From the HRA Journal: Issue 208-209 (Part ii)

Major Markets:

2013 worked out much better for most major bourses than even optimistic forecasters expected. In large part that was due to multiple expansion. Traders bid up the value of each dollar of earnings and the P/E ratio for the market increased.

That generated great returns last year but don't expect a repeat. Valuations are getting stretched and, so far, forward guidance by companies has been cautious.

Another 30% gain would generate a P/E for the SPX well above 30 without a massive increase in bottom line profits. Companies reporting so far have averaged about 6% YoY profit growth. That won't be enough to underpin multiple expansion.

The depth of the 2008-2009 crash held back retail investors for years even as markets in New York were staging one of the best rallies in history. $1.1 trillion flowed into bond funds as equities were shunned and the trend only started to reverse six months ago.

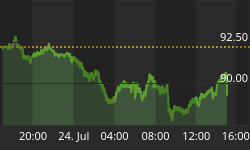

Since the middle of 2013 $90 billion has flowed back into equity funds and ETFs, though quite a bit of that is going to offshore equities. A glance at the charts above for the Nikkei and Euro Stoxx 50 show those were two of the favored destinations for those funds. The Nikkei was the biggest gainer among major world bourses and the Stoxx posted a 30% return since July.

While there have been stories about "massive" rotation into equities there is actually room for a lot more. If markets continue to pull back it might deter retail investors but there is still plenty of ammunition in bond funds that could be redirected to Wall St.

Retail investors got religion thanks to recent daily headlines about new highs on New York bringing back the greed factor. Continued sector rotation into stocks and share buybacks by companies could ensure enough demand to generate a modest return this year even if profit gains are weak.

Anyone with a hint of contrarianism gets queasy when they see how bullish retail investors in New York became. Retail sentiment readings and margin levels were at all-time highs. That almost always ends badly.

NY markets have been negative since the start of the year and the selling has intensified in the past few sessions. Worries about China and emerging market countries are the proximal cause but seasoned traders were looking for a reason to sell.

Economic readings in the US have been mixed since the taper announcement. A pullback is both justified and reasonable. Tamping down excessive optimism now reduces the odds of a much nastier pullback later in the year.

I expect New York to have a positive year but not an impressive one. An assumption that the US economy accelerates a bit more this year underpins that. Returns in the 5-10% range are as much as I would hope for this year unless growth exceeds 3% which doesn't seem to be in the cards yet.

I expect roughly the same sort of gains from Euro stocks. They are a lot less undervalued than they were a few months ago. The Eruo zone has provided most of the positive surprises in economic readings lately. That could be enough to generate returns like the US this year even though the region is still in very rough shape. Returns in Japan will be dependent on how much stimulus Abe applies. Mild inflation could do wonders for the Japanese economy--as long as gains get passed along to consumers and they go out and spend.

Traders are currently fleeing emerging market bourses and currencies so it will be tough for most of those to put in strong years. China is clearly slowing and the level of shadow bank debt is scaring markets everywhere. So far a lot of the moves out of EM countries are repatriation as US yields rise or just reaction to mismanagement. The countries seeing the biggest hits to their markets and currencies are those with overriding political and economic issues. I think the Fed taper is just a convenient excuse, not the reason, for these moves.

The "China Issue":

Debt in China and the speed its increasing at is a big concern. Debt levels are not excessive compared to other economies and certainly not compared to China's ability to generate growth from them. That will change if Beijing can't rein in debt growth.

The bigger issue is that there are plenty of while elephant projects driven by local and provincial governments without the taxing power to pay them off. Some of those will go under.

The "shadow banking" sector is dominated by wealth management funds and special vehicles created to fund projects or companies disguised as more balanced funds promising returns they probably can't generate. Again, some of those are going under. About half the funds are heavily regulated but the special investment vehicles are not.

A couple of prominent investment vehicles are in trouble. Everyone is waiting to see whether the banks that sold (but don't control) them or the government will give some sort of guarantee to unit holders.

This mess exists because China has only partially liberalized its financial system. Banks can set loan rates but Beijing caps rates for savings accounts at 3%. This has been great for the big state-owned banks that have huge loan spreads to work with. Not so much for consumers who were getting savings rates well below inflation. That is the main driver for the growth in the shadow banking sector.

A lot of the sector is similar to money market funds here and probably not in much danger. A lot of others created to invest in sketchy projects will fail and take investor money with them. Most of the money in the shadow bank sector does not appear to be heavily leveraged so in theory even a string of busts should not create systemic risk.

The bigger danger is panic either in China or by western traders reacting to it. China as an economy has massive liquidity and is capable of papering over even large fiscal disasters. It also has political leadership that likes to make examples when it wants to get a point across.

