From the HRA Journal: Issue 224 by Eric Coffin, December 2, 2014

Volumes remain high in the bullion markets and volatility is higher if anything. We just had one of the biggest up days in a couple of years but, overall, gold hasn't moved much higher. That won't change until we get a number of up days in a row rather than the pendulum swing we've seen lately. If India's reduced import restrictions lead to the import volumes we saw before 2013 and China's demand holds up we may finally get the change in trend we've been hoping for. I think the odds of that are good though its going to take time to evolve.

Traders used the fall in oil prices to sell commodities across the board. That would make sense if the main cause was a drop in demand. There has been some of that but the energy sector is really a victim of it own success. Increased supply is the real culprit. It doesn't make sense to sell most metals due to falling oil prices any more than it would have made sense to sell oil when iron ore prices dropped under the weight of oversupply.

The drop in oil will act as a stimulus for most economies, putting a little extra in consumers' pockets. It's not a huge thing but it might give growth rates in the lagging economies of Europe and Japan a small boost. That's better than nothing which sums up what politicians and central bankers in those areas have been able to accomplish on their own. We'll take all the help we can get.

As I expected, OPEC decided it's time to play "chicken" with non-OPEC oil producers, specifically shale oil producers in the US. As I noted a month or so ago OPEC clearly wants their market share back. They have reason to worry.

The market is catching up to the idea that production growth in the US is fast enough to present a new paradigm. Ominously for OPEC the US is not the only place with the right geology. There are several areas in central and Eastern Europe and Asia that could generate significant production growth if enough capital was applied to them.

There are regulatory hurdles to be sure. Fracking has become a four letter word but there are many developing countries that have oil to thank for perennial current account deficits. Getting even a portion of their demand sourced locally would take a lot of pressure off government coffers.

OPEC knows all this and knows too that its ability to manage the market is slipping away. The spread of fracking and horizontal drilling technologies is accelerating. Although the higher cost producers in the club aren't happy about it the more powerful Middle East OPEC members feel it's now or never if they want to retain price control.

The OPEC announcement was a blunt one and the group's spokesman made it clear there was no intent to revisit the decision before the next scheduled meeting in six months.

The gauntlet has been thrown down and now we wait to see who blinks first. The chart on page one starkly illustrates how many traders were surprised by the move. Many thought OPEC would cut production. Oil was sold and sold hard after the announcement taking the price to levels not seen since 2009.

A 10% drop in one day is a massive move for any commodity but prices could still go lower. Current over production is estimated at two million barrels per day. That much and more just became uneconomic but many producers' hedge and crude inventories are fairly high.

This could easily take a year or two to play out. Many large US producers insist they are close to fully hedged. That might be true. Oilmen seemed more surprised than anyone when oil went above $100/bbl early this year. They knew the market was getting oversupplied. If they did hedge sufficiently they could withstand this price drop for a while.

Prior to the price drop it was estimated that US production would rise by another 0.5 to 1 million barrels/day next year from the current rate of 9 million barrels/day. The largest new shale production areas like the Bakken claim production costs of less than $50/bbl. Companies in the midst of tying in new production will continue. The oil price drop may not stop, much less reverse, production growth for at least a few months, maybe longer.

So what does a one or two year run of $60-70 oil mean? It's a big positive for the world economy even if high cost producers get stung. A drop that large doesn't, strictly speaking, change discretionary income for consumers but it certainly redirects some of it. Money not spent at the gas pump can go to better uses like Christmas presents, baby shoes or mojitos at the bar.

Wall St takes the oil price drop as a good thing. No surprise there. Wall St takes everything as a good thing these days. It should be good for retailers (other than gas pumps), great for airlines and other heavy energy users.

It's not as good as it used to be though. The positive impact of a $10/bbl drop in oil to the US may be as little as a quarter of what it once was. That is because of the US's large domestic production. Falling oil prices don't have as much impact on imports and the current account as they used to and there will be a domestic cost in terms of oil sector jobs if prices stay low. The shale boom has been a big contributor to employment gains in the US recently and, unlike most recent employment gains, these are high paying jobs.

The market's opinion of oil's fall can also be seen in the US Dollar Index chart below. It had a fairly large one day move but stayed within the November trading range. It could break higher now though I think traders, as usual, are oversimplifying things.

Falling energy prices have the biggest positive impact on countries with the least domestic production. That list includes Japan, the Eurozone, China and India.

The percentage change in prices to consumers will be less where there are a lot of levies and taxes on top of prices (Europe and Japan) or where there are government price subsidies (most developing countries) though the fall in market prices will help cut government deficits in those countries.

In short, cheaper oil should be positive in exactly the places that really need it like Japan and Europe though the average consumer doesn't drive as much as North Americans do. It may increase consumer spending in Japan and the Eurozone and won't have the negative impact on domestic jobs that oil producers might see.

One other effect falling oil would have which would explain the immediate reaction in the gold market (if you're a simpleton) is it should also reduce inflation rates in most developed countries. That isn't a positive under current conditions. Central bankers are already freaked out about how low inflation is, especially in Europe. Keep in mind that lower energy prices won't change "core" rates or GDP deflators much which are the preferred measure for central bankers. Nonetheless, it will make lifting inflation to the 2%+ targets most G7 central bankers have a lot tougher.

In theory at least that may mean it takes longer for the US Fed and ECB to raise rates. That should be good for gold and other metals. If Japan and Europe get a bigger boost from cheap oil it might lead to a bit of strengthening in the Yen and Euro--if the growth chasm between them and the US narrows a bit.

India Surprises. Switzerland, Not So Much.

