Incredible to me, as well as to many others I am sure, is the fact that the words of one guy, Chairman Bernanke, who is leaving office soon, carries more weight in the market than all of the actual news that we see from day to day.

Today, France's sovereign rating was lowered by S&P to AA+ from AAA. This is more significant than it sounds, since it means that none of the European "bailout" institutions can feasibly carry a AAA rating any more unless Germany and the Netherlands want to guarantee the whole thing. (They don't.) In a humorous note, the French Finance Minister said that the country remains committed to restoring growth, lowering deficits, and adding jobs. Hmmm. One of these three doesn't seem to belong in a statement about restoring the credit of the nation. How does adding jobs - stimulus, that is - help the situation? It was a strange statement.

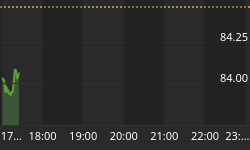

Portugal's situation is worsening again as President Silva is insisting on a broader "unity" government in which all parties participate in the government (and take the heat for austerity measures). Not all of the other parties agree; in particular the Socialists are demanding new elections, while declaring "we must abandon the politics of austerity, and renegotiate the terms of our adjustment programme." In this dust-up, the more extreme elements of the political sphere in Portugal are calling for debt repudiation. Portuguese bond yields (10y) are back up to 7.35%, which is well above the 5.20% lows from May although also a far cry from the 16% levels in the teeth of the crisis early last year (see chart, source Bloomberg).

Philadelphia Fed President Plosser today said in a speech that the Fed should start exiting from the asset purchase program in September, and completely cease buying bonds by the end of the year. He is concerned about causing another housing boom (too late!), and thinks the costs outweigh the further benefits. He is right, and bonds took some brief grief before investors remembered that (a) he's not the Chairman, who has the only vote that matters, and (b) he's not even an FOMC voter this year.

None of this - not France, not Portugal, not Plosser - rattled the U.S. equity market in the slightest, because Bernanke has pledged to keep the taps running as long as possible, tapering slowly, and then maintaining easy policy for a long time. So investors are delighted to see stocks at all-time (nominal) price highs with nearly a 24 Shiller P/E. At these levels, the expected real total return for the next decade from the stock market is less than 1.75% per annum...with 10-year TIPS yielding 0.50%.

So does the continued presence of easy money from the Fed warrant exceptional risk-taking and valuation in equities? It seems to me that it does not. Removing QE is, of course, tightening relative to the baseline of current policy. Policy may remain absolutely easy, but it is going to be relatively tighter...and the direction of interest rates, not merely their level, matters to investors. Of course, Fed mouthpieces clearly want to suggest that "policy will remain accommodative." Indeed it will, and it will also remain accommodative when the Fed Funds rate rises to 1%...and 2%...and 3% someday. But it will be less accommodative, or in other words: more restrictive.

The word-smithing by the Chairman in this regard is understandable, because the jawboning is an important part of policy for a central bank that is nearly impotent due to prior decisions. But it is absurd. Previously, investors were asked to stomach the "Perpetual Motion Machine" interpretation of policy: that buying bonds would push interest rates lower and increase economic activity, while selling them wouldn't push rates higher or decrease activity (or prices in related markets). This latest tweak to the argument asks us to believe also that buying fewer bonds has the same (positive) effect as buying a lot of bonds!

Again, I completely understand why the Fed is trying to jawbone the markets to their way of thinking. But you can't jawbone a bungee jump, and the inflection of policy here is the start of a bungee jump.

The risk here is that investors decide that the Fed is really going to be slow at removing accommodation (which I think is correct), but inflation is going to start to be problematic sooner than that. That sort of attitude adjustment may be closer than you think, for two reasons. First of all, the CPI report is due on Tuesday. Market expectations are for a figure lower than last month's +0.17% rise in core inflation, and a decline in the year/year core inflation rate to +1.6% (from 1.7%) as last June's +0.21% rolls out of the 12-month comparison. I believe there is a good chance that core comes in better than that, although it is unlikely to push the year-on-year change higher. But it could, since housing continues to accelerate and these low figures require ever-increasing drag from core goods prices. In any event, though, inflation will accelerate on a year-on-year basis in August, because the easy comparisons begin: +0.10%, +0.06%, +0.15%, +0.17%, +0.12%, and +0.12% are the monthly changes in core prices for the last six months of 2012: a 1.4% pace in aggregate. And the underlying inflation dynamics are accelerating at the same time.

The second reason that inflation expectations may begin to rise among investors soon is more pedestrian (in more ways than one): gasoline prices have recent spiked 40 cents in the futures markets, from near the lows of the year to near the highs of the year. This will pass through to retail gasoline prices over the next few weeks. If gasoline prices do not rise further from here, then no important shift in inflation perceptions will likely happen. But keep an eye on this. Enduring Investments' sophisticated measure of "consumer inflation angst" has been at multi-decade lows for some time (see chart), but a fairly reasonable shortcut way to evaluate how consumers are feeling about inflation is to look at prices at the gas pump.

You should note that there are two spikes on this chart. One covers the move higher from March 2001 to February 2003, a period during which stocks fell 28%. The second covers May 2007 to July 2009, covering a 35% slump in prices. (There is also a minor blip from November 2010 to September 2011, a period during which the S&P only dropped 4%.)

Of course, increasing consumer inflation angst wasn't the only thing that was happening during those periods that helped to drive stocks down. Among other things, valuations were high. Indeed, valuations were high partly because inflation angst was so low. And one ought to consider this: if stocks decline from here in concert with rising inflation expectations, we would be able to say the same thing looking back: it isn't only rising inflation expectations, but also high valuations and plenty of bad news to go around.

You can follow me @inflation_guy!

Enduring Investments is a registered investment adviser that specializes in solving inflation-related problems. Fill out the contact form at http://www.EnduringInvestments.com/contact and we will send you our latest Quarterly Inflation Outlook. And if you make sure to put your physical mailing address in the "comment" section of the contact form, we will also send you a copy of Michael Ashton's book "Maestro, My Ass!"