Before the markets opened on May 30, a Dow Jones article captured the serious nature of the escalating crisis in Spain:

European stocks fell Wednesday as the euro sank to its lowest level since July 2010 and Spanish bond yields soared, with concerns over Spain mounting. "Investors are heading for the exits once again as fears for a Spanish economic collapse heads closer to becoming a reality," said Mike McCudden, head of derivatives at Interactive Investor. "It appears to be only a matter of time before it's not just the banks that need bailing out, but the country itself," he added.

"The ECB's rejection of the Spanish government's plan to recapitalize Bankia...puts Spain on the steps of the region's fiscally based liquidity hospital, the European Financial Stability Facility/European Stability Mechanism. It looks increasingly likely that it will be knocking on the door soon asking to be admitted," said JPMorgan. "Spain looks to have gotten to the point where it cannot bear the burden alone. The Spanish government recognizes the need for burden-sharing, but it does not want the kind of burden-sharing that was made available to Greece, Ireland and Portugal," it added.

The markets in the U.S have been relatively calm having avoided new lows for six trading sessions. U.S. investors expect the European Central Bank (ECB) to bail out the markets once again. As we outlined in detail on May 26, the market may be underestimating the problems associated with the narrowing list of possible policy responses in Europe.

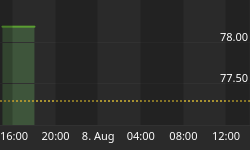

As shown in the chart below, on Wednesday morning the yield on a ten-year Spanish bond hit 6.70% for the first time since November 2011. If the ECB had a "solution" with little in the way of negative consequences, it is logical to assume they would have acted already. The ECB will take action at some point, but the low-hanging fruit is no longer on the policy-response tree.

At 7:00 a.m. EDT Wednesday, Bloomberg reported on a possible policy response in Europe:

The European Commission called for direct euro-area aid for troubled banks and touted common bond issuance as an antidote to the debt crisis now threatening to overwhelm Spain. The commission, the European Union's central regulator, sided with Spain in proposing that the euro's permanent bailout fund inject cash to banks instead of channeling the money via national governments... Proposals for more liberal use of European bailout money are likely to face resistance in creditor countries such as Germany, Finland and the Netherlands, the scenes of growing taxpayer opposition to more aid.

Since they are all flawed in some way or involve having Peter bail out Paul, the expression "likely to face resistance" has been common in recent media reporting. When push comes to shove, Europe will do something. The question is how low do the markets have to go to qualify as a shove.

The tables below, originally shown on May 26, have been updated as of the May 29 close. Even while the S&P 500 tacked on 14 points, Treasury bonds (TLT) and the U.S. Dollar (UUP) had very modest declines showing risk-averse investors were not impressed with the "good" news from Greece and the Wall Street rumor of a giant stimulus package coming from China. The tame reaction from TLT and UUP was one of the reasons we did not buy into Tuesday's rally.

While the S&P 500 and EWG recaptured two of the support levels in the table below on Tuesday, it appears as if those levels will be surrendered early in Wednesday's session.