Weekly Markets

Precious Metals - Oil

Other Commodities - Currencies

Bonds - Stocks

Weekly Commentary

Growing Concerns regarding Debt Levels & Excessive Leverage

Opinions

Sunday Times: Is the Bubble about to Burst?

Oil Price Surge & Exxon Mobil Report

OECD Senior Economist warns of risk of

Financial Accident

| Current Level | 5 Days | 1 Year | 5 Year | |

| Gold | 419.30 | +0.5% | +6.2% | +53.1% |

| Silver | 7.27 | +4.8% | +17.6% | +45.7% |

| S&P | 1,198.78 | +0.8% | +7.7% | -12.7% |

| Nasdaq | 2,075.73 | +1.4% | +4.6% | -34.4% |

| ISEQ | 6,223.12 | +1.1% | +20.7% | +21.4% |

| FTSE | 4,986.30 | +0.3% | +12.9% | -18.1% |

| USD/EUR | 0.7994 | +1.0% | -2.0% | -27.5% |

| OIL (Nymex) | 51.85 | +10.8% | 31.5% | +80.2% |

Weekly Markets

Stock markets were up marginally for the week.

Bond markets were largely unchanged.

Commodities were up and silver rallied 4.7% and oil surged 10.8%.

Precious Metals

For the week, gold futures added 0.5%, silver advanced 4.7% and platinum was up nearly 0.3%, but palladium lost 1.9%.

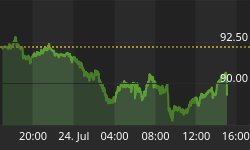

Gold was up $2.40 or 0.5% for the week. From $417.30 to $419.80 per ounce.

Silver was very strong and rallied sharply from $6.94 per ounce to $7.27.

Platinum (July) was down 1.9%, finishing at $864.70 from $862.50 per ounce

Palladium (June) was down also down marginally from $187.75 to $184.35 per ounce.

The Financial Times reported how the price of silver could this year test the 17-year high reached in 2004 as industrial demand increases and due to investment from funds and high net-worth individuals. , according to GFMS, the precious metals consultancy.

The comments by Philip Klapwijk, executive chairman, came as The Silver Institute released its annual report on the industry. Mr Klapwijk expects silver to trade near the $8.29 a troy ounce reached in April 2004, a level previously seen in 1987, provided there is a gold rally later in the year. Gold has a large influence on the price of silver, which was yesterday trading at about $7 a troy ounce.

Last month, Mr Klapwijk predicted gold could trade as high as $500 a troy ounce by year-end. The World Silver Survey 2005 says silver prices averaged $6.66 a troy ounce in calendar 2004, a rise of 36 per cent year-on-year. The price gain was driven mainly by investment from funds and high net-worth individuals.

It says investment accounted for 42.5m ounces of silver, a fivefold increase on the previous year. At the moment investment represents only some 5 per cent of total silver demand.

UBS commented during the week on unusually strong demand for physical gold bullion in Switzerland. "We have spoken repeatedly about the strength of the metal in non-USD terms in spite of large speculative selling from Comex running at a rate of 2.5-3.0 million ounces per week over the last three months. The reason for this appears to be largely related to physical demand; our Zurich physical sales team estimate that Swiss sales of physical gold are currently running at a rate of about 1.5 million ounces per week, with all refineries running at full speed, including weekends, which is a very unusual development."

Reuters reported how Afshin Nabavi, senior vice president at MKS Finance believed that price levels would have difficulty going down. "I think the market is stuck". He said "On the downside we are seeing extraordinary support from physical buyers so the market shouldn't move any lower than $416,"

Strong global physical demand continues. The Economic Times of India reported how 'Gold's scarce: find out why':

"The recent price slide has caused a sudden scarcity of gold. The local supplyof the yellow metal is drying up with traders having bought gold at higher prices,unwilling to sell it now.

