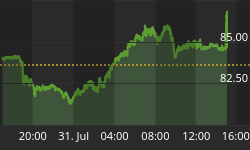

The Shanghai Composite rallied 10% this week, enjoying the "biggest two-day rebound since 2008." Friday saw Germany's DAX surge 2.9%. French, Spanish and Italian equities rallied about 3%. European periphery bond yields dropped (some). The S&P500 advanced 1.2%. It was, however, another rocky week for commodities.

Global markets this week approached the edge - then recoiled, as they tend to do. Over recent years it's become the typical pattern. Wait long enough and market stress is met with whatever desperate policy response it takes at that moment. Officials in China moved aggressively to adopt their belligerent brand of "whatever it makes" central market control. Crazy stuff. And as market participants expected, the Game of Chicken saw the Greeks and Europeans eventually cave to market pressure. Markets win again. Long live the king.

So has this been just another blip presenting buying opportunities - or something much more serious? To be sure, the situations in China and Greece continue to fascinate. We're living history real time 24/7.

My view is that China and Greece are both Broken. But that certainly won't stop the manic markets from their short-term focus and speculative impulses. Rewards have been too reliable for too long. There's nothing like a bout of hedging and shorting to get market operators salivating at the prospect of an abrupt reversal of hedges and short squeeze. Still, we can't take our focus off what is unfolding in the intermediate- and longer-term.

No doubt about it: markets will do what the markets will do. The optimists - who have accumulated great financial power over the past six years - are programmed to trust that policymakers have things well under control. The possibility that this is all one historic Bubble that could now blow up at any time is wacko.

On a weekly basis, I attempt to place developments into context. I see the global government finance Bubble as the grand finale of a historic period of serial Bubbles spanning several decades. This is an extraordinarily dangerous period - financially, economically, socially and geopolitically. The Bubble has made it to the heart of the global monetary system, to the very foundation of "money" and Credit: to central bank "money" and government debt. Virtually unlimited demand for this "money" has ensured unprecedented over-issuance. Governments everywhere are desperate to contain monetary disorder that is now escalating out of control.

Massive monetary inflation has inflated precarious securities and asset Bubbles on a global basis. It has spurred unmatched wealth redistribution and inequality. And the more folks come to appreciate the permanence of this "New Normal," the deeper the acrimony, discontent and geopolitical risk. And the bigger and more vulnerable Bubbles inflate, the greater the impetus for additional monetary inflation and only greater government control. China has built on lessons learned from the West.

I am convinced that the global government finance Bubble has been pierced. This helps explain why Greece and China (as well as Puerto Rico) have erupted simultaneously. In Europe, ECB QE has inflated bond Bubbles including those in Portugal, Spain, Italy and France, only to bypass a desperate Greece. In China, massive fiscal and monetary stimulus worked chiefly to inflate a historic stock market Bubble. In Europe, Asia and the Americas, efforts to sustain financial Bubbles only exacerbate the divergence between inflating securities markets and deteriorating fundamental prospects. At this point, a crisis of confidence in government finance and policymaking is unavoidable.

Meanwhile, markets rejoice at the notion of the Chinese resorting to blatant inflationism. The ECB will surely pick up the pace of QE. The Japanese now have an excuse to extend their reckless QE program that chiefly inflates speculation. At the Fed, a tightening of policies (not a meaningless little 25bps rate bump) is pushed out so far as to be invisible. Many global equities markets remain not far off record levels. So why are commodities so depressed?

It will be an interesting weekend in Athens, Brussels and Europe more generally. The press is alive with articles and analysis detailing the dual capitulation of nemeses Tsipras and Merkel. There may be an agreement this weekend. There will, however, be no resolution to the "Greek" crisis anytime soon.

Greece is Broken. Confidence has been shattered. The banking system is bust. So there will simply be no way to quickly bounce back from capital controls and having the banking system shuttered for a couple weeks. Importantly, the very real possibility of the return of the drachma cannot be erased from memory. "Money" wants out - out of Greek banks, out of Greek investment, out of the Greek economy and out of Greece generally. Devoid of confidence and a functioning banking system, the Greek economy is in a death spiral. It will now take a tremendous amount of new finance to keep Greece afloat. Going forward, the lurking specter of the drachma will severely hamstring recovery.

