After some considerable selling of gold from the SPDR gold Exchange Traded Fund in the preceding months, early in 2013, Goldman Sachs came out with a warning that the gold price was going to fall and fall heavily. It did after Goldman Sachs and JP Morgan Chase helped it down with a bear-raid. Thereafter, selling from the SPDR fund persisted throughout 2013.

But it became clear that this selling of physical gold provided an opportunity to 'short gold'. Goldman Sachs along with JP Morgan Chase and their clients, followed through on their forecast and around mid-April 2013 plus/minus 400 tonnes of gold was dumped onto the market knocking the gold price down by $200 within a fortnight. This encouraged more selling from the SPDR gold ETF and eventually the gold price was pushed down to $1,180 from the $1,650 level it stood at in early 2013. The 'bear-raid' was effective.

After the 'bear-raid' in April 2013 Asian demand came in, in tremendous force and drained the gold market of all of that tonnage from U.S. sellers of gold taking out a total from the developed world, over the entire year of 2013 around 1,188 tonnes of gold, refining it to 1 Kg bars in Switzerland before shipping it into Asian markets, particularly that of China. The gold price was halted in its fall at $1,280 making a double bottom at that price later in the year.

The time of the year that leading U.S. banks gave their opinion that the gold price will fall to around $1,000. So we ask could they make another 'bear-raid' on the gold price. A look at COMEX shows us record short positions opening up the door for such a raid on the market. But what was evident in the last raid was that the huge short positions prior to that raid needed a physical sales to be made in big sizes for the raid to succeed. Without it, the short sellers on COMEX have to 'hope' the price moves theor way. The ideal time for this we shall call the "Plunkett Point" as the end of the month requires positions on COMEX to be closed or rolled over to the next month.

The reason that equity market growth in the U.S. is underway and caused an institutional sell-off in the gold market throughout 2013 from the gold ETFs is for a similar reason to the one that was given in early 2013 [an equity market boom in the U.S.] but there are significant differences.

-

Sales from the U.S. based gold Exchange Traded Funds such as the SPDR have dropped to the point that net purchases into this fund have occurred in 2014 so far. The supply of nearly 1,300 tonnes has all but dried up. But if a major holder like Paulson came to the market with his holdings such a raid might be possible, but that appears most unlikely in view of the position his funds have taken to date. So a 'bear-raider' would not have the support of the gold E.T.F.s a critical ingredient for such a raid.

-

More importantly, the pricing power of the U.S. gold market that came with the 1,300 tonnes of gold has been used up. With the U.S. accounting for only 7% of global gold demand, the U.S. markets would have to rely on the influence of the derivatives market of COMEX.

-

Chinese demand remains robust with an annualized +2000 tonnes set to being withdrawn from the Shanghai Gold Exchange in 2014. While this is less than the amount seen on 2013 it is sufficient to buoy the gold price at current levels. However, we have no doubt that any physical tonnage would be snapped up by Asia placing heavy upward pressure on the gold price.

-

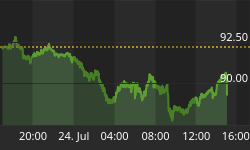

The gold price is not at $1,650, but at $1,250 with strong support underneath it and robust below $1,200. This considerably lessens the vulnerability to the gold price now.

-

Indian demand could resuscitate on the easing of gold import restrictions that severely curtailed Indian gold demand since August last year. The new ruling party is expected to review these restrictions inn the budget in the next week or so.

All in all, the risk-reward ratio does not favour a successful 'bear raid' of the order we saw last year.

Some may point to the additional weight High Frequency Trading could add to downward pressure on the gold price. We see HFT as heavy surf or foam in the market, capable of impacting day traders and shaking out weak demand or supply, but not affecting the underlying current in the gold market. So while such trading may be used in support of heavy physical selling of gold in a 'bear-raid' it will be closed out quickly on the falls. The nature of HFT is such that if it did not create a fall but turned the gold price back upwards, it would accelerate the rise.

While only the gentlemen in the ivory towers of Wall Street know whether there will be another 'bear raid', we do not believe it will have more than a short-term success if it is launched.

It makes far more sense for such heavy weight traders to be ready to change any such 'bear raid' into a 'bull raid' on the fall and take the gold price up much higher than it is now. But will the regulators be happy with such market destructive games?

What we can say now is that the gold market does not appear to us to be likely to stay as tranquil as it has for the last few weeks/months for much longer!

Hold your gold in such a way that governments and banks can't seize it!

Visit: www.stockbridgeMgMt.com And Enquire @ admin@StockbridgeMgMt.com