Below are extracts from recent commentaries posted at www.speculative-investor.com.

Outlook

Our view over the past few months has been that commodities, as represented by the CRB Index, would remain reasonably firm into the second quarter of this year with any weakness in metals and energies being offset by a resurgence in the grains and other food commodities. At this stage the metals and energies are mostly stable near their highs and the agricultural commodities are coming to life (refer to the below chart of the Agricultural Commodities Index for details), so things are panning out roughly as expected.

Actually, the industrial metals have been a bit stronger than anticipated, not only in US$ terms but relative to gold. The below chart of the gold/GYX ratio (the gold price divided by the Industrial Metals Index), for instance, shows that gold is currently near its lows of the past two years relative to the industrial metals. Taking a 2-year view we remain very bullish on gold relative to metals such as copper, nickel, lead, zinc, aluminium and tin, but as outlined in previous commentaries we doubt that gold will start to demonstrate much relative strength until the second half of this year. The reason is that economic growth is likely to remain reasonably firm during the first half of 2005, thus supporting the cyclical metals relative to counter-cyclical gold.

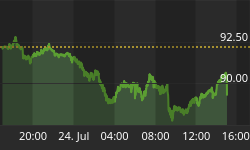

In US$ terms, early this year it looked like major peaks were in the process of being put in place in several of the industrial metals. However, it now looks like we could get a final surge to new highs in metal prices over the coming weeks. Copper, for example, has been consolidating in the $1.40-$1.50 range in a way that points towards a move up to the 1.60s (a weekly chart of copper futures is included below).

In our opinion, what is presently underway is a final blow-off to the upside in the prices of some commodities and many commodity-related equities. It's impossible for us to confidently predict how much further these moves will go before the inevitable downturn gets underway, although our guess is that major peaks will be in place before the end of March. What we can say with confidence is that the decline that follows the speculative blow-off will take back all gains achieved during the blow-off stage plus a lot more. For an indication of what is likely to happen in some other sectors following the current blow-off take a look at what happened to silver and silver shares during March-May of 2004.

Gold: A leading indicator

More often than not, important turning points in the gold price occur in advance of important turning points in the CRB Index. However, there is no typical lead time -- the lead time can be from a few weeks up to 12 months or even longer -- so the relationship is difficult to apply in practice. Just taking into account the past 18 months, though, we can ascertain from the below chart comparison that gold has been leading the CRB Index by about 3 months. Therefore, IF a major peak(*) was put in place in the gold market in December (we think it was) and the relationship of the past 18 months continues to hold then a major peak in the CRB Index is likely to occur this month.

Much of our work suggests that the CRB Index is very close to its peak for the year, although with agricultural commodities appearing to be in the EARLY stages of an advance there probably won't be substantial weakness in the index until the second half of this year.

*Unless we specifically state otherwise, when we use the term "major peak" we mean a peak that will hold for more than 12 months. Therefore, when we talk about commodities being close to a major peak we are not implying that the long-term bull market in commodities is about to end. We expect that MUCH higher prices for commodities will be seen later this decade.