The IMF appreciates that Greece today needs a huge new assistance program. But they also have rules. Greece has already defaulted to the IMF, so new "money" will not be forthcoming from the International Monetary Fund. The ECB also (supposedly) has rules. And I suspect Mario Draghi would even agree with Bundesbank President Jens Weidmann and others: At this point Greece is hopelessly bust. Sitting on tens of billions of suspect Greece obligations already, the ECB will tread carefully here as well. OK, so who's the sucker at the table?

I've always envisioned there'd come a point when the Germans had been pushed to far. Backlash would inevitably ensue. Festering anger would erupt, in unGerman-like fashion. Thus far, the "mad as hell..." Greek people have spoken. As for Germany, they have been blanketed with vitriol and unfair criticism. Far too ofter they have become the convenient scapegoat. Will German citizens now ensure that their voices be heard?

German politics is entering a period of uncharacteristic uncertainty. It appears that Chancellor Merkel, finance minister Schaeuble and other key officials now believe Grexit is necessary and inevitable. But under what circumstances will they finally bite the bullet? Seemingly the entire world is now pressuring the continuation of a course German leadership views as destined for complete failure.

Of course, the Germans don't trust that the Greeks will suddenly start living by agreements, especially after the public referendum and with an economy in collapse. They're appalled at the contempt Greek politicians and citizens have toward their lenders. The Germans also see political risks erupting throughout Europe. To be sure, this euro currency experiment has become a colossal problem.

The Greek people have shouted out their utter disdain for the status quo - a backdrop that today ensures a period of only greater hardship and social upheaval. It's difficult for me to disagree with what I believe is the current view of German leadership: at this point, additional assistance should be marshaled to assist the transition of Greece outside of the euro.

This primary issue is not so-called "austerity." It's wrong and unproductive to scapegoat the Germans. The critical issue is disregarded: by now it's clear that the dysfunctional Greek economy is not sustainable inside the euro zone. The harsh reality is that as part of the euro monetary regime both the Greek economy and banking system are financial black holes. It's the wrong currency for that economic structure: throw "money" in and it leaks right out. Who is willing to keep writing these checks? Who can afford to?

Greek dislocation will continue to foster various major risks. Yet the bursting Chinese Bubble foments more dangerous global financial, economic, market and geopolitical risks.

July 8 - Wall Street Journal (Andrew Brown): "Far more than simply a market crisis, the turmoil on the Shanghai Stock Exchange is viewed by China's leadership as a potential security threat to the regime. That helps explain the barrage of measures unleashed by financial authorities to counter a sudden market downturn that threatened to shake public confidence in the government. In that sense, the unprecedented rescue moves, including a multibillion-dollar fund set up by Chinese brokerages at the government's behest to buy blue chips, is a preview of what's to come following the passage last week of a national-security law that massively expands the definition of threats to the state to cover almost every aspect of domestic life, including 'financial risk,' as well as international affairs. The law explicitly states that economic security is the foundation of national security."

July 10 - Financial Times (James Kynge): "On Sunday, the new graduates of Tsinghua University are set to gather in their smartest attire to celebrate degrees from one of China's most prestigious institutions, a place that has fostered generations of political leaders. Just after the ceremony starts -- according to a written agenda -- the graduates must 'follow the instruction and shout loudly the slogan, 'revive the A shares, benefit the people; revive the A shares, benefit the people'.' To outsiders, this may seem a curious sentiment with which to send China's best and brightest forward into their careers. More commonly, the tropes of patriotic education are concerned with issues such as national unity and strength, socialist ideology, the recapturing of China's past glories and washing away a century of shame inflicted by imperialist Japan and western powers. But the elevation of A shares into this rarefied pantheon of national priorities hints at the centrality of the battle that Beijing has joined to restore calm to its slumping stock markets and, in the process, revive its own credibility. This is because the A-share rout risks something much bigger than lost investments; the Communist party's basic definition of how power and the people are supposed to interact is also in jeopardy."

