Holy cow, not even the most vociferous gold bears saw that one coming! Gold just suffered what can only be described as a panic. This metal plummeted so fast that its price surrendered a staggering 1/7th of its value in just two trading days! This blistering decline was so extreme it even dragged the general stock markets down with it. Shell-shocked gold investors are nervously wondering what to make of it.

The gold panic certainly caught me unaware, even after a dozen years of relentless study and very profitable trading of this secular gold bull. We were and are heavily deployed in dirt-cheap gold stocks in light of gold's incredibly bullish technicals and sentiment. Seeing one of gold's fastest selloffs ever wasn't even in the probability space, it should have been effectively impossible. Yet it still happened.

That's the problem with panics, they are so extraordinarily rare that they can't be predicted. 2008's crazy stock panic was the first true panic in 101 years, since 1907. The last stock selloff that even approached panic-magnitude before that happened in late 1974. So these events are separated by several decades to a century, making them impossible to game. Not one in a hundred selloffs cascades into a panic.

Gold's recent plunge was crash-like as well, but couldn't have been a crash. While panics cascade from lows after long declines, crashes erupt from record highs after long rallies. Crashes, which are also ultra-rare, are only seen immediately after major multi-year bull runs where euphoria just drove a parabolic terminal ascent. That certainly doesn't describe gold's weak downward price action over the past 6 months or so.

Gold was already low and unloved leading into its incredibly improbable panic. On last Thursday's close before the mayhem started, gold was already down 12.9% since its recent early-October interim high and 17.6% under its August 2011 bull high. This was very reminiscent of 2008's stock markets where the SPX was already down 22.5% over nearly a year just before it would plummet 30.0% in a single month.

Panics are ultra-extreme sentiment events that cascade out of lows when bearishness is already high. They are epic superstorms of fear that roar in and suddenly grip traders' hearts, driving outsized selling so crazy that it would be utterly impossible any other time. Gold plunged 4.7% last Friday, and another 9.6% on Monday! The kind of universal fear and selling pressure necessary to trigger that is staggering.

I've never seen anything like this gold panic, no one has. Our gold-price data goes back to 1969, an exceedingly-long 44-year span. Americans couldn't even legally own gold bullion before late 1974 thanks to another tyrannical Democratic President! There have only been two other comparable selloffs in nearly a half century, in January 1980 after the last secular bull's parabolic climax and February 1983.

That January 1980 event was actually a crash marking the end of the mighty secular gold bull of the 1970s. Gold plummeted 13.2% the day after its peak and 18.2% in the two days after. Realize gold was in a popular speculative mania then, drenched in euphoria. It had skyrocketed an astonishing 200.4% higher in just over 5 months, a far cry from its 12.9% decline in the 6 months leading into this panic.

Now that, a tripling in 5 months, is what a bubble looks like friends! I can't believe the number of knuckleheads I've seen on CNBC this week who claimed gold was recently in a bubble so its massive selloff was justified. They obviously know nothing about gold and nothing about speculative manias, which strips all credibility from their weathervaney hyper-bearish outlook. Gold was weak pre-panic!

Naturally the sharpest gold selloff of our lifetimes after the post-bubble crash in January 1980 is going to wreak catastrophic technical damage. There's no way a 13.8% two-day plummet isn't going to leave a mark, no matter which gold chart you are looking at. A fear and selling anomaly that extreme is going to leave all gold's technicals hopelessly broken. A panic's technical carnage is complete, utter devastation.

Panics are extreme herd behavior, nearly everyone succumbing to fear at once and frantically galloping for the hills. So I don't even know if they are explainable, since the herd ignores innumerable sparks for decades on end until one inexplicably ignites a stampede for the exits. Nevertheless, we have to try and understand this gold panic and its implications. And like everything in the markets, that requires context.

The lead in to the gold panic starts way back in the summer of 2011. Fears of Washington actually defaulting on US Treasuries in the last debt-ceiling fight spawned a rare summer surge in gold. Flight capital poured into this metal so it simply shot up too far too fast, becoming very overbought. Right at the peak I warned that a sharp gold correction was imminent, as excessive popular greed is never sustainable.

Before we move on, that August 2011 bull high itself is incredibly important today. The gold bears are out in force making the case that gold's secular bull is over. If they are right, its end had to be that August 2011 high. But as I explained last year, that looked nothing like a gold bull climax. There was no popular mania, gold was just overbought. And if that wasn't a bull-slaying climax, gold is not in a secular bear today.

