If you missed yesterday's comment "From May Day to Mayday," you can find it here.

If there were any question whether the recent weakness seen in the economic figures were a payback from a mild winter or an actual slowdown in activity, today's numbers essentially dispelled that question. The Payrolls numbers were horrendous. The Labor Department reported that only 69,000 new jobs were created in May, but also revised down prior estimates of jobs created for the last couple of months by a net -49,000 jobs. The net of +20,000 jobs does not compare favorably with pre-data expectations of +150,000. If this is payback for the weather effect, it means the rate we are paying back from was already lower than people thought it was.

The Unemployment Rate rose to 8.206% from 8.098%. The workweek fell, but is still okay compared to last year (see Chart) although it has never stabilized at full "recovery" levels. The labor force participation rate improved, which was the only bright mote, but of course that is one reason that the Unemployment Rate rose.

The perception of the man on the street, as indicated in various surveys, is consistent with the idea that the labor market is actually weakening (although it may also be that people are disappointed about the results compared to what has been previously promised).

Personal Income was also a smidge weak, although Consumption held up (God Bless America!). More importantly, while the year-on-year Core PCE deflator was as-expected at +1.9%, it was a soft +1.9% with the monthly change coming in flat. The deflator was 2% last month, which is the Fed's putative target. One month is not a trend - as we have seen, since Core CPI re-accelerated to new highs after its dip - but if the Fed wants cover for a decision to increase monetary accommodation, they have a tiny bit of cover now.

The ISM Manufacturing survey was somewhat weaker-than-expected, but it remains above 50 (53.5). Meanwhile, Manufacturing PMIs in Europe have been consistently weaker and today's releases put Spain at 42, Greece at 43.1, Italy at 44.8, France at 44.7, and Germany at 45.2.

Maybe the Mayans knew what they were doing when they said 2012 would be the end of the world? Just kidding, I think. Anyway, things would have to get substantially worse even to be the worst recession of the last five years, so let's look on the bright side!

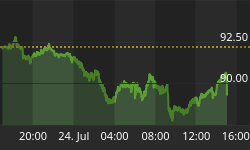

Stock markets were crushed on the uniformly bad news. Major European stock markets fell between 1% and 3.5% across the board. The S&P dropped 2% and couldn't even manage a respectable dead-cat bounce - rather then continued a slow-motion slide for most of the day. Commodities also took a beating, although less than stocks; in fact, if you avoided the Energy complex (which fell 3.1%) you would have been nearly unchanged in commodity indices. Precious metals gained 3.5% with gold itself up $61. Of course bonds did well. Ten-year real yields fell to -0.62%, and 30-year real yields to 0.35%. Ten-year nominal Treasury yields dropped to 1.46%. As the picture below shows, this is so far outside of the thirty-year downtrend (note the logarithmic scale) that there's nothing to compare the levels to.

The outlook is dim, but the sky isn't exactly falling yet, in the U.S. anyway. Stocks are only 10% off the highs, after all, although why they were ever at those highs I haven't figured out. They're still up on the year. There is some chance, though, that enough of these bad eddies - European growth, Greek election, Spanish/Bankia crisis, and so on - come together to cause some real rough seas over the next couple of weeks.

But we always have the central bankers! Talk of how this makes QE3 more likely may have been the only reason stocks didn't end up down 4% rather than -2.5% today. Recent pronouncements, however, such as by NY Fed President Dudley on Wednesday, have tended to be fairly discouraging about QE3. The question which is being continuously raised is: why bother with QE3 if interest rates are already at record lows for the whole yield curve?

There's some merit in this question, but let me start by pointing out that before the Fed eased in October 2008, 10-year rates were already around 3.50%, and hadn't been below 3% since the 1950s. So the argument that low rates obviate the need for easing clearly didn't stop the Fed in 2008 and I can't think of why it would stop them now. There's always room to have them lower.

Let's consider the question more formally, though. The Fed believes that monetary policy affects the economy in three ways: through the portfolio balance channel, by signaling, and by improving market functioning. The "portfolio balance channel" is just a cute way of saying that if the Fed buys all of the Treasuries, you'll have to buy something else. And when you buy corporate bonds or equities, for example, you provide cheap capital to business which then hires and the economy expands. Yes, I can hear you say "this sounds to me like getting the rubes to pour money into risky assets at bad prices." Precisely. But the Fed sees this as supporting business, and you can see what a wonderful expansion this has produced! Importantly, it isn't just the level of rates that matters, but the level of rates relative to other assets. So if stock prices fall, then merely maintaining rates where they are should be supportive of a return to the previous-bubbly levels.

The signaling channel is just what it sounds like. The Fed believes that we feel better when they're assuring everyone that rates will remain low through 2014 (even though they spent months trying to convince us that they didn't really mean it), and that businesses will invest more confidently knowing money will be cheap for a while. I doubt this has very much importance since the Fed is not held in the esteem it once was, and because businesses and individuals who are concerned about rising rates in the future have the option to lock in rates today with longer-term loans or derivative structures. But again, the important point is that they believe it.

Finally, there is no question that adding lots of liquidity does help "market functioning." If markets shut down, the economy will tumble. The Fed definitely needs to focus on keeping markets running smoothly. It isn't clear how much they need to increase the amount of money in the system for that purpose as opposed to directly supporting financial institutions, but this is certainly a valid reason to have easy money.

There is a fourth reason that isn't usually included in the list, and that's the fact that increasing monetary liquidity pushes prices higher, and in some cases (such as when a collapsing housing bubble threatens banks as borrowers walk away from loans) it may be perfectly reasonable policy to try and push prices higher. This is the main reason the earlier QE was defensible - because core inflation was low and sagging. It doesn't really apply in the U.S. at this time.

The biggest hurdle for more QE at this point is that the earlier QE evidently didn't work very well. Obviously, the world economy is still in a real mess, although there's no question QE succeeded in raising the price level. So either QE is fairly ineffectual when it comes to raising output permanently - in which case they definitely shouldn't do more of it but moreover should reverse whatever they've done - or it works, but they just haven't done enough of it yet. Regular readers of this space know that I adhere to the old theory that monetary policy affects prices but only affects growth in the presence of money illusion, which probably is not operative in a world where everyone thinks inflation is higher than it actually is.

That is, I don't think the Fed can do anything about the economy except raise prices, or try to rein in inflation. They ought to work to keep the financial system itself working, keep banks trading with each other (but not to make trading profits, nooooooo, just to help fill customer orders), and unwinding in an orderly way the institutions that cannot survive. But I wouldn't be voting to ease here.

But what are they going to do? Will central bankers sit by as markets and economies tumble and do nothing, simply because there's nothing they can do that would help? One thing I believe you can be certain of is that the Fed, the ECB, the BOE, the BOJ, and other central banks are not about to call themselves ineffectual. That means they will try to "do something" at some point, and they really only have one tool: the money supply. Whether it's through LSAP, or announcing a target 10-year rate, or eliminating the Interest on Excess Reserves, the process they use operates through the medium of the money supply. I strongly suspect that if markets continue to weaken and/or the Eurozone is sundered, the Fed and other central banks will wade back into the fray.

After all, how badly can they screw up? The Mayans say we only have six months anyway.