China Economic reported a 'Glittering recovery predicted for gold': "The World Gold Council, the London-based gold marketing organization funded by the world's leading gold mining firms, predicted consumer demand for gold in the Chinese mainland will increase by more than 10 per cent this year from 234 tons in 2004."

Dow Jones Newswires via Yahoo Business also reported on the substantial growing demand in China Urban Youth, Investors Boost China Gold Demand. Gold and Silver Investments Limited were featured and quoted in the article: http://sg.biz.yahoo.com/050525/15/3soyk.html

Silver strong surge meant that it closed convincingly above the falling wedge seen above - a tight and gradually narrower trading range which had recently formed. Normally such closes are followed by strong follow through movements. A few closes above $7.29 may result in a challenge of silver's highs of $8.04 per ounce in early December 2004.

Gold May Climb as Rising Oil Costs Spur Inflation, Survey Says - Bloomberg, 30-05-05

The Gulf Cooperation Council Urged to Peg Its Currency to Gold - Arab News, 30-05-05

Oil

Oil surged 10.8%. The price for a barrel of oil surged from $46.80 to $51.85. For the week, oil was up by $5.05.

Rumours of the serious ill health of King Fahd of Saudi Arabia. The world's largest oil producer declared a state of alert and cancelled the leave of its security forces. King Fahd was hospitalized on Friday and the Ministry of the Interior officials issued the state of alert.

Economic growth is not possible without energy. According to all indicators, the world's energy supply is depleting much faster than the world leaders had anticipated.

Exxon Mobil recently reported the highest quarterly profit ever of some $8.42 billion. Of far more significance was their largely overlooked report 'The Outlook for Energy: A 2030 View', which forecasts a peak in non-OPEC oil production in just five years. Alfred Cavallo writing in the respected Bulletin of the Atomic Scientists wrote how "In the past, many who expressed such concerns were dismissed as eager catastrophists, peddling the latest Malthusian prophecy of the impending collapse of fossil-fueled civilization. Their reliance on private oil-reserve data that is unverifiable by other analysts, and their use of models that ignore political and economic factors, have led to frequent erroneous pronouncements. They were countered by the extreme optimists, who believed that we would never need to think about such problems and that the markets would take care of everything. Up to now, those who worried about limited petroleum supplies have been at best ignored, and at worst openly ridiculed....

What all this means is that the petroleum industry is approaching a turning point. Conventional petroleum production will soon--perhaps in five years, ten at best--no longer be able to satisfy demand. For their part, American consumers would do well to take a cue from their Western European counterparts, who enjoy a comfortable lifestyle despite a per capita use of petroleum that is half of that in the United States."

All the oil majors are experiencing declining discoveries. Indeed many firms are reporting disappearing reserves. Royal Dutch Shell has admitted it overstated reserves by 20 percent in 2004. BP have also restated and reduced estimates of their reserves.

The consulting firm, HIS, who catalogue oil reserves and discoveries have pointed out that the year 2003 was the first time since the 1920's there was not a single discovery of an oil field in excess of 500 million barrels.

Dr Jeremy Leggett wrote in Energy Bulletin and The Independent of London how "The record of oil discovery shows clearly that all is not well. The world's biggest oil-fields, the giants of Saudi Arabia and Kuwait, were discovered way back in the 1930s and 1940s. The last time a major oil province was discovered was in the 1970s. The last time we discovered more oil in a year than was used was a quarter of a century ago. Half the world's current production comes from the 100 biggest fields, and almost all of these are more than 25 years old. The recent rate of discovery of "giant" oil-fields, of more than 500 million barrels, is as follows: in 2000 there were 16 discoveries, in 2001 nine, in 2002 just two, and in 2003 none. It takes six years from the discovery of an oil-field for the first oil to come to market. And even if they're called "giant", they still represent less than a week's global supply at current demand rate." www.energybulletin.net/5627.html

