After weathering a long consolidation followed by a major correction, gold stocks remain deeply out of favor today. But this bearish sentiment is slowly yielding as gold powers higher in its usual autumn rally. Gold stocks are starting to show signs of life again. And after their strong advance since late July, they are now on the verge of a major upside breakout. Odds are this event will herald a major new upleg.

Despite the gold-stock sector commanding some of the biggest gains of the past decade, gold stocks have become a four-letter word. The flagship gold-stock index, the HUI, essentially stalled out way back in late 2010. Then it more or less ground sideways for an entire year despite gold continuing to surge. While the HUI did achieve a marginal new record high last September, it corrected sharply in early 2012.

Over an 8-month span ending in mid-May, the HUI plunged a gut-wrenching 40.8% in a massive correction. The tail end of this selling was so extreme that it mushroomed into a full-blown capitulation, a panic-like selling climax. Gold stocks had become the pariah of the stock-market world, ignored or scorned by virtually everyone. And much of that hyper-bearish sentiment lingered through the summer.

That brutal capitulation, like all extreme selling events, was purely emotional. Irrational fear snowballed into a short-lived bubble, which soon popped so the HUI bottomed. But traders, as usual, chose to rationalize that selloff and attempt to justify it in fundamental terms. So a belief was born that gold stocks as a group were no longer able to profitably mine gold, that their costs were rising too fast to surmount.

But this notion was a total falsehood, absolutely untrue. To combat it I advanced our gold-stock-valuations thread of research in June. I looked at the individual price-to-earnings ratios and dividend yields of every HUI component stock, and aggregated them into market-capitalization-weighted HUI valuation metrics. These reflected gold-stock valuations as a whole, and in reality they were incredibly low.

The gold stocks had never been cheaper throughout their entire secular bull in conventional valuation terms than they were during that irrational May capitulation! The HUI's P/E ratio was running at 12x earnings at the end of May, lower than it had been during the stock panic and even way lower than the broad S&P 500 index's P/E. Gold stocks were incredibly profitable, so much so that they were value plays.

Nevertheless, the false belief that gold miners' costs were spiraling out of control persisted throughout the summer. Since doing original research is so challenging and tedious, and being a contrarian and being brave when others are afraid is so darned hard psychologically, the great majority of traders took the easy route. They swallowed the fundamental rationalization of an emotional selloff, blinding themselves.

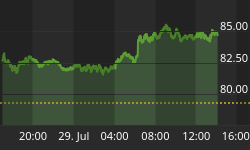

This fabricated notion, which I still hear on CNBC even this week, capped the HUI's post-capitulation bounce near 460 all summer. But over the last couple weeks the HUI has started to seriously challenge this multi-month resistance. As I pen this essay, this headline gold-stock index is probing above 460 in breakout territory. This gold-stock breakout will really help accelerate the sentiment shift back to bullish.

This first chart helps illustrate why, setting the scene for the HUI's imminent breakout. It shows the HUI superimposed over the gold price, the primary driver of gold miners' profits and hence ultimately their stock prices. Gold has already broken out above its own summer resistance in recent weeks, and is accelerating higher. Once the HUI follows it and breaks decisively above 460, everything changes.

You can see the HUI's 460 resistance that has capped it since May's capitulation on the right side of this chart. While the gold stocks as a sector haven't been able to carve new highs since then, there have been higher lows. This creates a bullish technical formation known as an ascending triangle, rising support and flat resistance. The same phenomenon recently led gold to shatter its own $1625 resistance.

And the sheer potential of the gold stocks after this imminent breakout is breathtaking. Gold stocks mine gold of course, so its price determines their long-term profitability. And universally in the stock markets, profitability determines any stock's long-term price level. This past spring's gold-stock capitulation ignited a big divergence between gold stocks and gold, the miners' stock prices aren't reflecting their profitability.

Since April, the HUI has largely languished in a band between 400 and 450. It is shaded a darker blue in this chart. Note that during this latest episode, gold was trading around $1600. Is that situation rational fundamentally, have this year's summer-doldrums gold-stock prices reasonably reflected prevailing gold levels? Not a chance. This is readily apparent when considering past 400-to-450 HUI consolidations.

The previous one before this summer's ran from late 2009 to mid-2010. Where was gold trading then? Around $1100. So despite this summer's baseline gold price being about 45% higher, the HUI was trading at the same levels as several years ago. This makes no sense at all, it is irrational and illogical. The incredibly low valuations of gold stocks prove this past summer's levels were fear-driven, not fundamentally justified.

