While we wait for our Employment Report tomorrow, there is plenty of excitement overseas.

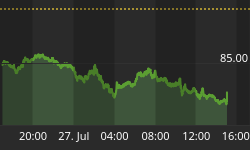

The dollar continued to strengthen today, with the dollar index reaching the highest level since the middle of last year (see chart, source Bloomberg).

As with the rest of the dollar's strengthening move, it was really not any of our own doing. The dollar is simply, and I suspect very temporarily, the best house in a bad neighborhood right now. In the UK, the Scots are about to vote for independence, or not, but it will be a close vote regardless. In Japan, the Yen is weakening again as the Bank of Japan continues to ease and Kuroda continues to jawbone against his currency.

In Europe this morning, the ECB surprised many observers by cutting its benchmark rate to the low, low rate of just 5 basis points (0.05%), and lowered the deposit rate to -0.2%...meaning that if a bank wants to leave money sitting at the ECB, it is forced to pay the ECB to hold it. A negative deposit rate is akin to the Fed setting interest on excess reserves at a negative figure, something that makes great sense if the point of quantitative easing is to get money into the economy. In the Fed's case, it turns out that the real point was to de-lever the banks forcibly, so it didn't care that the reserves were sitting inert, but in the ECB's case they would really like to see inflation higher (core inflation for the whole Eurozone is under 1%) so it is important that any increase in the balance sheet of the central bank is reflected in actual currency in circulation.

Right now, the negative deposit rate isn't so important since the ECB holds negligible deposits. But the negative deposit rate was step one; step two is to gin up the quantitative easing again. ECB President Draghi had promised several months ago to do so with 'targeted LTRO', and today he delivered by saying that the ECB has decided to begin TLTRO in October. The ECB will "purchase a broad portfolio of simple and transparent securities" even though some observers have noted that there aren't a lot of asset-backed securities in the market to buy (but trust Wall Street on this: if there is a buyer of a few hundred billion Euros' worth of such securities, those securities will be issued. Wall Street isn't good at everything, but they're darn good at finding ways to satisfy a motivated, huge buyer. (See "subprime MBS").

This is significant, as I said it was when Draghi first mentioned this back in June. It is significant if they follow through, and at least at this point it appears they mean to do so. Now, Europe still needs to fight against the dampening effect on money velocity that lower interest rates are having, but at least they recognize the need to get M2 money growth above the 2.7% y/y rate it is at presently (which is, itself, above the 1.9% rate of the year ended April). Money growth in Europe is currently the lowest in the world, and - surprise! - deflation is the biggest threat in Europe. Go figure.

How does this affect inflation in the US?

Changes in the global money supply contributes to a global inflation process that underpins inflation rates around the world. The best way to think about the fluctuations in exchange rates, with respect to inflation, is that they allocate global inflation between countries (or, alternatively, you can think of inflation as being "global" plus "idiosyncratic", where a country's idiosyncratic inflationary or disinflationary policies affect the domestic inflation rate and the exchange rate with other countries). So, the ECB's aggressive easing (when it happens) will have two main effects. First, it will tend to push up average inflation globally compared to what it would otherwise have been. Second, it will tend to weaken the Euro and strengthen the dollar so that inflation in Europe should rise relative to US inflation - all else being equal, which of course it is not.

With respect to this latter effect, I need to take pains to point out that it is a small effect, or rather than the relative movements in the currency need to be a lot bigger to be worth worrying about. A stronger dollar, in short, is not going to put much pressure on US inflation to be lower. The chart below (source: Enduring Investments) shows a proxy we use for core commodities inflation, ex-medical, against the broad trade-weighted dollar lagged 9 months.

You can see that core commodities respond broadly to the dollar's strength or weakness. A 5% rise (decline) in the dollar causes, nine months later, a 1% decline (rise) in core commodities inflation, ex-medical care commodities. Core ex-medical care commodities represents about 18% of the consumption basket, and the dollar's effect outside of that part of the basket is indeterminate at best, so we can say that a 5% rise in the dollar causes inflation to decline about 0.18%.

In short, don't waste a lot of time worrying that the 4% rise in the dollar this year will lead to deflation any time soon. Against that 18% of the consumption basket, we have 57% of the basket (core services) inflating at 2.6%, and over half of that consists of primary and owners' equivalent rents, which are rising at 3.3% and 2.7% respectively and have a lot of upward momentum. Unless the dollar shoots dramatically higher, it should not affect overall prices very much.

You can follow me @inflation_guy!

Enduring Investments is a registered investment adviser that specializes in solving inflation-related problems. Fill out the contact form at http://www.EnduringInvestments.com/contact and we will send you our latest Quarterly Inflation Outlook. And if you make sure to put your physical mailing address in the "comment" section of the contact form, we will also send you a copy of Michael Ashton's book "Maestro, My Ass!"