Leading into gold's last secular-bull climax in January 1980, a whopping 3/4ths of gold's total gains since its last major interim low a few years earlier happened in that run's final 5 months! It was a vertical parabolic blowoff driven by a popular speculative mania. But the run up to the August 2011 high only saw 1/3rd of gold's total gains in its major multi-year rally accrue in the final 5 months. It wasn't a parabolic climax!

So gold wasn't and isn't in a new secular bear, but it did need to correct after that summer 2011 surge like all bull markets. And correct it did. It fell sharply in a massive initial correction, bounced, and then fell sharply again heading into late 2011. That weak price action would establish a major multi-year support line that was likely the primary contributing factor to the recent gold panic. $1550 would hold for years.

If gold's bull had really died in August 2011, the gold price would have kept on relentlessly falling rather than consolidating high. That consolidation between $1550 support and $1775 resistance ultimately helped form the huge descending-triangle technical formation highlighted in yellow. An upside breakout from such a large and long-lived triangle would be a very bullish omen for any market, as it was for gold.

Gold broke out decisively to the upside late last summer. Futures speculators, who are always wrong at price extremes as a group, were hyper-bearish which is a major buy signal. So gold surged impressively last August and September even though it was loathed by mainstream analysts and investors. But that run also proved too far too fast, gold took a breather to consolidate a bit at that $1775 resistance line.

This metal soon started climbing again in early November, but then a second major contributing factor to the panic started to emerge. The general stock markets bottomed then and started to rally, despite all the intense political and taxation uncertainty. As this stock rally grew and grew, first achieving new cyclical-bull highs and then nominal record highs, demand for alternative investments like gold simply shriveled.

Gold's weakness over the 5 months or so since is a direct result of the increasing euphoria and high complacency the levitating stock markets generated. Gold started exhibiting a high negative correlation to the flagship S&P 500 stock index, on timeframes running from intraday to monthly. Mainstream money managers were selling their small gold allocations low in order to buy stocks high, so gold suffered.

This increasingly-poor gold sentiment as capital rotated out of the metal to chase melting-up general stock markets triggered serious differential selling pressure in the leading gold ETF, GLD. Stock investors were selling GLD shares much faster than gold was being sold, spawning the biggest correction in GLD's physical-gold-bullion holdings since the stock panic. This GLD selling further weighed on the gold price.

While this weak gold action thanks to the lofty stock markets sucking away interest and capital from alternative investments was very frustrating for contrarians like me, gold was still holding its own. Several times since February's capitulation (which are normally selling climaxes marking major lows), gold bounced near its major $1550 support. This resilience was despite the stock market edging ever higher.

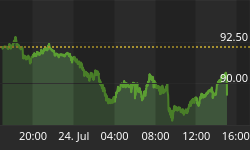

And last Thursday afternoon at $1561, gold was again just above $1550. Since $1550 had held rock-solid through a major correction and high consolidation for the better part of two years, many gold futures speculators had stop losses placed just under it. You generally allow a 1% overshoot on major support and resistance lines to make sure any breakout is real, so a big mass of stops was set around $1535 or so.

All last week, gold was under pressure because of fears the Central Bank of Cyprus would be forced to dump that country's official gold holdings into the marketplace. If you have any experience in the gold market, you know that central-bank selling is its ultimate bugbear. With sentiment already weak thanks to the anti-alternative-investment fallout from the stock-market melt-up, these fears really took root.

This Cyprus gold-sale talk left me pulling out my hair in frustration. Why? Cyprus's official gold holdings are trivial, just 13.9 metric tons! They rank 55th out of the world's countries, and the gold market could have easily absorbed them in a single day. In fact, on three separate trading days since mid-February the leading GLD ETF alone had been forced to liquidate 20.8t, 13.5t, and 16.8t. Cyprus's gold is nothing.

Another contributing factor psychologically earlier that week was major investment banks predicting gold was heading much lower. This shouldn't have scared anyone either though, as Wall Street always makes the wrong calls at extremes. These same major banks were very bullish on gold in August 2011 as it peaked, calling for imminent surges well into the $2000s. And they were bearish on stocks in early 2009.

But with gold near $1550 support just above a minefield of stops, any selling at all could start an avalanche. And it did, even though the odds were wildly against it. Last Friday morning gold was at $1545 before the main US futures-trading session opened, and sold off sharply soon after. Once gold dropped 1% under that $1550 support, stops began to trigger. Selling begets selling, driving prices lower in a vicious circle.

And this gold selling was completely futures-based initially as the panic started cascading. Gold futures are a highly-leveraged vehicle. Though they've since been raised a little, that morning the maintenance margin on COMEX gold futures was just $5,400 per contract. That means futures traders could control 100 ounces of gold worth $156,100 for just 3.5% down. That is insanely-risky 29-to-1 leverage!