I wouldn't discount the possibility of managers of a blown up fund or two getting thrown in jail or in front of a firing squad. I'm being literal here. Most Chinese would view that as natural justice but it could freak out international investors.

The people running China are smarter than many westerners give them credit for. They are aware of the dangers of being heavy handed. They still might choose to do something drastic to cool off excessive speculation in their economy.

A recent example of this is spikes in overnight interest rates in China's interbank market. Virtually all western observers assume that market has gone beyond the control of the People's Bank of China (PBOC). Many commentators based in China, on the other hand, viewed the spikes as something completely intentional.

Local commentators think the PBOC intentionally allowed rates to spike to send a message to the banks to increase liquidity. They also point out that spikes like that are not uncommon, though they are usually smaller. I don't pretend to have enough insight to know which side is right but it's true that "China bears" have been pretty consistently wrong over the years. The transition to a consumer driven economy will be tricky and is the biggest danger facing the world economy this year and next. I expect bumps along the way but won't assume it's going to generate a lasting crash unless things get much more serious over there.

China's demand for most commodities, iron ore and copper in particular, were much higher than forecast at the start of 2013. How much of this is warehousing and how much is true demand by end users is hard to determine.

Shifting the economy to consumer demand and services should slow the increase in intensity of metals demand. That hasn't happened yet but I think we have to assume it will. Note that we are still talking slower increases rather than absolute decreases in demand.

The latest banking crisis will be another test of the skills of China's leaders. They could drop the ball but until they do I am going to assume this crisis will be managed successfully. It does highlight again that the biggest dangers in China's economy are at lower government levels. City and provincial politicians need to be reined in. That is part of the intent of the latest five year plan but Beijing may need to do something dramatic to force the issue.

Precious Metals:

2013 was a disaster for precious metals but there is growing evidence that 2014 will be better. As I noted above everyone is targeting the $1000-1100 range for gold this year with similar percentage moves for silver. Silver has a bigger industrial demand component that could help it in a stronger economy but, generally, it tracks gold. Comments made about gold below can be assumed to apply to silver.

Gold appears to be putting in a double bottom. As this is written the price is sitting right at the downtrend line defined by price tops through the past year and just below the high reached in early December. If it can break higher here I would expect another flurry of short covering trades.

Physical gold demand absorbed massive selling in the futures and ETF markets last year, albeit at lower prices. This was particularly impressive when you consider moves by India's government to choke off gold demand there. China has assumed the mantle of world's largest gold buyer.

There is no indication that buying is slowing and the confluence of the Lunar New Year in Asia and a stock market correction may be goosing demand again.

ETF selling has recently dried up. I don't know what the true core holding in ETFs is but it's not zero. The further ETF holdings drop the more likely it is that the remainder is in the hands of committed longs who won't add to the selling pressure going forward.

I think 2014 demand out of China will equal 2013 and it could be higher. The biggest potential upside surprise is relaxation of import duties and controls by India. I don't see change there before the May elections. Even then, it depends on who wins. There is a vast amount of gold smuggling going on in India so we don't know how much demand has really dropped off. Even with porous borders Indian gold buying has probably been cut in half so ending the restriction would be huge.

I assume central bank buying of gold remains stable. I ignore China in that equation since Beijing is not telling us how much it's buying. Many assume China has doubled or tripled its gold reserves. I wouldn't be surprised by an announcement like that but the market would be. When China makes its intentions clear a bunch of new gold bulls will be created.

I don't think China will create a gold standard. I do think it will back its currency with gold reserves as several other major economies do. Gold standards handcuff politicians when it comes to monetary policy (that's the whole point). I don't see Chinese leadership putting up with the restrictions.

The combination of balance and probably buying pressure returning to physical markets, skittishness about equities and a continued large short position should be positive. I'm looking at $1400 as a target for this year. That could be raised if things really go our way early in the year. Silver would follow along.

Platinum and palladium have more supply constraints and production is concentrated in unstable countries. Platinum has gained as both a jewelry metal but the auto sector is still the big user. In that sense PGMs are pro-cyclical with demand tracking auto sales.

South Africa has ongoing issues with power generation and labor strife. Most of the deposits there are also inherently expensive to mine as they tend to be both relatively narrow and flat lying. There are still huge PGM deposits in South Africa but few want to tackle the problems that come with mining there.

One positive for South Africa is that the Rand is one of those EM currencies getting hit right now. If the Rand continues to fall it will help the bottom line for miners. I like PGMs in general but I am still looking for a project I really like in a low risk political jurisdiction.

Base Metals:

If we do see a slight increase in growth across the major economic blocks this year it will be a positive for base metals. That doesn't mean they will fly higher though. Several metals and bulk materials are expected to enter or remain in supply surplus this year.