I've expected the bursting of the Chinese Bubble to be "frightening." It's commenced. I never really contemplated things would quickly turn so bizarre. "Revive the A shares, benefit the people." Investigating "malicious short selling." The banning of selling by large holders and company insiders. Forcing institutions to buy. Blaming rumor-mongering and foreign meddling. Media gag orders against negative reporting. Widespread trading halts and illiquidity. And the bear market is barely underway... So much in China is Broken.

"The bloom is off the rose," as they say. Perhaps Beijing can restore some semblance of domestic confidence in Chinese equities. Tall order. But I fully expect foreigners will be looking to get out. As a foreign shareholder, would I trust Chinese communist officials to protect my rights and financial interests? Going forward, should we expect a focus on the interests of shareholders or the leadership's political interests and fixation on global power? While the crowd ponders buying the dip, I increasingly question whether China at this point is even "investable"?''

Some of the reporting is reminiscent of the initial subprime eruption. The general expectation is that stock market losses won't have a significant impact on consumer spending or the overall Chinese economy. Only a small part of the population will be impacted. The government will protect against broader economic effects.

From my perspective, the key issue is the impact the stock market dislocation will have on the broader Chinese Credit Bubble. While very few appreciated it at the time, subprime amounted to the initial piercing of the mortgage finance Bubble. It represented the catalyst for a mortgage Credit tightening, escalating risk aversion, de-leveraging and a self-reinforcing general tightening of Financial Conditions. There was ebb and flow, repeated policy responses and bouts of wild volatility. Confidence proved resilient longer than I expected, with everyone somehow remaining oblivious to the ramifications of the bursting of a major financial Bubble.

Prior to recent tumult, there were already serious cracks in Chinese Credit. Housing Credit had slowed sharply, while commodities related Credit issues were also likely taking a toll. The government's reflationary stock market gambit has been instrumental in sustaining rapid system Credit growth - massive ongoing Credit expansion required to keep a highly maladjusted and unbalanced economy levitated. With equities market Credit contracting, I expect a forthcoming huge issuance of government debt in the name of "system stability."

I've seen a couple analysts question what China's response to its faltering stock market Bubble means in terms of the ascendancy of the renminbi to an international "reserve currency." This is an extremely important issue, although I'll come at it from a somewhat different perspective: What do cracks in the Chinese Credit Bubble, the bursting of China's stock Bubble and their heavy-handed and bizarre responses mean to the general stability of the Chinese currency?

I do not believe one can overstate the vital importance of the stable renminbi link to the U.S. dollar. I have posited that this "peg on steroids" has incentivized an enormous flood of "hot money" into China and, more specifically, into high-yield Chinese debt instruments. It is this massive speculative "carry trade" that has Chinese officials so jittery. It was this "hot money" Bubble that had officials backtracking from their 2014 managed currency devaluation. And it was the combination of faltering apartment and "hot money" Bubbles that was behind policymakers rolling the dice on the reflationary wonders of the stock market (they saw it work in the U.S.!) It could all come crashing down.

The renminbi began the week at 6.2055 to the U.S. dollar, right where it ended 2014. China's currency ended the week down a meager 0.06% to 6.2094. In spite of all the market tumult and uncertainty, the renminbi peg to the dollar has been solid as a big boulder. So are we to believe that Chinese officials can control the stock market, control their Credit system, control the economy, control the media and "foreign meddling", control financial flows, control speculation and, as well, control the currency peg to the dollar? I know, I know: they have control over $3.7 TN of international currency reserves. I've always believed this reserve position was much more vulnerable to disorderly "hot money" flight than commonly perceived. We may yet find out.

Throughout their historic boom, the Chinese have bent all kind of "rules" - economic, financial and otherwise. Can they continue to flout the fundamental rule that economic, financial and market instability spurs currency volatility and vulnerability?