Leggett is now Chief Executive of Solar Century and is another former oil industry insider to have warned regarding peak oil production. Along with these insiders it seems like Exxon Mobil are now coming out of the closet. They now join the many former industry insiders and the present insiders such as the CEO of Simmons and Comp International, Matt Simmons. He is an energy adviser to the Bush Administration who has has been repeatedly warning regarding peak oil. The Washington Times reported his view that Saudi Arabia has been overstating its oil reserves for years and that its biggest oil fields are in decline. Simmons is the CEO of one of the most respected investment bankers to the energy industry and has a book coming out soon entitled 'Twilight In The Desert: The Coming Saudi Oil Shock And The World Economy'.

http://washingtontimes.com/upi-breaking/20050503-034026-2579r.htm

Also during the week the Deputy Prime Minister of Australia acknowledged the threat of peak oil.

Warren Buffett through Berkshire Hathaway bought an electric utility. It is unlikely that Buffett would buy something which didn't have pricing power and this would seem to indicate that Buffet's and Berkshire Hathaway's long-term energy price outlook is for higher prices.

Other Commodities

Reuters Commodities Research Bureau's Index was up strongly from 293.28 last Friday to 300.89 for a gain of 2.6%.

The CRB's year to date gains are at 6%.

Since hitting a low of 182.83 in October 2001 it is up some 65%.

The Reuters CRB Index ( the 17 basic components include hard tangible assets such as Metals, Textiles and Fibers, Livestock and Products, Fats and Oils, Raw Industrials, Foodstuffs). One of the CRB index's greatest strengths is the fact that there is an equal weighting of all of its 17 components. This weighting assures that no price increase in any single commodity, like oil, can significantly skew the entire index. Significant moves in the CRB are only possible when the majority of its component commodities are moving in unison with a particular primary trend. Oil, silver and gold only account for 3/17th of the entire index.

The Goldman Sachs Commodities Index was up 4%. The GSCI is a world production-weighted commodity index which next year will be composed of 24 liquid exchange traded futures contracts. The GSCI includes energy, industrial metals, precious metals, agricultural and livestock products. It is up 14.3% year to date.

Currencies

The U.S. dollar index was down 0.15 points from 86.61 to 86.46 on Friday.

The Euro index was up from 125.45 to 125.83 Friday. The euro was up 0.65% for the week.

The British pound was largely unchanged against the dollar for the week.

The Japanese yen was up marginally 0.28 points to 92.65 Friday.

Bonds

The treasury and bond markets were largely unchanged with yields falling slightly.

The 10-Year Treasury note yield was largely unchanged for the week from 4.125% to 4.073%.

Five-year Treasury yields were down 5 basis points, ending the week at 3.81%.

Two-year Treasury yields ended the week down 2 basis points to 3.64%.

Long-bond (30 year) yields dropped 1 basis points to 4.43%.

The spread between 2 and 30-year government yields declined from 78 to 77.

Stocks

The stock markets were up marginally. The Dow and S&P are at two month highs but still down year to date.

The Dow Jones Industrial Average was up from 10,472 to 10,549.

The S&P 500 Index was up from 1189.28 to 1199.

The Nasdaq Composite was up 3.52% for the week to 1976.8 after a late day rally on Friday.

The FTSE was up 0.3% and the ISEQ was again stronger and was up nearly 1.4%.

The broader US stock market was mixed also.

The Transports were unchanged despite the soaring oil price.

Utilities were up marginally.

The Morgan Stanley Consumer index was lower marginally%.

The Morgan Stanley Cyclical index was up 1%.

The small cap Russell 2000 and S&P400 Mid-cap indices were both up some 1%.

The NASDAQ100 and the Morgan Stanley High Tech index were up 1.5% and 1% respectively.

The Semiconductors were also up 1%.

The Street.com Internet Index and NASDAQ Telecommunications indices were up 3% and 1% respectively with Google's relentless march to the heavens continuing.

