The following is part of Pivotal Events that was published for our subscribers November 28, 2013.

Signs Of The Times

"Investors are pouring more money into stock mutual funds than they have in 13 years."

- Bloomberg, November 21

"Printing money is not the way out of the euro zone crisis."

- ECB economist, Bloomberg, November 20

"The extended rise in prices has led to an unsustainable level of consumer indebtedness, as well as overvaluations in the housing market."

- Fitch Ratings on the Canadian housing boom, November 25

"Rising Bad Loans at Indian Banks"

"Record onion prices and the soaring costs of rice and coriander in India are frustrating the battle to curb inflation."

- Bloomberg, November 22

As Peter Sellers would say "My goodness, gracious me".

Stock Markets

Three things seem to have been conditioning the stock market rise.

One is the "Springboard Buy" noted in the October 10th Pivot. Another is the "Horsemen" - a group of stocks that have been steeply rising in a parabolic blow-off.

And then there is the A/D line in the S&P that has been setting new highs as the index made new highs.

The S&P has yet to generate the opposite to the "Springboard".

But, the A/D line kept rising until last Friday when it did not make new highs. It could take a few weeks to complete a negative divergence.

Some of the "Horsemen", such as DDD have hit a brick wall and are faltering.

Almost 200 of these are flying together, if they all decline together it will be interesting.

About a third of such flyers have hit the wall and dropped by some 10 percent.

As the ChartWorks noted on Tuesday, the models of 1926, 1937 and 2007 continue to guide. The path is to a cyclical high.

In the meantime, Thanksgiving weekend is a seasonal positive. Then there is the middle of December when the "small-caps" begin to outperform. Some important highs have been set at the turn of the year. The Nikkei at the end of 1989 is a great example.

Going the other way, crude oil and base metal prices continue weak and are getting depressed.

Base metals (GYX) have declined to a band of support at the 330 level, but is not oversold. The high was 502 set in the first part of 2011 when our Momentum Peak Indicator registered a cyclical top.

Base metal miners (SPTMN) have declined from 1600 in early 2011 to 662 in June. The Daily RSI got as low as 22, which we noted. The index is at 729 and with the RSI at 27, it is getting oversold.

This could decline further in testing the key low at 692.

We have been looking for a tradable low for this sector towards the end of the year.

On path, crude oil has declined from the high of 112 in August to 91.77 yesterday. At 36 the Weekly RSI is at the level that has ended sell-offs over the past year. The plunge with the European Crisis of 2012 ended with the RSI at 28.

As industrial commodities bottom it could set up a significant rotation from "High Flyers" to the "Neglected".

Ross recalls that as the Tech Bubble collapsed in 2000, depressed "value" stocks jumped.

Commodities

As a group, commodities continue to perplex those who learned (long ago) that when the Fed depreciates the dollar hard assets go up. After all, it is a socio-economic law, or should be.

The problem is that both policymakers and hard-asset people remain convinced that Fed expansion of credit stimulates business. And that pushes prices up.

History records that the public decides whether to speculate in tangible or financial assets. This is why we continue to use the classic definition of inflation. "An inordinate expansion of credit", and it does not mention price.

In June we published "Inflation is Instantaneous". This noted that the Fed needs a speculative bid, using leverage, to expand its portion of credit.

That bid can be in tangible or financial assets.

Lately it has been in financial assets and the game changed in 2011 when the CRB soared to 370 in April. Our Momentum Peak Indicator does not often generate signals, but when it does we pay attention. The chart follows.

It soared to 1.34 in April 2011, which we took as a "Sell" on whatever was in play.

Namely, base and precious metals. The highest reached was 1.39 with the blow-off in gold and silver in January 1980. We concluded that the decline in precious metals would be significant, but not as severe as the post-1980 disaster.

Also concluded was that base metals could start a cyclical bear market, which has been the case.

Previously when the big action was in commodities, the bear would be accompanied by a recession. So we expected a recession. This was not the case and we have no explanation other than that the bubble in "paper" is levitating the economy.

In August, agricultural prices (GKX) reached the most oversold on the Weekly reading since the 2008 Crash. With this we thought that the GKX had the best chance for a price recovery. The low then was 361 and the rise made it to 388. The decline was to 358 a few weeks ago. This extended the downtrend, but it is within the general decline in the CRB that is getting close to a tradable bottom.

Currencies

The low for the DX at 79 a month ago looks like what Ross calls an "isolated low".

Often these will clear a market for an intermediate rise.

Last week's conclusion was that the dollar could base at the 81 level for a while.

Our target of the 95 level for the Canadian unit was reached earlier in the month. The rise to 96 rolled over to yesterday's 94.3.

This put the Daily RSI down to 30, which could soon limit the decline. RSI 28 would likely end the move.

The action could remain in this condition until the low is in for most commodities.

Credit Markets

The bond future reached our rebound target level at almost 136 and we took that as completing the rally.

Our technical side considers that the very oversold at 129 in early September needs a good test.

Our "old-timer" side considers that the whole experiment has been absolute madness. It takes a certain level of audacity to try to push short rates down, but it is something else again to try to push long rates down.

What helps the mad men to look good has been that corporate bonds have been doing very well. Zero short rates has forced many investors to buy issues that should have been avoided and the first business cycle out of a classic crash has helped a lot.

A secular decline in yields ended in 1946 and a secular increase began with the dynamic expansion out of a great depression. Ignorant of this pattern, the Treasury started buying bonds out of the market with hopes of keeping rates from rising above 3 percent. This

was intensified in the early 1960s with "Operation Twist". That was to keep them from rising above 6 percent. The high at the end of the secular rise in rates was 15 percent.

Long interest rates for AAA corps declined from 5.5% reached as the 1932 panic ended.

The bull market with the boom drove the yield down to 3.10% at the end of 1936. A sharp but brief rise was associated with the end of that recovery and the end of that bull market in stocks.

What happens to bond prices when commodities turn up?

Corporate spreads relative to treasuries continue to narrow and are slightly better than at the levels reached at important highs. These were in 2004, 2007 and 2011.

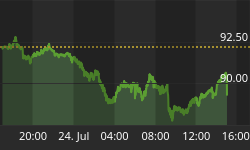

Something Unusual

- Charts like this never happen naturally.

- Something very arbitrary is going on.

- Is it "sustainable"?

- If not, what's next?

Chickens!

- "When the wind blows strong enough, even domestic chickens can fly".

- This is an old stock market saying that was applied to hitherto unexciting "blue chips".

- It suggested that a bull market was getting mature.

- There is a chicken "ranch" in Texas where the wind blows all of the time. On the rare instance when it stops - all of the chickens fall over.

- It is uncertain how this chart applies to today's "High Flyers", but it prompts some puns that are best left to the reader's imagination.

Link to NOVEMBER 28, 2013 Bob Hoye interview on TalkDigitalNetwork.com: http://www.institutionaladvisors.com/1/post/2013/11/bob-hoye-interview14.html