In some cases they are finely balanced and could stabilize under better conditions. The capital intensive projects required by iron ore and coal are still very tough to finance. Some of the expected supply growth in those sub-sectors is still in doubt. Based on its most recent budget, China plans to reduce infrastructure spending in some areas, notably railroads. Private side demand may not be enough to counteract those cuts so I am cautious about iron ore this year.

Above and below are one-year charts for copper, zinc and nickel. All three ended the year at lower prices though zinc came very close to even at year end. I expect similar performances this year.

Copper had the price decline I expected last year. Several copper mine startups did not have the intended effect on copper inventories. Indeed, there was a large decline in warehouse stocks in the second half of 2013 and copper inventories are now on the low side of their five year range.

One important point about warehouse inventories should be made. In the past few years there has been rapid growth in unregistered warehouse stocks and third party warehouses not counted by the LME. Owners could be end users or investment banks or hedge funds holding metal for gains or as hedges. The exact nature of the holdings is impossible to gauge which makes base metal forecasting a lot trickier.

The LME is forcing changes to make it easier for end users to take delivery of metals but inventories are still murky. There has been a lot of strange goings on in the metal space during the past couple of years. There is potential for surprises as the market is (hopefully) brought back to a more transparent state. I think the odds are surprises would be of the upside variety.

2014 should be a surplus year for copper though it now looks like it will be a small one. China is the 800 lb gorilla when it comes to metals but both the US and EU are significant copper end users. If both areas tack on an additional half percent growth copper could end the year close to balanced.

I still think we will see another price decline but it may be smaller than I expected. The red metal could end the year near $3 which would be supportive of copper producers and new projects alike.

Nickel has attracted some attention recently due to a ban on the export of raw concentrate by Indonesia. Indonesia is one of the world's biggest producers. Nickel is produced by a large number of local companies using simple laterite mining.

The local miners that dominate Indonesia's nickel production can't afford to build smelters and Indonesia's grid doesn't have the power to supply them. I think there may be some compromises on the export ban. Even if there are not the Philippines could ramp up production from its similar locally-run operations. Nickel inventories are still rising. I would be hesitant about chasing nickel stories unless they have superior grade. I am not expecting a lot of movement from the nickel price.

Zinc was the best performer among major base metals and that could be repeated this year. The Brunswick mine ended production last year and the Century mine in Australia should be closing next year. Century is the third largest zinc mine and its closure will take almost half a million tonnes of production a year offline.

There are mines in development but none of Century's scale. Zinc's main end uses are in larger scale construction and automotive sectors. It goes without saying that Chinese growth will be the main determinant of demand but zinc is mainly a supply story for now.

LME inventories have dropped by 300,000 tonnes but are still high by historic standards. There should be anticipatory buying closer to yearend that will generate price gains for zinc but it looks like 2015 will be the pivotal year.

The Juniors:

2014 started with the Santa Claus rally we hoped for but it's been cut short by the correction in major markets. The US Dollar and Treasures are getting fear buying though the Dollar isn't trading as well as many expected. That's in part because the Euro and Yen are getting their share (more than, really) of safe haven buying too.

The Christmas rally lifted the Venture index through its 200 day moving average for the first time in almost three years. Nine months of trading flat is the main reason that was possible but it's still a positive sign. December created a double bottom, also a strong technical signal if it holds.

The recent rally carried the index above the resistance level it topped out at three times in 2013. It's tough for microcaps to advance when the big indices are getting pummeled. We'll have to see a bottom to the current correction before we know if this is just another head fake. I think it isn't this time.

That won't be proven until the Venture manages a higher low and rallies to a new high above 987. That would make it a triple bottom and bring the index to its highest level since last April's gold crash.

All that happening presumes two things; that New York is just correcting not crashing and that gold can clear the $1280 level and start hitting buy stops. If these events unfold, which could take a month or two, then I think the Venture could post a 30%+ gain this year.

I mentioned that figure to some of you at the Cambridge conference. Most people were startled at how positive I was. That surprised me in turn because 30% doesn't seem that optimistic a number.

We're talking about a sector that is off by two thirds over the space of three years. A 30% gain barely starts the process of rallying back. We can rally that much just with an end to selling pressure and gains from a small subsector of stocks. 30% is just "the good guys" doing better, not a tide that lifts all boats.

That looks achievable to me if the market can get past the taper panic and gold trades a bit higher. It wouldn't be a banner year but there would be gains to he had in select names. I'll take that for a start.

Newsletter writers Keith Schaefer, Eric Coffin and Lawrence Roulston are bringing the management teams of their 2014 Top Picks to this year's Subscriber Investment Summit at the Downtown Toronto Hilton on Saturday March 1, the day before the PDAC begins. Hear them speak and talk with them directly. Register NOW for FREE--only 200 people can attend and the last two events have sold out. http://toronto-sis-2014.eventbrite.ca

Predictions for 2014