The stock market gained 2% today, and commodities jumped 1.25% led by energy, metals, and softs. There was no news that could have rationally justified such a move, and volumes were as light as they have been in two weeks. Some commentators, grasping for straws, suggested that the decent NAHB Housing Market Index number (up to 46 versus 41 expected, to the highest level since 2006) and modestly stronger-than-expected Existing Home Sales figure (4.79mm versus expectations for 4.74mm) triggered the rally, but that ignores the fact that most of the equity move was completed prior to the 10:00ET release of these figures.

Others resolved the conundrum by saying that "apparent progress on the fiscal cliff" led to the rally, but the only progress made was that neither side was hurling epithets at the other in public. There is no sign of any agreement being made, and certainly no chance of any agreement being made that would persuade investors with big gains to avoid realizing taxes this year (since it is exceedingly unlikely that the upper end of the tax structure will be unchanged or lower next year). Now, I'd suggested last week that "this is mostly a cycling of positions, a re-setting of tax basis at a higher level, and shouldn't amount to a major selloff by itself," but there are other reasons to be less-than-exuberant about the market's immediate prospects too.

One of these is the conflict in and around Israel and the territories under her control. While there is loose talk about a 'cease-fire,' Israel is demanding a long-term agreement to stop the rocket fire and Hamas is saying "Israel started it." I think it says something about our political discourse here that it is probably easier to resolve the Israeli-Gaza-Syria-Egypt-Iran conflict than to resolve the Fiscal Cliff discussions, but also keep in mind that Israel still wants to do something about Iran's nuclear capabilities, so a cease-fire strangely may not be in her interest at the moment.

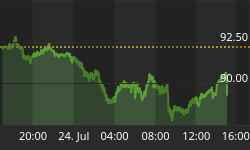

There is no doubt that our domestic housing market is getting better, to be sure. I've pointed out periodically (see here, here, and here for example ) that home prices are rising again and not surprisingly that is making home builders happy again. The chart below (source: Bloomberg) shows the NAHB index I alluded to earlier.

It looks suspiciously like the chart of home builder Toll Brothers (TOL) shown below (source Bloomberg), suggesting that there is not a lot of true analysis going on among the buyers of that stock. Toll Brothers has a current P/E of 61 on trailing earnings, and 50 on estimated forward earnings. I don't have a position in TOL, nor do I plan to; I just point this out in case your child was thinking of becoming an equity analyst. Help him or her along a different path.

Part of the reason for today's surprise in home builder sentiment might be the sudden promise of new home building activity along parts of the eastern sea board, courtesy of Sandy, but the trend has been well established for a while. While there is ample inventory of existing homes (though these are being drawn down as well, slowly), the inventory of new homes has been at a 50+ year low for more than a year (see chart, source Bloomberg) and it was just a matter of time before more were built. An existing home is a good, but imperfect, substitute for a new home.

Now, as an inflation guy the reason I care is because the decline in home inventory, coupled with virtually free money for builders and home buyers who can qualify, is pushing up the cost of a big chunk of the consumption basket. Owner's Equivalent Rent (which is 60% of housing, which in turn is 40% of CPI) has been rising at slightly faster than that of core inflation. As the chart below shows, there is a distinct relationship between prices in the market for existing homes and the general increase in rents (both direct and imputed) 15 months later.

It's not a new story, but rather one I've been talking about for some time, and remains a key reason I remain bullish on inflation despite global central bank protestations (and asset manager convictions, as far as I can tell) that deflation is a more proximate threat.

Meanwhile, other economists have concluded that the reason inflation has been rising rather than falling despite huge amounts of slack globally must be that ... their Phillips curve needs recalibration. In a recent funny note by Goldman's economics group - though it was not meant to be funny - entitled "A Flatter and More Anchored Phillips Curve," they said

"We have long argued that labor market slack would weigh heavily on inflation in the aftermath of the Great Recession. This view has generally worked well as core (ex food and energy) inflation has fallen substantially since 2007. But the decline in core inflation abated in late 2010 and -- despite recent signs of renewed disinflation -- core inflation has generally been stickier than the large amount of slack would have suggested.

"A candidate explanation is that the inflation process (or "Phillips curve") has changed in recent years. Economists have argued for some time that improved central bank credibility, globalization and downward rigidity of nominal wages have altered inflation dynamics since the inflationary 1980s.

Considering that the Great Recession didn't really kick in until late 2008, and core inflation (ex-shelter, which was suffering from the implosion of a giant bubble) rose from 2007 until late 2009, another 'candidate explanation' would be that their model was not mis-calibrated but rather completely mis-specified. The Phillips Curve, which relates wages, not core inflation, to slack in the labor market, is not useful in forecasting inflation. This is well known, and yet expensive economists have worked incredibly hard to resurrect the theory. (Here's a fuller illustration/explanation of why the Phillips Curve as typically used is wrong).

But beyond that - if you need to keep changing the calibration of your model to fit the facts, then it's not a good model. That's sort of Modeling 101. The economists explain/plead further:

Economic principles suggest that core inflation is driven by two main factors. First, actual inflation depends on inflation expectations, which might have both a forward-looking and a backward-looking component. Second, inflation depends on the extent of slack (or spare capacity) in the economy. This is most intuitive in the labor market: high unemployment means that many workers are looking for jobs, which in turn tends to weigh on wages and prices. This relationship between inflation, expectations of inflation and slack is called the "Phillips curve."

Well, no. Economic principles suggest that inflation is mainly driven by money and the velocity of money. Some discredited principles suggest what they say, but it's not working. Their own chart, showing they're off by some 100%, is reproduced below.

On to happier items. In case anyone still thought France was a AAA nation, Moody's announced their opinion this afternoon that it is not, in downgrading the nation from Aaa to Aa1. Moreover, France remains on watch negative, due to structural challenges and a "sustained loss of competitiveness" in the country. I guess on second thought, that's not so happy. How did France lose competitiveness? Do you think it has anything to do with the incredibly expensive social contracts and the short working week and year? But no, perhaps they didn't spend enough on education and national health care.