I have posited that a proliferation of global currency "carry trades" (borrowing/leveraging in devaluing currencies to speculate in higher-yielding instruments in other currencies) is the unappreciated key source of speculative finance helping to fuel the global government finance Bubble. And for the most part, to this point currency markets have remained extraordinarily orderly and predictable. Draghi has orchestrated an orderly devaluation in the euro, essentially granting free "money" for those borrowing/shorting the euro to finance securities purchases elsewhere. Kuroda is going on three years of QE Fest, devaluing the yen and fomenting what I believe is one of history's great speculative plays ("yen carry trade"). The Chinese have certainly done their part, with their currency peg to the dollar ensuring easy speculative profits to anyone willing to short the dollar, yen or euro and use the proceeds to leverage in high-yielding Chinese Credit instruments and securities.

The euro is vulnerable to Grexit. The crowded euro short has as well shown susceptibility to squeezes. The yen this week again indicated potentially robust demand in the event of a bout of de-risking/de-leveraging. The yen gained a quick 1.5% against the dollar during Wednesday's nervous trading. At this point, no one is questioning China's commitment to its currency peg. But they sure have their fingers in a number of leaky dikes.

I question whether currency markets are about to enter a period of acute volatility. Could they crack? It's been awhile since the last episode of serious currency market tumult. I suspect a tremendous amount of "carry trade" leverage has accumulated since then.

For the Week:

The S&P500 was unchanged (up 0.9% y-t-d), and the Dow added 0.2% (down 0.4%). The Utilities fell 2.2% (down 9.5%). The Banks dipped 0.8% (up 3.4%), and the Broker/Dealers slipped 0.2% (up 7.4%). The Transports rallied 1.0% (down 10.3%). The S&P 400 Midcap index was little changed (up 3.5%), while the small cap Russell 2000 added 0.3% (up 3.9%). The Nasdaq100 declined 0.3% (up 4.3%), and the Morgan Stanley High Tech index fell 0.6% (down 0.5%). The Semiconductors were hit for 3.9% (down 4.1%). The Biotechs gained 0.8% (up 21.4%). With bullion down another $5, the HUI gold index sank 4.8% (down 13.6%).

Three-month Treasury bill rates ended the week at a basis point. Two-year government yields added one basis point to 0.64% (down 3bps y-t-d). Five-year T-note yields rose three bps to 1.66% (up one basis point). Ten-year Treasury yields increased two bps to 2.40% (up 23bps). Long bond yields were unchanged at 3.19% (up 44bps).

Greek 10-year yields sank 109 bps to 12.92% (up 318bps y-t-d). Ten-year Portuguese yields fell 10 bps to 2.81% (up 19bps). Italian 10-yr yields dropped 11 bps to 2.13% (up 24bps). Spain's 10-year yields declined eight bps to 2.12% (up 51bps). German bund yields jumped 10 bps to 0.89% (up 35bps). French yields rose four bps to 1.28% (up 45bps). The French to German 10-year bond spread narrowed six bps to 39 bps. U.K. 10-year gilt yields gained eight bps to 2.08% (up 33bps).

Japan's Nikkei equities index was hit 3.7% (up 13.4% y-t-d). Japanese 10-year "JGB" yields declined three bps to 0.44% (up 12bps y-t-d). The German DAX equities index recovered 2.3% (up 15.4%). Spain's IBEX 35 equities index rallied 2.4% (up 7.4%). Italy's FTSE MIB index gained 1.9% (up 20.6%). Emerging equities were mixed. Brazil's Bovespa index was little changed (up 5.3%). Mexico's Bolsa slipped 0.3% (up 4.1%). South Korea's Kospi index sank 3.5% (up 6.0%). India's Sensex equities index lost 1.5% (up 0.6%). China's Shanghai Exchange rallied 10.2% (up 25.6%). Turkey's Borsa Istanbul National 100 index rallied 1.9% (down 3.4%). Russia's MICEX equities index declined 0.5% (up 16.3%).

Junk funds this week saw inflows of $55 million (from Lipper).