Biotechs were up 1%.

The more interest sensitive Broker/Dealers were down 1% and the Banks were down 0.5%.

The XAU Index of large precious metal mining stocks was up strongly some 7.1%.

The HUI (AMEX's Gold BUGS index) a basket of unhedged gold and silver stocks was up 8.7%.

Other Credit and Money Supply Indicators

Broad money supply (M3) declined $3.3 billion to $9.578Trillion (week of May 16). Year-to-date, M3 has expanded at a 2.7% rate, with M3-less Money Funds growing at 4.9% pace. For the week, Currency added $0.7 billion. Demand & Checkable Deposits dropped $12.7 billion. Savings Deposits gained $2.5 billion. Small Denominated Deposits rose $4.3 billion. Retail Money Fund deposits dipped $2.4 billion, and Institutional Money Fund deposits declined $2.8 billion. Large Denominated Deposits added $1.3 billion. For the week, Repurchase Agreements gained $7.0 billion (up $43.5bn in 5 wks), while Eurodollar deposits declined $1.2 billion.

Bank Credit expanded $4.2 billion last week, increasing the year-to-date expansion to $345 billion, or 13.3% annualized. Securities Credit is up $133 billion, or 18.1% annualized, year-to-date. Loans & Leases have expanded at an 11.2% pace so far during 2005, with Commercial & Industrial (C&I) Loans up an annualized 19%. For the week, Securities added $0.7 billion. C&I loans jumped $5.0 billion. Real Estate loans dropped $9.5 billion. Real Estate loans have expanded at a 12.5% rate during the first 20 weeks of 2005 to $2.66 Trillion. Real Estate loans are up $287 billion, or 12.1%, over the past 52 weeks. For the week, consumer loans gained $3.9 billion, and Securities loans rose $5.8 billion. Other loans dipped $1.7 billion.

Total Commercial Paper rose $4.9 billion last week (up $34.6bn in 3 wks) to $1.519 Trillion. Total CP has expanded at an 18.5% rate y-t-d (up 13.1% over the past 52 weeks). Financial CP increased $2.0 billion last week to $1.365 Trillion, with a y-t-d gain of $81 billion (15.6% ann.). Non-financial CP rose $2.8 billion to $154 billion (up 28% in 52 wks). It is worth noting that Total CP has now increased $105.5 billion y-t-d compared to M3's $98.3 billion.

Fed Foreign Holdings of Treasury, Agency Debt rose $6.8 billion to $1.411 Trillion for the week ended May 25. "Custody" holdings are up $75.1 billion, or 13.9% annualized, year-to-date (up $200bn, or 16.5%, over 52 weeks). Federal Reserve Credit declined $1.0 billion to $786.6 billion. Fed Credit has declined 1.3% annualized y-t-d (up $42.9bn, or 5.8%, over 52 weeks).

ABS issuance ballooned to $23.5 billion (from JPMorgan). Year-to-date issuance of $269 billion is 15% ahead of comparable 2004. At $171 billion, y-t-d home equity ABS issuance is 23% above the year ago level.

(Noland, Prudent Bear)

Commentary

There are growing concerns in the western world about record debt levels and the possibility of bubbles in property markets.

A long overdue debate in the business and financial press about these issues has been engendered due to Alan Greenspan recent remarks about the possibility of a property bubble in the US. Greenspan said that it is "pretty clear" that the US property market has "an unsustainable underlying pattern". He warned that there was froth in the US property markets. Froth is a a mass of small bubbles and Greenspan explicitly warned of "a lot of local bubbles". Greenspan was presumably referring to the property markets which have experienced the largest price appreciation in Florida, California, San Diego, New York and Washington.

Source: Economics & Strategy - CIBC World Markets - Shenfeld, MD and Senior Economist, CIBC

This increasingly speculative housing boom is being fuelled by massive debt levels both in the US and in the UK.

