity and hope to a market lacking both.

What To Do

First, recognize that markets work, but only in the longer term. If you can't handle that, find another avocation. The cure for low prices is low prices; the cure for high prices is high prices. In order to sell high, you must buy low. What is the appropriate response to a strong market? Sell! What is the appropriate response to a weak market? Buy! Be a contrarian or be a victim.

Second, understand that the junior gold sector is a trap; it is valueless. Individual issues can make you fabulously wealthy, but the sector will inevitably bankrupt you if you buy the sector. Stock picking is the key.

Next, don't buy yesterday's market. The institutional sector has challenges, like disintermediation, to overcome. The institutional momentum stocks that led the last rally, particularly the very large, low-grade, capital-intensive stories that appealed to the "leveraged to gold" crowd, will not work as well as the higher-grade deposits where return on capital employed will lead to a takeover. Where our ultimate buyer used to be a momentum- and liquidity-driven institution, our new exit will be a larger mining company.

Understand that more of our profits will come from a smaller number of successful speculations. Discoveries and takeovers will lead to outsized gains while the remainder of the sector stagnates, at best. Differentiate qualitatively, prune your portfolio mercilessly, and act as a contrarian.

Last, if you have the courage and the means, this could be an epic year for private placements. Issuers were reluctant to raise capital last year as a consequence of declining equity prices, but they continued to spend. They have, as an industry, pursued an illogical circular exercise: spending money to generate news… to increase share prices… to raise money. This year many will have to raise equity irrespective of market conditions, and the small institutions and mutual funds that funded them so generously in the past will probably be unable to do so in the future. Back only the best teams and good projects. And go for a warrant!

While we may not enjoy the rewards for contrarian acquisitions this year, I am certain we will be well rewarded over time.

Attendees at the upcoming Casey Research Recovery Reality Check Summit will doubtless hear more from Rick on this subject as well as several others. If you weren't fortunate enough to grab a seat for this sold-out event, don't despair: you can hear every minute of his – and 30 other financial luminaries' – presentations. And if you act fast, you can get them at a seriously discounted price.