In the stock markets, the Federal Reserve has limited margin to 2 to 1 since 1974 (a brutal year that saw a near-panic). Yet even with 50% down, panics are still possible as we learned in 2008. Imagine the gold futures traders Friday morning taking 100% losses on a 3.5% gold swoon. If gold went down 7%, they would lose twice the capital they originally risked! Leverage is a dangerous, unforgiving game to play.

So early on Friday, the gold futures traders who wisely had stops since their leverage is so extreme got stopped out. Their automatic selling pushed gold prices lower. Then other futures traders who were paying attention sold too, before their 50% losses mushroomed to 100% or beyond. And margin calls were shooting out, futures trading houses demanding clients add more cash to cover their gold losses.

In ultra-rare extreme-selloff scenarios, the brokerages liquidate treacherous longs themselves. The markets are moving so fast that there isn't time to track down their clients and get money wired. So they dump futures contracts en masse themselves, traders aren't even given a chance to make a sell decision. These margin calls and forced liquidations are, without any doubt, what fueled that crazy gold panic.

Of course with gold plunging, stock traders soon joined the futures traders in fleeing in terror. They started selling GLD shares aggressively as Friday wore on, ultimately forcing this ETF's custodians to liquidate another 22.9t of its holdings (1.9%). But as I discussed last week in an essay written Thursday (before the panic), clusters of 1.0%+ down days in GLD holdings near gold lows are major bottoming indicators.

Friday gold plunged 4.7% by the time the US stock markets closed, a very large loss. But it still wasn't panic-grade yet. During this secular gold bull which was born in April 2001, gold had fallen by more than 4.5% on 9 previous trading days (out of 3029). And I remember every single one of them, they were miserable if we happened to be long then. Friday is the worst psychological time for an outsized selloff.

Near extreme lows sentiment is overwhelmingly bearish, with everyone falling all over themselves to rationalize why the already-battered price is doomed to head much lower still. The weekends also prevent traders, both American and foreign, from acting on their growing fears as they read all this weathervaney hyper-bearish commentary. They stew and fret all weekend, and return Monday ready to literally panic.

We've seen the dangers Mondays present many times in the stock markets. Remember Black Monday 1987? That dark day in October the S&P 500 plummeted 25.7% after a 5.4% loss the preceding Friday! In August 2011, that same index plunged 6.7% on another Monday after Standard & Poor's downgraded US Treasuries for the first time in history after the preceding Friday's close. Mondays are dangerous times when weekend fear is extreme.

So the forced gold selling continued Monday morning, first in Asia and Europe. Those markets were mostly closed on Friday when gold started plunging in the States, so foreign futures traders were suffering the same margin calls and forced liquidations the very next trading day. They continued in the US too, with gold plummeting an unbelievable 9.6%! That has only happened 2 other times since 1969, virtually never.

And it was mostly futures selling Monday, leveraged players getting eviscerated for their own greed and stupidity. Even though gold's down day was the largest since February 1983, 30 years ago, GLD only experienced enough differential selling pressure to force its holdings 0.4% lower (4.2t). The stock-trader selling was mostly out of the way Friday, when fully 5/6ths of it occurred as measured by GLD bullion liquidations.

The gold panic was a forced-selling phenomenon driven by a support break crushing over-leveraged futures players. Unfortunately their mistakes caused vast collateral damage among the rest of us. I've never seen my portfolio lose a sixth of its value over two trading days before, even during 2008's once-in-a-century stock panic. This gold panic is one of my worst experiences in decades of trading. It royally sucked.

But like anything in the markets, there is no sense getting emotional about it. What has come can't be changed, all that matters is the future. And it is critical to realize that all panics are emotional events, they have nothing to do with fundamentals. It is quite literally impossible for global supply and demand fundamentals in gold or anything to change fast enough to justify a 1/7th plunge in two trading days.

The bullish fundamentals for gold did not change one bit between Thursday afternoon and Monday afternoon, despite gold being 13.8% lower. The only thing that changed is sentiment. Traders got scared, the selling breached a major stops zone, which resulted in margin calls and forced liquidations, and the gold price is much lower as a result. But nothing fundamental changed in the gold market!

The central banks didn't suddenly dump their vast gold hoards, no one figured out how to economically precipitate gold out of seawater or use alchemy to transmute it in a laboratory, and no massive new gold mines suddenly came online. Whatever gold fundamentals existed last week are exactly the same now. Gold is a global and slow-moving industry, with supply and demand trends gradually evolving over many years.