The British Conservative Party's Debt Commission gave their conclusions in late March. They said that the standard of living of around 15 million people is threatened by the current unsecured personal debt level of £1,920 billion. The Chairman of the Commission, Lord Griffiths, a former director of the Bank of England, warned that Britain's personal debt 'timebomb' mountain poses a real financial threat to more than 15 million people or more than 25% of the population.

We are bombarded with so many facts, figures and statistics these days that when confronted with such large figures one's eyes can easily glaze over. When one gets into the realms of such astronomical figures one can easily fail to grasp the enormity of such sums of money or debt and their implications for the wider economy.

£1.92 trillion is £1,920 billion or £1,920,000,000,000 that has to be paid back to lenders plus interest. Much of the debt is in the form of credit card debt which is subject to adjustable rates and in a rising interest rate environment the costs of servicing such debts will increase.

The majority of people should be in a position to maintain their debt repayments. But in an era when many couples are dependent on two salaries in order to pay their mortgages any change in their financial position due to serious illness, family difficulties, loss of a job or any of the many other difficulties which life has a habit of throwing up will create financial distress. There may be a significant minority of borrowers at the margin who will not be able to maintain their debt repayments and their difficulties may have implications for the wider economy with regard to consumer confidence and consumer sales going forward.

Also during the week came a warning from Barclays, Britain's biggest credit card lender, that bad consumer debts were rising faster than expected. This raised fears for the whole banking sector driving financial shares lower.

Concerns about soaring levels of consumer debt are likely to rise, particularly over the willingness of banks to give large loans to poorer households. Write-offs in the fourth quarter of 2004 are expected to reach a record level of more than £6 billion for the year as whole, according to a report in the Financial Times. The last time bad debt write-offs reached this level was in 1993, when Britain was mired in a recession.

This situation is the same, if not worse, in the U.S. The number of bankruptcy filings is a barometer of the intensifying economic insecurity and ever-rising debt load of American families. Personal bankruptcies have soared from 200,000 a year in 1978 to 1.6 million in 2004. The debt burden carried by the average US household is very large. In 1946, at the beginning of the post-World War II economic boom, consumer debt amounted to 22 percent of after-tax household income. Now debt is proportionally five times as great, amounting to nearly 110 percent of income.

For much of the postwar boom period, rising consumer debts took the form of home mortgages, car loans and revolving credit balances with department stores or essentials such as shelter, transport and food. Credit card debt (which was generally used for the purchase of less necessary consumer goods but is increasingly being used by distressed citizens in order to buy food and other essentials) only began to become a major factor in the 1970s and 1980s. From 1989 to 2001, according to a recent report by the public policy group Demos, credit card debt nearly tripled, from $238 billion to $692 billion. During the same period, the savings rate plunged and the number of bankruptcy filings jumped 125 percent. While middle-class families saw a 75 percent increase in credit card debt, the more vulnerable were much more likely to plunge over their heads: credit card debt for senior citizens rocketed 149 percent, and for very low-income families, making $10,000 a year or less, the increase was 184 percent.

The explosion in consumer debt is also due to the boom in home mortgage refinancing and the increasing instability of working class and middle class incomes, which has compelled more and more families to rely on credit to offset sudden drops in earnings and sustain consumption. From 2000 to 2003, home mortgage debt soared by more than one-third, from $4.9 trillion in 2000 to $6.8 trillion in 2003. Even though many homeowners refinanced their mortgages to use home equity to pay down debt, non-mortgage consumer credit still climbed by 15 percent, or $300 billion. The proportion of homeowners' equity in their own homes was 86 percent in 1945; by 1990 it had fallen to 61 percent and by 2003 to only 55 percent of the value of their homes.

These huge debt levels in two of the leading economies of the world, at the same time that the French and German economies are mired in recession do not bode well for the long term economic health of the global economy.

