Let's reset the state of things:

- The Federal Reserve, and other central banks, have added a tremendous amount of liquidity to global financial markets. Ironically, both central banks who want higher prices (the Bank of Japan) and central banks who do not (pretty much all the rest) are pursuing the same strategy, and both groups believe they are winning.

- Global growth recovered from the post-crisis lows, but several major economies may be returning to recession after an expansion whose duration has been somewhat typical of the post-war period (even if the amplitude has not been).

- Some central banks have gone so far as to essentially declare victory, and are considering what course to take to unwind the extraordinary liquidity.

What is really somewhat remarkable about the current circumstance is really the last point. What central banks have done to date is really the easy part: handing out presents to children at Christmas always brings hugs and cheers. The difficult part is going to those children after Christmas and telling them you need the presents back, because you bought them on credit and need to return them to the store since you can't pay for them.

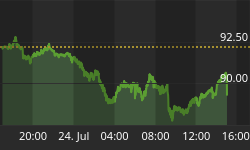

And the children in such a case can react poorly. That essentially happened this week when very mild comments from Ben Bernanke helped provoke a 7% one-day plunge in the Nikkei and considerable volatility in a number of other markets over the last couple days of this week.

But let's go one step further, because while the direction of the reaction to hints of an eventual change in Fed policy is not surprising the magnitude of that change may be. In other words, does anyone think that a 7% fall in a stock market, on the basis of vague statements about future monetary policy, is normal? Or does it look like the reaction of a frothy, overpumped market filled with participants who are there because...they feel there's nothing else available (and, anyway, one shouldn't "fight the Fed")?

(I am just asking, just as I am asking why my mother-in-law's broker virtually refused to let her sell stocks on Wednesday this week (before the breaks), urging her to "not give into fear." Fear, when the market is going up in a straight line? That's an odd thought. When brokers can't even conceive of why someone might want to not hold stocks, we are in a frightening state of mind.)

Incidentally, I didn't find the overall message on further asset purchases and timing of a future "taper" terribly unclear. William Dudley, president of the NY Fed and probably the second most-powerful voice at the Fed, said that the decision to taper will take three or four months. Moreover, the release this week of minutes from the most-recent FOMC meeting noted that "A couple of participants expressed the view that an additional monetary policy response might be warranted should inflation fall further." If Dudley is talking in terms of 3-4 months to even decide on a taper, and some meeting participants are still questioning whether more asset purchases could be warranted, there's simply no reason to be concerned about a change in policy for quite a while.

(Incidentally, I also found another snippet from the minutes interesting. Low and stable inflation used to be considered a good thing, but not necessarily any more: "It was also pointed out that, even absent further disinflation, continued low inflation might pose a threat to the economic recovery by, for example, raising debt burdens." It is not at all clear to me that a taper will even be announced in 2013, much less effected.)

In any case, if a simple lack of clarity on asset purchases causes a massive selloff in Tokyo and jittery markets worldwide, then it really is time to stop the asset purchases because it will get harder and harder to take those presents away.

Now, the sad part of all this is that the Fed's unwind plan simply isn't going to work to restrain inflation. According to that same story linked to above:

"That strategy calls for the Fed to allow assets to mature without being replaced. The central bank would then modify its guidance on how long it plans to keep the federal funds rate near zero and begin temporary operations to drain excess bank reserves. The Fed would next raise the federal funds rate, and finally, start selling securities."

Remember, draining excess reserves should have no effect at all on the supply of transactional money (e.g., M2). The Fed needs first to drain something like $1.6 trillion in excess reserves (I have kinda lost track) before their actions have an impact on a variable that matters. Simply wanting to restrain inflation isn't enough.

I do think that we are going to get higher interest rates; I just don't think those higher interest rates are going to impact the inflationary impulse now being charged in the system. However, as events this week showed, they very likely are going to impact market prices, and perhaps severely.

You can follow me @inflation_guy!

Enduring Investments is a registered investment adviser that specializes in solving inflation-related problems. Fill out the contact form at http://www.EnduringInvestments.com/contact and we will send you our latest Quarterly Inflation Outlook. And if you make sure to put your physical mailing address in the "comment" section of the contact form, we will also send you a copy of Michael Ashton's book "Maestro, My Ass!"