Another episode of the HUI consolidating between 400 and 450 happened in early 2008 before that year's epic once-in-a-century stock panic. Where were prevailing gold prices then? Around $900. This past summer's $1600 gold was 78% higher than the spring of 2008's, yet the gold stocks as measured by their flagship index are trading at the same levels! This fundamental anomaly can't persist for long.

And that is why the imminent gold-stock breakout is so exciting and hyper-bullish. Since May's capitulation, investors and speculators have simply been blinded by fear whenever they looked upon this sector. But a major breakout, as we've seen in gold in recent weeks, works wonders in rapidly bleeding off bearish sentiment. So once the HUI shoots decisively above 460, the scales will fall from traders' eyes.

As they take a fresh look at gold stocks, they are going to be flabbergasted at the vast fundamental disconnect. They will start to realize that having the gold stocks trading as if gold was at $900 or $1100 when it is really around $1700 is a monumental bargain. And capital will start flooding in to ride the gold-stock mean reversion back up to more reasonable levels relative to gold. Hedge funds will lead the way.

During this past summer when gold stocks were as deeply out of favor as they've been since the stock panic, elite hedge-fund managers started nibbling as they examined this sector's core fundamentals. Their gold-stock holdings continued to grow as the HUI recovered in August. And other hedge-fund managers, eyeing those big profits in a year where finding performance is challenging, are salivating.

Since they are seeing their contrarian peers making money in gold stocks, and they are already interested, it won't take much to push them into buying mode. So a major upside breakout will almost certainly prove more than sufficient. Nothing attracts capital like upside momentum, and the HUI's should accelerate considerably once it breaks out. And interestingly, the summer's 460 resistance may not even be the biggest breakout.

Really big moves in gold stocks, both uplegs and corrections, nearly always persist for more than a few months. So the summer resistance may be considered too short-term by some to get excited about breaking out of. But look carefully at the chart above, and you'll see the HUI's black 200-day moving average is just a little higher. This critical metric is currently around 470, merely a single good up day's rally higher from here.

When a sector in a secular bull with amazing fundamentals crosses back over its falling 200dma after a major correction, it is supremely bullish. The last similar event occurred way back in early 2009, during the stock-panic recovery. Once the consolidating HUI broke decisively above its falling 200dma, it surged from around 300 to 600 in the subsequent couple years. Gold stocks doubled after that similar breakout!

Could they again? Could the HUI's next major upleg ultimately carry it from around the recent 450 levels to over 900? Absolutely, it isn't even a stretch. And the reason is because gold stocks remain so anomalously cheap relative to prevailing gold prices. This is easiest to understand when viewed through the lens of the venerable HUI/Gold Ratio, the HUI close divided by the gold close charted over time.

I've done a lot of HGR work over the years, which has led to massive realized gains in gold stocks for us and our subscribers. Prior to the stock panic, for 5 years running the average HGR ran 0.511x. The HUI tended to trade at about half the prevailing gold price. The stock panic torpedoed this longstanding secular relationship, generating such extreme fear that many gold-stock traders fled and never came back.

If you want to get up to speed on the HGR, read my latest round of research on it published in mid-June. This next chart builds on that, comparing the HGR (blue), the HUI (red), and a hypothetical HUI that shows where this index would be trading if it regained its pre-panic average HGR of 0.511x (yellow). When gold stocks are considered relative to their fundamental driver, their upside potential is incredible.

You surely remember 2008's brutal stock panic, no one who lived through it will ever forget it. That once-in-a-lifetime fear superstorm blasted that emotion to heights previously unimaginable. And unfortunately even though gold weathered that panic better than almost everything else, gold-stock investors and speculators wilted in the withering onslaught of extreme fear. They dumped gold stocks like the Apocalypse was nigh.

As you can see, this pummeled the HGR down to silly levels well under half its historical average. But as I told our subscribers at the time, this was an emotional anomaly. Gold stocks were radically undervalued fundamentally, so once the fear storm inevitably passed they'd have to soar back up to reflect reasonable levels relative to gold. And indeed they did, the HGR more than doubling by only a year after the panic.

Since the 5-year pre-panic average HGR is 0.511x, let's call half that panic levels. Only the greatest of fear, the most extreme bearishness, can force the HUI under 0.25x the price of gold. Like a beachball held underwater, the moment that emotional pressure abated the gold stocks rocketed higher relative to gold out of the stock panic. Amazingly, these panic-level HGRs were seen twice again this past summer!