Freddie Mac 30-year fixed mortgage rates declined four bps to 4.04% (up 17bps y-t-d). Fifteen-year rates fell four bps to 3.20% (up 5bps). One-year ARM rates slipped two bps to 2.50% (up 10bps). Bankrate's survey of jumbo mortgage borrowing costs had 30-yr fixed rates down five bps to 4.14% (down 14bps).

Federal Reserve Credit last week added $1.2bn to $4.442 TN. Over the past year, Fed Credit inflated $105bn, or 2.4%. Fed Credit inflated $1.631 TN, or 58%, over the past 139 weeks. Elsewhere, Fed holdings for foreign owners of Treasury, Agency Debt dropped $11.5bn last week to $3.367 TN. "Custody holdings" were up $74bn y-t-d.

M2 (narrow) "money" supply rose $19.8bn to a record $12.026 TN. "Narrow money" expanded $653bn, or 5.7%, over the past year. For the week, Currency increased $1.3bn. Total Checkable Deposits jumped $17.6bn, while Savings Deposits were little changed. Small Time Deposits slipped $1.2bn. Retail Money Funds added $1.8bn.

Money market fund assets jumped $19.2bn to $2.634 TN. Money Funds were down $99bn year-to-date, while gaining $58bn y-o-y (2.3%).

Total Commercial Paper surged $68.3bn to $1.021 TN. CP declined $21bn over the past year, or 2.0%.

Currency Watch:

The U.S. dollar index slipped 0.2% to 95.78 (up 6.1% y-t-d). For the week on the upside, New Zealand dollar increased 0.5%, the euro 0.4%, the Swedish krona 0.3%, the Swiss franc 0.2% and the Mexican peso 0.1%. For the week on the downside, the South African rand declined 1.1%, the Australian dollar 1.0%, the Brazilian real 0.8%, the Canadian dollar 0.7%, the British pound 0.3%, and the Norwegian krone 0.3%.

Commodities Watch:

The Goldman Sachs Commodities Index sank 4.2% (down 0.6% y-t-d). Spot Gold slipped 0.4% to $1,164 (down 1.8%). September Silver declined 1.1% to $15.48 (down 0.8%). August Crude sank $2.78 to $52.74 (down 1%). August Gasoline added 0.8% (up 37%), while August Natural Gas was unchanged (down 4%). September Copper dropped 3.0% (down 10%). September Wheat sank 2.5% (down 2.3%). September Corn gained 1.5% (up 10%).

Greece Crisis Watch:

July 10 - Financial Times (Peter Spiegel and Eleftheria Kourtali): "Eurozone finance ministers will decide on Saturday whether to keep Greece's prospects of staying in the eurozone alive, after lawmakers in the cash-strapped country voted in the early hours to back the government's bailout proposals. Greek prime minister Alexis Tsipras saw off a threat from rebels in his ruling coalition and overwhelmingly won the parliamentary vote in Athens on his reform plan. Earlier, Greek media reported that Left Platform, the hard left in Mr Tsipras's Syriza party, were going to vote for the plan. In a statement after the vote, which the government won with the help of pro-European opposition parties, Mr Tsipras said he had a 'strong mandate to complete the negotiations to reach an economically viable and socially fair agreement'."

July 5 - Reuters (Lefteris Papadimas and Renee Maltezou): "Greeks overwhelmingly rejected conditions of a rescue package from creditors on Sunday, throwing the future of the country's euro zone membership into further doubt and deepening a standoff with lenders. Stunned European leaders called a summit for Tuesday to discuss their next move after the surprisingly strong victory by the 'No' camp defied opinion polls that had predicted a tight contest."