Opinions of the Week

"Thanks to poor macroeconomic policymaking in the U.S. and over-reliance in Europe and Japan on exporting to the U.S., we are heading for an environment where most assets might go down,"

Tim Drayson, ABN AMRO Analyst

"Some artefact or some development, seemingly new and desirable - tulips in Holland, gold in Louisiana, real estate in Florida ... captures the financial mind. The price of the object of speculation goes up ... This increase and the prospect attract new buyers; the new buyers assure a further increase. Yet more are attracted ... " So wrote the economist John Kenneth Galbraith in his Short History of Financial Euphoria.... What worries some analysts is not only the speed with which prices have been rising, but the way in which Americans have suddenly begun financing their purchases. Until recently, the typical buyer sought a fixed-rate 30-year mortgage that set total monthly payments at an unchanging, predictable and affordable level. But times have changed. More Americans - two-thirds of new buyers, by one estimate - are opting for variable-rate mortgages or choosing to pay only the interest in the early years, leaving repayment of the loan till later.... More worrying to those who see a bubble in America's future is the willingness of homeowners who have built up equity in their homes to borrow against that equity, either to finance a spending spree or to invest in more property. Economy.com estimates that Americans borrowed $705 billion against their homes last year, compared with $266 billion in 1999."

Irwin Stelzer, Director of the Hudson Institute, House prices: the bubble that won't burst?, Sunday Times, 29-05-05

"Leverage - the ability to raise vast amounts of cheap debt to finance big ticket deals - has been the vital ingredient fuelling the deal makers in their multi-billion-euro property-buying spree.... However, the country's love affair with debt, and the London property market, could soon begin to wane. Even the power of leverage cannot counteract inflated property values.... "About 20 years ago, the market was dominated by institutions who bought entirely through equity," said Vernon. "In the last 10 years a new model has emerged - the highly leveraged model. Even the institutions themselves are highly leveraged now." ... The flip side of the huge rewards associated with leverage is risk.... The danger for any leveraged deal, more than rising interest rates, is to overpay. The London commercial property market, home to a very large chunk of Irish investors' leveraged bets, is looking choppy. Office rental values in the City of London, the touchstone of the capital's market, have fallen 50% in the last four years and vacancy levels have pushed up to 15%.... The movement of the market against such blatant fundamentals has given rise to talk reminiscent of the tech bubble.... Mark Richards, an economist with Lombard Street Research, a UK-based economic think tank, believes the market is in danger of overheating. "It seems hard to justify the high prices that are being paid for commercial property at the moment. There is a risk that we are going into real bubble territory from here," said one London-based property analyst with a US brokerage. "Unlike the last bubble in the late 1980s, this is a bubble in terms of valuation." He said tycoons such as Gerald Ronson and Nick Leslau had been selling commercial property arguing that the market was becoming overheated. "These guys are savvy and very well-respected investors in property, so when they move, others really have to start taking note," said the analyst.

Brian Carey & Joe Brennan, Focus: Is the Bubble about to Burst?, Sunday Times, 29-05-05

"The past seldom obliges by revealing to us when wildness will break out in the future. Wars, depressions, stock-market booms and crashes, and ethnic massacres come and go, but they always seem to arrive as surprises. After the fact, however, when we study the history of what happened, the source of the wildness appears to be so obvious to us that we have a hard time understanding how people on the scene were oblivious to what lay wait for them."

Peter Bernstein, 'Against the Gods - The Remarkable Story of Risk' as quoted by

Jack Crooks, Bond bubble, American-style, Asia Times

"Every big market decline must have scapegoats to blame for losses. While the timing of the next market collapse is anything but clear, the scapegoat is already in view. It will be those horrid hedge funds.

In recent weeks, the blame for every little market gyration, whether in bonds, commodities or stocks, seems to have been assigned by some commentator or other to a hedge fund strategy gone awry. Memories of Long-Term Capital Management, whose near collapse in 1998 so alarmed Wall Street that the Federal Reserve organized a rescue, are fresh again."

