The following is part of Pivotal Events that was published for our subscribers October 16, 2014.

Signs Of The Times

On the FOMC minutes of October 8th, the Street claimed that the report was "Dovish" and markets soared. On the next day's Pivot we noted that the stock market couldn't go down until all of the shorts had been forced to cover. The push by the establishment seems to have accomplished that.

Not emphasized within the minutes was:

"Some financial developments that could undermine financial stability were noted, including a deterioration in leveraged lending standards, stretched stock market valuations, and compressed spreads."

Why try so hard on the "squeeze?

"It's been a painful week for Wall Street's biggest bond brokers. Primary dealers had the biggest short position on government notes at the beginning of the month since last year's taper tantrum in June 2013."

- Bloomberg, October 10

It has been worse this week and on Monday CNBC observed:

"Stock market fails to get an oversold bounce."

Taking out some support levels got us into our history files, especially when a TV spokesman observed that the stock market had hit some "air pockets".

"If a recession should threaten (it is not indicated at present), there is little doubt that the Federal Reserve System would take steps to check it."

- Harvard Economic Society, October 19, 1929

More reporting than dreaming was:

"Recall of Foreign Money Grows Heavier--All Europe Withdrawing Capital"

- Commercial and Financial Chronicle, October 21, 1929

Then there was the first use of the term mentioned above.

" 'Air pockets' (a phrase coined to denote a lack of bids for individual issues)."

- The Economist, November 2, 1929

Perspective

Our September 25th Pivot summed up our work on the previous few months with some important stages:

Exuberance:

The percent bears in dropping to only 13.3 had not been seen since 1987. The Monthly Upside Exhaustion reading registered in August and September hadn't been seen since just before the peak in 2000.

Divergence:

There were many, but the Small Caps (RUT) provided the best pattern and was updated on September 23rd.

Volatility:

While we observed that the VIX, itself, doesn't "do" volatility at its lows, it gave a Sequential Buy on August 22nd. On September 25 we noted that it broke above resistance at 15 and provided the alert. So far the high has been 31.

Resolution:

That the intense speculation would finally resolve to the downside was not in doubt. The question was when? We noted that the action had registered the most distinctive "Hindenburg Omen" since March 2000. This suggested sometime "soon". Then there are seasonal forces.

Consequences:

This section is an addition to our September 25th summary and this week has seen severe covering of suddenly unsupportable positions. Longs in crude, shorts in the bond future and longs in Greek bonds all took serious hits.

Forced liquidation in various games is becoming heavy but is not yet a panic. Will it end in a panic or will a panic be prevented by something "innovative" from the central banking crowd?

We will see, but the latter seems doubtful, as they would have to reverse deterioration in the credit markets and rally depressed commodity prices. Both immediately as in right now.

It is worth recalling that the original purpose of the Fed was to prevent financial crises because they caused recessions. The next few weeks will be interesting.

Stock Markets

Our review of the big NYSE average, the NYA concluded that the decline was equivalent to its action in November 2007, which was only a few weeks after that fateful peak.

On Monday's plunge the S&P took out the 200-Day ma, which is noteworthy.

The Oil Patch and base metal mining stocks have sold off a lot from their overbought condition in May and July, respectively.

Banks in Canada and the US have declined steeply since late September.

However, we now start to look for the oversold that will end the plunge and prompt a brief rally. The following table outlines the seasonality of some of the most important liquidations in financial history. The key pattern now is that they all occurred in the fall.

Within this, liquidation became very intense in the latter part of October. A brief bounce was followed by a test in November.

A tradable rally followed.

The ChartWorks is monitoring for the trade.

Bubble Conclusions: Seasonality

Currencies And Commodities

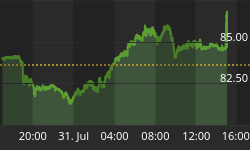

The key to recent dollar volatility has been reaching an impressive overbought and then rallying further. We had a target of 85 for the DX and when it got there we noted this possibility.

It was based upon the old saying that historical crashes "come out of oversold conditions".

We noticed this characteristic when the grains became oversold enough for a good trade. A brief and modest bounce was followed by a slide from 321 to 290 two weeks ago.

Similar action was recorded by crude on a decline into August, Brief rally then failure. The slide is becoming severe, which could be crude beginning the equivalent of the massive adjustment in natural gas pricing. This is not to say that crude's decline will be proportionate to the six-year plunge in gas from 15 to 2. But it will be important.

As part of the play, the Canadian dollar has declined to 88.24 and is attempting to stabilize.

Some weeks ago we mentioned that last year natural gas prices were depressed by the unusually cool summer. And then there was a good trade as the cool weather prevailed through the winter. This summer we suggested trying the trade and then got off it. It is still tempting, particularly as general liquidity problems ease.

Precious Metals

On precious metal stocks we have been expecting that the buying opportunity would appear in October, possibly towards the end of the month. This would occur during the ending phase of forced selling of stocks, lower-grade bonds and commodities.

Using the GDXJ, the Daily RSI slumped to 27 on October 3rd, which was enough to pop a rally from 31.28 to 34 last week. It has drifted down to 33.5 and the low needs a test, which could happen over the next week or so. This would fit with this phase of diminishing overall liquidity.

Our "get-me-in-or-out" monitor is the action in the silver/gold ratio. On the "Rotation" rally that got us in in December when the Daily RSI was down to 30. The rally in gold stock was outstanding and we took money off the table in March and again in June. The first swing in the GDXJ was from 28 to 46. The next swing was from 32 to 46 in June.

On that one, the RSI zoomed to 84 which indicated excessive speculation.

The RSI plunged to only 18 earlier in the month, which indicated that the gold sector was very oversold.

October was likely to be the month in which to begin accumulation and the sector needs to test the lows.

Ampersand

In the other assets department I have made some portfolio changes. Two of the more expensive Alfa Romeos have been sold. Over the past few years the price advances for older sports cars has been outstanding. So the 1962 Spider and the 1963 Sprint Coupe are sadly gone to their new owner in Oregon.

The 1967 Alfa Giulia Super is a sports sedan and still at home. It is easy to get in and out of and a lot of fun to drive.

Gold/Commodities

- This is a proxy for gold's real price.

- Note the bear market from 2011 to June of this year.

- It needed to break above 3.90 to confirm the uptrend. This happened at the end of September and it is at 4.10.

- This is now a new bull market for gold's real price and is becoming very constructive for the industry.

Perspective

September 19: S&P Peak 2010

"The U.S. stock market's bears have gone into hibernation. With no end in sight to a rally now in its fifth year, once pessimistic Wall Street forecasters are espousing rosier views."

- Wall Street Journal, September 15.

October 15: S&P at 1820

In any century it has been prudent to use safety glasses.

Link to Bob Hoye interview on TalkDigitalNetwork.com: http://talkdigitalnetwork.com/2014/10/volatility-generates-volatility