July 9 - Financial Times (Claire Jones, Anne-Sylvaine Chassany and Peter Spiegel): "Jens Weidmann, the president of Germany's Bundesbank, has said doubts about Greek banks' solvency are 'legitimate' and 'rising by the day'. Mr Weidmann also said the majority of Greeks who had voted 'no' in Sunday's referendum had 'spoken out ... against contributing any further to the solvency of their country through additional consolidation measures and reforms'. The Bundesbank president, a member of the governing council of the European Central Bank who has called for Greek banks' €89bn liquidity lifeline to be scrapped, said it needed to be 'crystal clear' that responsibility for Greece lay with Athens and international creditors, and not the ECB. 'The Eurosystem [of eurozone central banks] should not increase the liquidity provision, and capital controls need to stay in force until an appropriate support package has been agreed by all parties and the solvency of both the Greek government and the Greek banking system has been ensured.' The Bundesbank president hit out at Athens for causing economic ruin. '[Eurozone member states] can decide for themselves not to service their debts, to collect taxes inadequately, and -- this is something I particularly fear in the case of Greece -- to lead their country's economy into deep trouble,' he said... The Syriza-led government had 'not only walked out on the previous agreements, but has been widely criticised as an unreliable negotiating partner'."

China Bubble Watch:

July 7 - Bloomberg (Jonathan Burgos, Kyoungwha Kim and Kana Nishizawa): "Foreign investors are selling Shanghai shares at a record pace as China steps up government intervention to combat a stock-market rout that many analysts say was inevitable. Sales of mainland shares through the Shanghai-Hong Kong exchange link swelled to an all-time high on Monday, while dual-listed shares in Hong Kong fell by the most since at least 2006 versus mainland counterparts. Options traders in the U.S. are paying near-record prices for insurance against further losses after Chinese stocks on American bourses posted their biggest one-day plunge since 2011. The latest attempts to stem the country's $3.2 trillion equity rout, including stock purchases by state-run financial firms and a halt to initial public offerings, have undermined government pledges to move to a more market-based economy...They also risk eroding confidence in policy makers' ability to manage the financial system if the rout in stocks continues, said BMI Research, a unit of Fitch. 'It's coming to a point where you're covering one bad policy with another,' said Tai Hui, the Hong Kong-based chief Asia market strategist at JPMorgan Asset Management... 'A lot of investors are still concerned about another correction."

July 6 - Financial Times (Gabriel Wildau): "An uneven recovery of Chinese stocks following official measures to halt a three-week sell-off has prompted warnings that government credibility is at stake in the performance of the market. Economists say that while the direct spillover from the stock market to the real economy is limited, any perceived failure of government moves could dent already slowing confidence in the broader economy. 'With authorities throwing a wide range of unprecedented tools (including pensioners' funds) at the equity market in order to prop it up, the stakes are now significantly higher,' Andrew Wood, head of Asia country risk at BMI Research, a unit of rating agency Fitch, wrote...'A failure to stabilise the market (and indeed to achieve a notable recovery from current levels) could lead to a crisis of confidence in the heretofore infallible state apparatus.' ...Even if the emergency steps succeed in boosting shares, they could undercut the government's claims that it intends to allow market forces to drive the economy, while regulators focus on ensuring transparency and fair competition. 'These measures could undermine the credibility of regulators in the long term. That's something they tried very hard to establish in the first place. Now it will have to be repaired,' said Shuang Ding, chief China economist at Standard Chartered. Liu Yang, who chairs Atlantis Investment Management... said investors must pay attention to the direction of policy above all. 'I believe the Communist party still has the final say over the stock market, even nowadays,' she said."

July 8 - Bloomberg: "The extra yield investors demand to hold junk debt in China widened the most in two months as the government's failure to avert a stock slump damped demand for risky assets. The gap between five-year top-rated and AA- rated corporate bond yields increased seven bps Wednesday to 142.25, matching the steepest climb since May 15, ChinaBond data show... China needs a 4 trillion yuan ($644bn) package to halt the panic, Tim Condon, the head of Asia research at ING Groep NV, wrote... 'While the outlook for the financial market is unclear, investors have chosen to dump the most risky assets,' Liu Dongliang, a Shanghai-based senior analyst at China Merchants Bank Co., said.'"