In both mid-May and late July the HGR again knifed under 0.25x! This is just staggering, it defies belief. While there was certainly good reason to be scared senseless during 2008's epic stock panic, what was so darned scary to gold-stock investors and speculators this past summer? Is $1600 gold, which was never even seen before July 2011, such a bad thing for gold miners? They print money hand over fist at these prices!

There was no fundamental justification for sub-0.25x HGRs back in late 2008 and there was even less so this summer, when the gold stocks' collective P/E ratio was almost 25% lower! For whatever reasons, the traders who own gold stocks got trapped in some hyper-bearish spell last spring. Their fear led them to sell so aggressively that they irrationally hammered these stocks back down to panic levels relative to gold.

But their loss is our gain, if the weak hands who drove the capitulation can't think rationally then they deserve to lose money. The stock markets gut people who choose to be swept away in popular greed or fear. Such extreme gold-stock levels couldn't persist after the panic and they can't persist now. And all it will take to ignite a fast recovery rally is the beginning of a sentiment shift from bearish to bullish.

And the imminent gold-stock breakout, either above summer resistance or the HUI's 200dma, ought to be more than ample. After that, the potential upside in the beaten-down unloved gold stocks is gigantic. Note above on this chart the massive gap between where the actual HUI is trading and where this index would be if it merely returned to its pre-panic average HGR of 0.511x. We are talking a HUI above 850!

And that is at today's gold prices. Gold is already climbing higher in its major seasonal rally that accelerates almost every autumn. On average since its secular bull was born in early 2001, gold powers 19% higher between late July and late May. This year gold was trading around $1577 at worst in late July. From that base, a merely average seasonal rally between now and May would carry gold to $1875.

At $1875 and a 0.511x HGR, the HUI would be over 950! This is more than double today's levels in a relatively short time frame, well under a year. Will it happen? No one but God knows the future. Could it happen? Absolutely. It is not much of a stretch at all to merely expect an average seasonal gold rally given global central banks' fast money-supply expansion, and gold stocks will inevitably once again reflect prevailing gold prices sooner or later.

Now you certainly don't need to agree with these assumptions to buy the dirt-cheap gold stocks today. Let's be super-conservative instead. Assume gold has a tough busy season and only rallies 10% between late July and May. And let's assume the HGR merely gets back up between 0.35x to 0.40x, where it spent the majority of its time in this post-panic era. This still yields a HUI target between 605 and 695, way higher from here.

But realize there is a decent chance for a large upside surprise too. We haven't seen any euphoria in gold stocks since way back in early 2006, a long time ago. When that happens, traders briefly drive them up to expensive levels relative to gold before the greed bubble bursts. And the one thing that can ignite euphoria is a massive and relatively rapid upleg. And this is certainly likely given how irrationally undervalued gold stocks are today.

Back in early 2006, gold stocks actually getting popular temporarily catapulted the HGR near 0.61x. So the pre-panic average of 0.511x is certainly no hard ceiling. As we saw in silver back in early 2011, once investors and speculators start actually getting excited about something in precious-metals land they can quickly drive it far above historical relationships with gold. The sky is the limit if greed gets excessive.

At Zeal we are skeptical contrarians. We relentlessly study the markets to uncover what is really going on, and then we fight the crowd to buy low when others are afraid and later sell high when others are brave. So this summer as that silly and easily-disproven fallacy about gold miners' costs being out of control spread, we were buying cheap. This week the gold and silver stocks on our books bought since the capitulation already have unrealized gains running as high as 60%!

And with the HUI still so low relative to gold, this young gold-stock upleg is likely just getting underway. If you have the contrarian chops to ride it before all the easy gains are won, join us. We publish acclaimed weekly and monthly subscription newsletters loved by speculators and investors worldwide. They dig into the markets to help you understand what is going on, why, and what opportunities it is creating. Our contrarian approach has proven wildly profitable, with all 628 stock trades recommended to our subscribers since 2001 achieving stellar average annualized realized gains of +35.5%! Subscribe today.

The bottom line is gold stocks are on the verge of a major upside breakout. Once the HUI gold-stock index climbs decisively above its summer resistance and 200-day moving average, the shift in sentiment from bearish to bullish should accelerate dramatically. As traders start understanding just how cheap gold stocks are fundamentally, capital should flood in and feed on itself to drive a major new upleg.

And with gold stocks recently back down at panic levels relative to gold, the upside is incredible. The major gold stocks would have to nearly double just to trade at reasonable levels relative to today's gold price. But gold is likely to continue powering higher in its usual strong season, pushing the bar even higher. And smaller elite gold and silver miners should really leverage the headline HUI's gains.