In my Jan. Model Bond Portfolio for Moderate Risk investors, I recommended maintaining a 25% position of one's overall stock/bond portfolio in bonds, the same percentage I recommended for cash.

Since cash held in money markets or perhaps CDs promises to return hardly anything (let's estimate from 1/4%, to say, 1% after interest rates likely increase this year), this equality of bonds and cash allocations means we are not currently (nor were we last year) highly positively predisposed toward bonds.

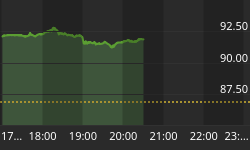

While it is still likely to be the case that some types of bond funds will do significantly better than cash, overall, it appears we have already seen a topping out of bonds in early February.

From comments gleaned recently from Fed officials, including Fed Chairwoman Yellen, it appeared likely in January that the balance was tipping more and more toward the beginning of a period of slowly increasing rates starting this summer. Then, on Feb. 18th, the Fed released a statement perhaps designed to confuse everyone, or perhaps just reflecting their own indecision. But the message seems clear: Higher interest rates are coming, although the Fed doesn't want to pre-commit to exactly which month this will happen: early summer, late summer, or perhaps early this fall.

It should be realized, however, that the bond market (as well as the stock market) typically moves ahead of actual events in anticipation of what is perceived as highly likely. Therefore, it should really make little difference when "liftoff" comes, only that it is coming quite soon.

Nearly all signs point to a US economy that is showing enough strength that rates hovering just about 0% are no longer justified. True, conditions elsewhere in the world are anything but strong with even some whiffs of deflation, which is just the opposite of where central banks want things to go. But that shouldn't mean that the US is on the doorstep of the same kind of trouble.

While the rest of the world should gradually outgrow its problems, the US economy should easily remain ahead of the pack. This means that while, low, or even actually negative, interest can prevail elsewhere, we are perhaps a year or two ahead in the so-called interest rate cycle in which interest rates begin to rise as the economy strengthens.

As many readers will recognize, the US has also led the world in keeping interest rates artificially low after the economic crisis of more than a half decade ago. The purpose of the Fed's actions was to ensure growth, presumably during an extended period when the economy needed all the help it could get. Such extreme stimulation likely did help the economy pull out of its doldrums to some degree and proved particularly a boom to stocks which thrive on low interest rates. It also helped move investors into bonds given hardly any return on money markets/CDs and assurance there was little chance of any surprise rate increases to hurt bond prices.

But Fed officials are now seeing that the need for such extreme stimulation of the economy has clearly past. While they are still a little worried about low inflation, Yellen has made clear that the majority view is it likely will be short-term in nature. While no one can be sure, even gas prices, one of the currently most visible signs of low inflation, appear to have reached bottom recently and are again starting to rise.

Assuming market-determined interest rates do start rising in the months ahead and bond prices fall in anticipation, bond fund investors could be in for some rough sledding. Already returns have been lackluster over the past few months and we expect that trend to continue.

Investors should be best served by favoring shorter maturity bonds or even cash in the event that bond fund returns possibly go negative. Of course, another advantage of holding cash instead of bonds is that it gives one a pool of assets available to begin investing again more aggressively in bonds (or stocks) once conditions become more favorable. In the case of bonds, we do not expect that to be the case for quite a while.