Floyd Norris, Who's to Blame? Hedge Funds,New York Times, 27-05-05

"We have two huge deficits, in our federal budget and our balance of payments, and we are essentially depending on strangers to finance them ... Anne Colamosca, with whom I've written two books, and I are testifying this week before the congressional commission on trade with China. We've just handed in our testimony, and one of our basic points is that the best way to characterize the American economy right now is as the "Blanche DuBois Economy." She, you will remember, was a major character in Tennessee Williams' 'Steetcar Named Desire'.

Her most famous line, of course, is "I have always depended on the kindness of strangers." And that's the position that the U.S. finds itself in right now. We have two huge deficits -- in our federal budget and our balance of payments -- and we are essentially depending on strangers to finance them.

It's obvious that fighting a war and cutting taxes at the same time has been a profligate way to run the economy. And I find it hard to believe that there will not be consequences in terms of slow growth and tough employment opportunities in America before it's all over."

William Wolman, Former Business Week Chief Economist and Author The US economy is too dependant on the kindness of China, Business Week

"Last year Wal-Mart (America and the world's biggest retail stores group) imported $18 billion worth of goods from China. Of Wal-Mart's 6,000 suppliers, 80 percent are from China."

Newsweek, From the May 9th issue

"Yahoo and Google's total ad revenues this year could rival the combined prime-time ad revenues of ABC, CBS, and NBC -- a stunning achievement for the companies and a watershed moment for the Internet as an advertising medium."

Advertising Age, From the April 4th issue

"It is 2 o'clock on a hypothetical Monday afternoon, and the Dow Jones industrial average has plummeted 664 points, on top of a 847-point slide the previous week.

The chairman of the New York Stock Exchange has called the White House chief of staff and asked permission to close the world's most important stock market. By law, only the president can authorize a shutdown of U.S. financial markets.

In the Oval Office, the president confers with the members of his Working Group on Financial Markets -- the secretary of the treasury and the chairmen of the Federal Reserve Board, the Securities and Exchange Commission and the Commodity Futures Trading Commission."

Brett D. Fromson, Plunge Protection Team, Washington Post

"Without any press conferences, grand announcements, or hyperbolic advertising campaigns, the Exxon Mobil Corporation, one of the world's largest publicly owned petroleum companies, has quietly joined the ranks of those who are predicting an impending plateau in non-OPEC oil production. Their report, The Outlook for Energy: A 2030 View, forecasts a peak in just five years."

Alfred Cavallo, Oil: Caveat Empty - Bulletin of the Atomic Scientists, 27-05-05

"Fat tail events are things that are so unlikely you're not supposed to worry about them at all. Like the risk of nuclear war or a stock market crash. They are called "fat tails" because they appear on the far extremities of bell curves...where the lines are supposed to tail out to nothing. Instead, they often bulge; they grow suddenly fat - there are most extreme events than statisticians think there ought to be. Things that are not supposed to happen do happen more often than most people expect. We don't know how great the risks of nuclear attacks really are ... but we'd much rather wait it out in Nice, France, than in Farmington, New Mexico. The food is better, the beach is closer ... and both the women and the buildings are prettier....

In the financial markets, too ... we have the impression that the earth is beginning to rumble. Here in Britain, every day seems to bring more bad news. The day before yesterday, factory output was at a 10-year low. Yesterday, retail sales took their biggest plunge in 10 years. And in the United States, we have this stunning news from The Financial Times: "Real wages fall at fastest rate in 14 years."

We are tempted to stop right there. We have been saying for years that consumer spending cannot make people rich; instead, it makes them poor. You don't get rich by spending; you get rich by saving ... and building new businesses, new factories, and new and better products. You get rich by foregoing consumption in favor of production - so you can produce better automobiles, for example, than your competitors. But the United States has done just the opposite. It consumes and allows its competitors to invest and produce. That's why GM and Ford are now facing bankruptcy (not immediately) ... while Toyota is reporting the strongest sales and highest profits ever....

