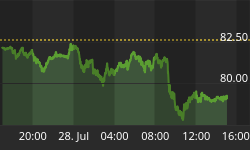

Ah, it is so nice to be in this illiquid period right before quarter-end, when interested parties can easily ramp up prices to where they need them to be in order to get good end-of-period marks. One would think this game would diminish somewhat, given the crusades against the LIBOR and possibly FX price-setting conspiracies, but there's no conspiracy here. There's no need for investors and dealers to discuss putting the stock market up; everyone knows it happens and everyone knows why. The hedgies who flush microcaps higher because they can ought to be stopped, but there's no way to stop the general tendency, especially when you have very clear indications of when that trade is supposed to begin...such as when Fed officials show up and start chanting "stocks shouldn't go down!" in unison.

For the last couple of days, Fed officials have been out in force saying that the "market overreacted." (Mostly, they mean the bond market, but for many people "the market" equals "stocks" because they think CNBC is about "markets" rather than "stocks".) Today, New York Fed President Dudley, Fed Governor Powell, and Atlanta Fed President Lockhart pursued the overreaction theory in separate speeches, echoing Minneapolis Fed President Kocherlakota's sentiment from yesterday. Yes, yes, we all know that everyone else will treat that as a signal to get long again (both stocks and bonds) into quarter-end, but what it really shows is that utter cluelessness of the people in charge at the Fed. Powell said that "Market adjustments since May have been larger than would be justified by any reasonable reassessment of the path of policy." Well, duh. As I pointed out a while ago - before the real selloff - such a virulent selloff was entirely to be expected at some point due to convexity demands. The most-virulent part of the selloff may have coincided with Bernanke's statements last week, and that might have triggered some of the convexity selling, but the degree of selloff had nothing to do with the Fed.

Someone should tell these guys that not everything is controlled by the Fed. Sometimes, rates move for other reasons.

To be sure, the Fed is correct about the fact that their communication is helping to cause the volatility. But it isn't because they haven't been clear enough, or that what they said was misinterpreted. The problem is too much communication, and making the path of policy (and any inflections in that policy path) crystal clear. When policymakers are opaque about monetary policy, then investors change their opinions stochastically, at random intervals; when policymakers set off a flare for every minor change in the trajectory, all investors change positions simultaneously. Transparency not only doesn't reduce volatility, it is a prescription for creating volatility.

Clarity on the fiscal and regulatory front, incidentally, is quite different. Volatility in business ventures is high enough already to ensure that entrepreneurs don't have an incentive to get too far out over their skis no matter how clear the regulatory environment, and decisions made in a business context don't have the hair-trigger half-life of decisions in financial markets. Uncertainty, when long-term decisions have to be made, impairs that decision-making. But uncertainty is good when decisions are easily reversible and the cause of volatility is that consecutive orders to sell aren't spread out enough. For stable markets, you want buys and sells to come all jumbled up, rather than all the buys together or all the sells together. For maximum economic growth, you want risk-takers to have the ability to make long-term decisions with confidence.

So while equity markets have rallied as we approach quarter-end, I don't think this rally will far outlast quarter-end, because there are just too many negatives at the moment for equities - high multiples, rising interest rates, softening global growth, a less-benign regulatory environment etc. The selloff in stocks was never very bad (compared to bonds), because there's not the same kind of convexity problem in stocks, but it also has a lot further to go than bonds do.

Fixed-income markets have rallied along with stocks, with TIPS leading the way up as they led the way down. The interpretation here is different, because in the case of the bond market we are looking at the well-known phenomenon of convexity selling. My advice for fixed-income investors, from long and painful experience, is this: don't jump in with both feet yet. These bounces are normal in this kind of flush. It does probably mean we are closer to the end of the flush than to the beginning, but usually you need a period of a couple of weeks of sideways action before you can start to retrace the "convexity selling" damage and get back to something like fair value.

The healing period is necessary because every prospective bond buyer knows (or should know) that there are large trapped sellers out there who are waiting to pitch bonds overboard (at the new, improved levels!) if there is any sign of further market weakness. The rally over the last few days is fast money, doing what they think the news is telling them to do, and they will be back out as quickly as they got in.

We'll see what happens next week. On the one hand, dealers will have more ability to hold positions (although they're not supposed to, under the Volcker Rule); on the other hand, quarter end will be past and any inclination to hold off to avoid making a bad situation worse will be past as well. It will still be fairly illiquid, with a half-day on Wednesday, the Independence Day holiday on Thursday, and then Payrolls on Friday. I suspect we will see a resumption of prior trends in fixed-income and equities - although I hasten to add as a reminder that there will eventually be a rally off these rates. I just don't think we've exhausted all of the sellers yet.

You can follow me @inflation_guy!

Enduring Investments is a registered investment adviser that specializes in solving inflation-related problems. Fill out the contact form at http://www.EnduringInvestments.com/contact and we will send you our latest Quarterly Inflation Outlook. And if you make sure to put your physical mailing address in the "comment" section of the contact form, we will also send you a copy of Michael Ashton's book "Maestro, My Ass!"