The Dow and S&P 500 closed a seventh straight weekly advance on Friday as a better-than-expected jobs report indicated strong economic growth, but perhaps to the point where interest rates could rise sooner than previously anticipated. For the week, the Dow rose 0.7 percent and the S&P rose 0.4 percent. It was the seventh straight weekly gain, a streak not seen in a year for both. The Nasdaq fell 0.2 percent on the week. As seen in the graph below treasury bonds have performed at stratospheric levels year-to-date, as interest rates remain extremely low. Conversely low rates have been catastrophic for gold mining stocks.

The Bullish Index is a popular market "breadth" indicator used to gauge the internal strength/weakness of the market. It is the number of stocks in an index (or sector) that have point & figure buy signals relative to the total number of stocks that comprise the index (or sector). So essentially it is the percentage of stocks that have buy signals. Like many of the market internal indicators, it is used both to confirm a move in the market and as a non-confirmation and therefore divergence indication. If the market is strong and moving up, the BPI should also be moving up as more and more stocks make the "buy list." When the market moves higher, the BPI should also move higher to confirm the market's strength. As highlighted in the chart below, the S&P 500 BPI has reached an extremely overbought level, which is why the index has been consolidating the past few weeks. Also noted momentum is trying to turn bearish.

A few weeks ago treasury prices jumped as result of a historical day in the bond market when there were all-time lows in 10-year yields simultaneously in France, Germany, Italy, Spain, Netherland, Portugal, Switzerland and Japan. In the updated chart below you can see treasuries dropped last week and the dollar returned to its lofty levels, which drove down precious metal prices after gold started the month gushing higher.

Market Outlook

The Stock Trader's Almanac report over the course of this year, they compared 2014 to past midterm years and more specifically midterm years that were also sixth years of presidential terms. Whether you are a believer or not in seasonal patterns and analysis, it is difficult to ignore the fact that DJIA and S&P 500 have tracked the Sixth Years seasonal pattern rather well in 2014. January proved to be a tough month, but from the beginning of February into the third quarter, DJIA and S&P 500 both moved steadily higher just as they had both done in previous Sixth Years. However, rather than peaking early in the third quarter, they continued higher until mid-September before crumbling into mid-October. And from their October lows, DJIA and S&P 500 rocketed higher, just as the Sixth Year pattern does. Now the Sixth Year pattern is suggesting a brief period of consolidation before the market resumes its march higher into yearend. This pause is likely to last until mid-December and DJIA and S&P 500 could finish the month around 2% higher than they are currently trading.

Last week we said December is the number one S&P 500 month and second best for DJIA since 1950, averaging gains of 1.7% on each index. It's also the top Russell 1000 and Russell 2000 (1979) month and second best for NASDAQ (1971). Rarely does the market fall precipitously in December. In midterm years, December's rankings slip modestly, but average gains remain inline. The "January Effect" of small-cap outperformance starts early in mid-December. Wall Street's only "Free Lunch" of distressed small- and micro-cap stocks making new 52-week lows on December Triple-Witching Friday will be served before the opening bell on December 22. Santa's Rally begins on Wednesday December 24 and lasts until the second trading day of the New Year. S&P has averaged gains of 1.5% since 1969. In years when Santa Claus did not come to Wall Street, bear markets or sizable corrections have often materialized in the coming year.

As mentioned last week, investors are really enthusiastic about the U.S. economy as smaller capitalization indexes like the Russell 2000 and Midcap 400 continue to lead the stock market over their larger cap brethren. Even more telling is that Dow Transport and Real Estate are the hottest asset classes in the fourth-quarter as these sectors are dependent on domestic economy performance.

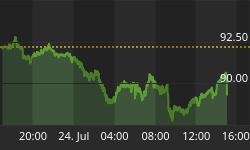

The updated chart highlights the Momentum Factor ETF (MTUM) uptrend line that initiated in the middle of November. Until there is a confirmed break below the uptrend line we expect to see stock prices continuing to climb higher for the rest of the year.

Wall Street's fear gauge, the CBOE Volatility Index (VIX) dipped sharply on Friday after a surprisingly strong jobs report, and there was a surge in put activity in the index's options. In the updated CBOE Volatility Index (VIX) graph below the index dropped to its lowest level since August as the S&P 500 index once again reached new all-time highs. The VIX can be expected to bounce from the current low point, but unless the stock market pulls back significantly any upward move in the VIX will be limited through year-end.

The current American Association of Individual Investor Survey (AAII) survey results approximate long term averages which signals a predominately neutral trend over the next few weeks. Retail investors backed off their excessively bullish percentage from a few weeks ago which significantly reduces the probability of stock prices falling. The best bet is price consolidation before the markets finishes with a year-end spurt.

Third-quarter National Association of Active Investment Managers (NAAIM) exposure index averaged 71.09. Last week the NAAIM exposure index was 86.78%, and the current week's exposure is 86.06%. The current exposure remains the highest since the middle of the year as investment managers are buying high performing shares to put on the books for year-end window dressing. Note that exposure still is not as high as this time last year and if investment managers decide to get fully invested this will send the market soaring at year-end.

Trading Strategy

As displayed in the chart below, over the past thirty days cyclical and healthcare stocks are the leading S&P sectors. Historically, cyclical stocks begin picking up steam at this time of year and of course, healthcare shares benefit from Obamacare regulations forcing consumers to purchase health insurance. Energy stocks rebounded last week, but we need confirmation before betting this sector is starting to recover. Since we are beginning what is termed "the best six-months" of the trading year, now is a probably a good time to invest in shares of hot stocks in the best performing sectors.

Regards,