Just before this issue was completed there was news out of New Delhi that India's 80:20 gold import rule was being scrapped. This was a huge surprise to the market.

It was no secret the India's central bank and economic ministry were not happy about the way Indian gold imports have skyrocketed in the past 2-3 months in particular. Most expected rules to be toughened.

There was little immediate reaction because it came on a day Comex closed early and electronic markets were closed. I think a lot of traders didn't even know about the change before the markets closed Friday.

The seeming confusion even among finance department bureaucrats has many wondering if there isn't another announcement coming. Perhaps the 80:20 rule gets replaced with something more permanent like an annual quota. That might or might not be more restrictive.

I don't know if there is something else coming either of course. It seems very odd that restrictions were loosened in a terse announcement on late Friday afternoon. It may be driven indirectly by the fall in oil prices. Finance officials don't care about gold per se. They care about how gold imports add to the current account deficit. Oil imports are an even bigger factor.

Assuming oil prices do stay in the $60-70 range India's current account should get an annual boost of about $50 billion due to savings on oil imports. That saving is more than the entire cost of gold imports. It may be the Modi government decided to make a politically populist change to gold rules because oil prices have given the finance ministry a lot of wiggle room.

The 10% import duty on gold has not been removed. That will be a drag on demand but if jewelers can get whatever gold supplies they need the local premium on gold prices should drop which will make purchases more attractive. Indian imports have already moved higher so we may not see a big immediate impact.

If Indian gold imports move back to pre-2013 levels 300 tonnes would be added to market demand annually. Indian buyers are price sensitive; without tariffs and the 80:20 rule 2013 demand would have been several hundred tonnes higher just as it was in China. A return to demand levels comparable to China would be a huge boost for the gold market.

I won't spend much time on the Swiss referendum since it was rejected by a wide margin. The voting margin was wide enough that I don't expect to see the gold referendum reappear soon.

The party that championed the gold referendum is a populist one. There are gold bugs in its ranks but I think there was more to this than just gold. I had the sense that the referendum's backers also saw it as a way to break the Swiss Franc's peg to the Euro, currently set at 1.2 SFr:1 €.

Switzerland has always had a strong currency, in part because it was partially gold backed until 1999. Since then the Swiss central bank has been the largest sovereign seller in the gold market.

The chart above shows the size of various central bank balance sheets as a percentage of their county's GDP. Most of you will be surprised to learn the balance sheet that expanded the most is that of the conservative frugal Swiss. In terms of balance sheet compared to GDP it's not even a close race. The SCB's ratio is twice as big as Japan's.

Why is that? Bailing out banks? Eating bad real estate loans or holding rates down to encourage employment? Nope. It's all about keeping the SFr from appreciating. The bank instituted the Euro peg as a "temporary" measure in 2011. It prints Swiss Francs out of thin air and uses them to buy Euros or Euro denominated debt.

The bank feels compelled to keep the SFr from rising to help protect exporters. It won't be enough. Switzerland has run deficits on goods trade for decades. Switzerland has very high costs of living. Holding the Franc down isn't helping the average person on the street. Letting the Franc appreciate would lead to cheaper imports for them. I guess that isn't who the bank answers to. I don't see how a rising currency would hurt financial transactions either. Money moved into Switzerland would gain currency appreciation on top of financial returns.

Unless the Eurozone gets its act together the Swiss National Bank will have to just keep buying Euros. I don't think anyone was betting on the referendum passing but if they were we might see a few Euro shorts unwound.

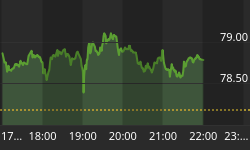

All this brings us finally to the latest look at the gold market. It's all over the map. Gold got smashed right along with oil but something changed when gold fell to $1140, just as it did almost a month ago. The market turned hard. Much harder in fact than can be explained by changes in the USD or oil. It was a repeat of last month's Freaky Fridays on a grander scale. Buying was heavy and constant through Sunday night and Monday's day session.

The bounce in oil and (small) fall in the USD certainly played a part and we may have been getting a delayed reaction to India's announcement. Whatever it was it generated another outside day on heavy volume and the largest one day upward move in at least a couple of years.

There was a lot of negative gold commentary on the weekend after the Swiss vote. Much of it was from technical analysts and part time gold market watchers. They may have been short and caught out. Notwithstanding the initial drop on Sunday I don't believe any serious gold market participants were positioned for a win in the Swiss referendum. The polls were heavily against it for a month.

Oil could grind lower but it's a positive for non-US G7 economies especially. If the drop in oil helps the advanced economies--and it should--that could help put a floor under industrial metals, currencies and precious metals too.

The last chart in this article is in some ways the most interesting. Gold lease rates have been climbing rapidly and that climb accelerated after oil prices collapsed. The Lease yield curve has been upended and 30 day rates have increased 250% in a month. Likewise, the GOFO rate has turned even more negative. Both of these measures indicate extreme tightness in the physical market and both are near historic levels. This doesn't jibe with a falling gold price. Historically, rapidly rising least rates or deeply negative GOFO rates precede larger than average price increases. Physical market measures simply do not point to price weakness going forward. I don't see compelling reasons for new lows in gold but its all sentiment driven right now.

The next US payroll report comes out late this week. That has created big price swings lately. Gold got above its 50 day moving average for the first time in four months and it got there on massive volume. That looks significant and may finally be a trend change if a blockbuster payroll report doesn't knock it back.

None of this helped the venture Index but this time the selling is mainly oil and gas stocks. We are still seeing tax loss selling but that should dry up over the next few sessions. I want to see GDX get above its November or, better yet, October high. If we can get there this month 2015 might finally be the decent year resource trader are so overdue for.