Real wages are falling for the very reasons we've described so often. In the new, globalised division of labor there are billions of people ready to do Americans' work more cheaply. They save. They invest. They build new factories. Their wages and profits increase. Ours decline"

Bill Bonner, Shanghai Surprise, Daily Reckoning

"Remember the stock market bubble? With everything that's happened since 2000, it feels like ancient history. But a few pessimists, notably Stephen Roach of Morgan Stanley, argue that we have not yet paid the price for our past excesses. I've never fully accepted that view. But looking at the housing market, I'm starting to reconsider.

In July 2001, Paul McCulley, an economist at Pimco, the giant bond fund, predicted that the Federal Reserve would simply replace one bubble with another. "There is room," he wrote, "for the Fed to create a bubble in housing prices, if necessary, to sustain American hedonism. And I think the Fed has the will to do so, even though political correctness would demand that Mr. Greenspan deny any such thing....

But although the housing boom has lasted longer than anyone could have imagined, the economy would still be in big trouble if it came to an end. That is, if the hectic pace of home construction were to cool, and consumers were to stop borrowing against their houses, the economy would slow down sharply. If housing prices actually started falling, we'd be looking at a very nasty scene, in which both construction and consumer spending would plunge, pushing the economy right back into recession.

That's why it's so ominous to see signs that America's housing market, like the stock market at the end of the last decade, is approaching the final, feverish stages of a speculative bubble.

Some analysts still insist that housing prices aren't out of line. But someone will always come up with reasons why seemingly absurd asset prices make sense. Remember "Dow 36,000"? Robert Shiller, who argued against such rationalizations and correctly called the stock bubble in his book "Irrational Exuberance," has added an ominous analysis of the housing market to the new edition, and says the housing bubble "may be the biggest bubble in U.S. history"

Paul Krugman, Running Out of Bubbles, New York Times, 27-05-05

"The "will the economy tank?" concerns have clicked up a few degrees this week, for there has been a flood of disquieting data both in the UK and in Europe. This is not hugely unexpected - at least not to anyone with any sensitivity for the way the UK and European economies have been moving, as these columns have reflected. It would be more surprising if the numbers were coming in above the official expectations. But it is worrying, none the less, even to those of us who were already quite worried.... Hanging over all this are the global imbalances. The key is the relationship between the US and China. US demand is still cantering along (the OECD expects 3.6 per cent this year) but the current account deficit gets ever-wider. But this relies on the rest of the world financing the US and trade protectionism in Congress not reaching such a level where it seriously squeezes Chinese imports. The US - and China - need a gradual adjustment but that is hard to engineer. The OECD chief economist, Jean-Philippe Cotis, referred to these imbalances and said that the OECD was not saying there would be a doomsday situation tomorrow morning - but of course that very statement carries the implicit warning that there might be one in the none-too-distant future.

The best answer from a narrow UK stance to the "will the economy tank?" question is: "not as such, but expect slower growth, particular in consumption but also in public spending". From a US perspective it is: "not yet, but the dangers are considerable in the medium term". And from a eurozone perspective, I'm afraid it is: "Germany and Italy at least are not going to have a fun-filled year.""

Hamish McRae, Brakes are on for growth as Britain and EU loses momentum ... The Independent

"Borrowers splurge; the banks whine about bad credit.

For every action, there is an equal and opposite reaction."

Rhys Blakely, When the lenders get physical, Sunday Times, 29-05-05

"We are not saying there will be a doomsday tomorrow morning ... but because the adjustments [to global imbalances] are relatively slow, we are running the risk that an accident will happen. [..] Time is running out - the numbers are getting big, big, big."

Jean-Philippe Cotis, OECD Chief Economist, Interview in the Financial Times

Opinions and Quotes can be found in articles in the Daily News and Commentary sections of www.gold.ie.