It might seem crazy what I'm 'bout to say

Sunshine she's here, you can take a break

I'm a hot air balloon that could go to space

With the air, like I don't care baby by the way

- From "Happy" by Pharrell Williams

Cliff Asness and John Liew have an article that is in the latest issue of Institutional Investor, discussing the development, strengths, and shortfalls of the Efficient Market Hypothesis, which underlies the Nobel award for both Fama (as a proponent) and Shiller (as a skeptic) this year.One of the interesting points that Asness and Liew make is that examinations of market efficiency depend on the "joint hypothesis" that (a) prices move efficiently to represent correct values, and (b) the model of values that they move to is correct. They point out that if prices seem to deviate from fair value (as expressed by a model), that could mean that either markets are inefficient/irrational, or that the model is wrong (or both). And they suggest strengthening the EMH to include a limitation on such models that they make some kind of sense - since a model that incorporates irrational behavior might well-describe all sorts of crazy market action but not be "efficient" in any sense that makes sense to us.

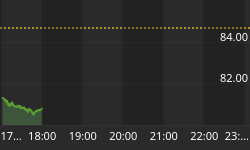

This may not be an irrelevant reflection, given the price events of today. Stocks more than rebounded from yesterday's Ukraine-induced selloff, implying that not only are stocks just as valuable today as they were yesterday, but that they are even more valuable than they were before we found out about escalating tensions in the Crimean. This seems to border on the "unusual model" side of things - especially since nothing particularly soothing happened today.

Earlier today, Reuters reported that one of the Russian threats made in response to the vague declarations of the U.S. that "all options are on the table, from diplomatic to economic" (pointedly leaving out "military," as Obama did yesterday, because gosh knows we don't want the Russians to think that's even a possibility) was that Russians might not repay loans due to U.S. banks (or, presumably, European banks if they joined any sanctions). This is a clever threat, in the old vein of "if you owe $100, it's your problem; if you owe $1 billion, it's the bank's problem." Everyone who thinks that economic sanctions are a no-brainer are correct, in the sense that it would imply no brain.

Russia also tested an intercontinental ballistic missile. This was "viewed as non-threatening and is not connected to what is going on in Crimea," which is of course absurd: regardless of how long the test has been scheduled, someone who was trying to "de-escalate" tensions would surely defer the test for a week. The fact that the test happened is one of many signs today that Putin's soothing words were hollow. All of the actions today, from additional warships steaming towards the Crimean peninsula to ICBM launches and confrontations between Ukrainian and Russian troops, were consistent with an escalating crisis even as Putin said there was no "immediate" need to invade eastern Ukraine.

Stocks loved the idea that the conflict may be over, with the west simply conceding the Crimea and Russia deciding that she is sated for the time being, as ridiculously unlikely as that outcome actually is. And, as I fully expected, we heard over and over today the Rothschildian admonition to "buy on the sound of cannons." And indeed, they bought. Oh, how they bought. The S&P rose 1.53% and most European bourses were up 2%-3%. The expected comparisons were made, to the performance of equities during and following the Cuban Missile Crisis, the first Gulf War, and the invasion of the Sudetenland.

These comparisons are all nonsense. Here's why.

| Event | Date | CAPE prior to |

| Sudetenland | June 1938 | 11.99 |

| Cuba | Oct 1962 | 17.32 |

| Kuwait | Aug 1990 | 16.17 |

| Ukraine | now | 24.87 |

This is what happens when people learn the "whats" ofhistory, but don't learn the "whys." The Rothschildian point isn't simply to buy on the sound of cannons. It's to buy when markets are cheap because of the sound of cannons. And that is most assuredly not the case presently. If stocks had dropped 50% because of the Russian invasion, I would have been at the front of the line telling people to buy. It is reckless and feckless to buy when the market is expensive, and there are cannons that suggest a higher risk premium is warranted at least for a time.

Really, what is the risk here, today? Is the risk really that an investor might miss the next 25%, because the world becomes not only safe, but safer than it was a week ago, and a super-cheap market simply takes off? Or is there some risk that an investor might participate in the next -25%? Good heavens, surely the latter is a far greater risk right now. And, after all, Rothschild also said "sell on the sound of trumpets" (it's always interesting how the bearish parts get forgotten), so that if the crisis is over and the west is victorious then you're supposed to be selling! Here I guess is my point: this is not Rothschild's market.

And, as Asness and Liew might put it, the model that implies stocks are more valuable after such an episode...might not be a rational model. But today, Pharrell wins: clap along if you feel like that's what you want to do!>

You can follow me @inflation_guy!

Enduring Investments is a registered investment adviser that specializes in solving inflation-related problems. Fill out the contact form at http://www.EnduringInvestments.com/contact and we will send you our latest Quarterly Inflation Outlook. And if you make sure to put your physical mailing address in the "comment" section of the contact form, we will also send you a copy of Michael Ashton's book "Maestro, My Ass!"