If fundamentals haven't changed, then there is no reason for gold and gold-stock investors to join the hysteria and sell near major multi-year lows. Investing is about being brave when others are afraid, and in gold and especially gold stocks they are terrified right now. And thanks to the precedent of 2008's stock panic, which hammered gold, we know that the gold extremes just reached are actually very bullish.

This longer-term chart helps put gold's panic in better strategic context. Yes the panic shattered gold's multi-year high consolidation and pushed its total correction to 29.0% over 19.8 months. But interestingly we have seen worse within this secular bull! In just 7.9 months in 2008, gold plunged 29.3%. That stock panic drove the metal down over twice as fast in aggregate, although its climax wasn't quite as extreme.

Back in that stock panic, gold investors were also terrified. They believed the mainstream hype that gold was dead. After all, if gold couldn't act as a safe haven during a once-in-a-lifetime stock panic, why would anyone want to own it? They proclaimed the US dollar and US Treasuries were the new safe havens, that gold's secular bull had failed miserably. The universal gold hate in late 2008 dwarfed today's.

But all debating aside, gold had fallen too far too fast for its late-2008 prices to be sustainable. It was hyper-oversold, as measured by my highly-profitable Relative Gold trading indicator. In both October and November 2008, gold sunk down to 0.807x its own 200-day moving average. This was unprecedented within its secular bull, so all hope seemed lost. The technically-broken metal was down near $700.

But the bears were wrong, and the gold bulls like me were right and made fortunes buying in that stock panic. Gold would more than double after those extreme oversold stock-panic lows, powering 166.5% higher over the subsequent several years or so. When a price is at extreme lows, has fallen exceedingly far and fast, but its underlying supply and demand fundamentals remain bullish, it is the ideal time to buy.

This Monday, gold revisited those panic levels relative to its 200dma! It traded at 0.810x in rGold terms, almost exactly the same degree of oversoldness it bottomed at during 2008's stock panic. And after panics, even in the stock markets, prices always at least double over the subsequent two or three years regardless of whether a secular bull or bear is in force. Gold's panic likely guarantees a coming doubling!

As long as global gold demand growth continues to outpace supply growth, gold's secular bull remains alive and well. So a post-panic doubling to $2700 is merely par for the course. New gold mines take a decade to bring online, and the lack of investor enthusiasm for gold stocks during gold's high consolidation has decimated this industry anyway. There will be no big supply increases for years to come.

Meanwhile global investment demand is almost certain to recover and grow dramatically. Global central banks are drastically ramping their money supplies, leading to very overbought and toppy stock markets. Once these inevitably turn, demand for alternative investments will recover then soar. And investors are woefully underinvested in gold, it is still on the order of only 0.5% of Americans' total portfolios.

This gold panic is the ultimate test of our contrarian mettle as gold investors. Are we rational and tough enough to weather it, or will we panic and sell low? At Zeal our decades of study and trading have forged us into traders who simply don't feel fear. We are well aware of the risks, but like elite commandos going into combat our extensive training has eliminated fear. Fear is for the naive, not the battle-hardened.

The gold panic hammered gold down to panic-level oversoldness, but gold stocks actually to literal panic levels. The bargains among dirt-cheap hyper-oversold gold stocks are truly epic, the greatest of this entire secular bull by far after the stock panic. So if you want to buy low, check out our extensive research on our fundamental favorite gold and silver stocks. We sell popular and inexpensive reports detailing our extensive research into the world's best precious-metals miners and explorers. Buy yours today!

We've also long published acclaimed weekly and monthly subscription newsletters for speculators and investors. Our hardcore contrarian approach will give you invaluable knowledge and perspective that will help you learn how to buy low and sell high. It works, with the 637 stock trades recommended in our newsletters since 2001 averaging stellar annualized realized gains of +33.9%! Fear and greed can be overcome, we can help you do it. Subscribe today!

The bottom line is gold just experienced a totally anomalous panic. Gold's sentiment has been getting increasingly bearish as the levitating stock markets sucked all capital out of everything else. This slowly pushed gold down to major multi-year support. And then some selling on minor news triggered stops and fed on itself. This resulted in margin calls and forced liquidations among leveraged futures traders.

So gold plunged. But as always in panics, such extreme selling is unsustainable. It burns itself out very quickly, leaving nothing but bargain-hunting buyers. So prices recover rapidly after panics, and ultimately more than double over the subsequent few years on the outside. The traders tough enough to buy low, or hold low, when everyone else is terrified earn fortunes in these massive post-panic rallies.