July 6 - New York Times (David Barboza): "With his stock market riches, Gong Yifeng bought a riverfront apartment here for his son and daughter-in-law. He can eat well and travel abroad. He can also afford to pay for his granddaughter's education. But the losses are rapidly piling up for Mr. Gong, a retired shipyard worker. With China's stock market 30% off its highs, his portfolio is down more than $30,000 in the last few weeks. 'I don't need a high-flying market, just a stable one,' Mr. Gong said. Millions of ordinary investors like Mr. Gong, who piled into an ever-soaring Chinese stock market over the last year, are bracing for a roller-coaster ride... As property prices slumped, the government started to cut interest rates in an effort to stabilize the economy. With share prices looking undervalued and real estate in a rut, money flowed into stocks, said Chang Chun, a finance expert and executive dean at the Shanghai Advanced Institute of Finance... The government further fueled interest by viewing the market as a way to help start-ups and innovative companies. The state-run news media began publishing articles about the coming bull run and the creation of exchanges geared toward listing new companies. As droves of investors jumped on board, the stock market boom began to head into bubble territory."

July 7 - Bloomberg: "Plunging Chinese equities have damaged the confidence of its main driving force -- the more than 90 million individual investors who make up about 80% of the market, according to a survey of households. While they are 'relatively optimistic' about the future, they still want to reduce their stakes as their gains vanish, according to a poll by the Survey and Research Center for China Household Finance at Southwestern University of Finance and Economics. Only 40.5% of households still had gains in their stock accounts in the week starting June 27, down from 73.8% in the period June 15 to June 18, it found."

July 7 - Bloomberg: "China will limit the opening of new futures contracts in an index of small-company stocks to rein in excessive trading and stem a bear market rout. Investors can buy or sell at most 1,200 new contracts linked to the CSI 500 Index per day starting Tuesday, the China Financial Futures Exchange said... 'The move is intended to limit the power of short-selling on the futures market and this is what the exchange can do now under the pre-condition that it doesn't break the rules of the game," said Jiang Lin, an analyst at Xinhu Futures... 'However, the effect may be limited as overall valuations of small caps are still pretty high. Once the downtrend takes hold, it cannot be easily reversed.'"

July 9 - Reuters (Ruby Lian and David Stanway): "Large Chinese steelmakers' losses in core business more than doubled during the first five months from a year earlier as tumbling steel prices plunged producers into red, a top official of the China Iron & Steel Association (CISA) said... CISA members, comprising of 101 big mills, posted a loss of 16.48 billion yuan ($2.65bn) in steelmaking business for January-May, which was 10.36 billion yuan more from the same period of last year, according Zhang Guangning, CISA's chairman. 'It's obvious that China's apparent crude steel consumption has reached the peak, and the large growth of demand has became a history,' Zhang said... Chinese steel prices are at their lowest in more than 20 years as the stuttering economy is hitting demand for a range of commodities including iron ore, steel and copper, threatening the survival of small steel mills."

Fixed Income Bubble Watch:

July 7 - Bloomberg (Nabila Ahmed and Cordell Eddings): "Junk-bond investors who've been enjoying more than six straight years of gains fueled by easy-money policies may soon find their streak nearing an end. After the three strongest years on record for issuance and annual returns of 15% since the start of 2009, there are growing signs of trouble in high-yield debt. For every speculative-grade company that has had its credit rating upgraded this year, about two others have been downgraded -- the worst ratio since 2009. U.S. high-yield companies posted two consecutive quarters without earnings growth for the first time since the financial crisis. And their average level of debt-to-earnings is at an all-time high. All of this is creating what Bank of America Corp., the second biggest underwriter of the notes, sees as a grim outlook for investors... 'The conditions are the worst since the crisis and therefore outlook is the worst since the crisis,' Michael Contopoulos, the head high-yield strategist at Bank of America, said... 'The longer-term prospects for the asset class are worrying.' Junk bonds lost 1.52% last month -- their worst month since September..."

U.S. Bubble Watch:

July 9 - Reuters (Sam Forgione): "Investors in U.S.-based funds poured $14.1 billion into stock funds in the week ended July 8 marking the biggest inflows into the funds since mid-December, data from Thomson Reuters' Lipper service showed..."

July 7 - Bloomberg (Alex Barinka): "Buybacks and dividends are rising to records in the U.S., and for many chief executives, that means a fatter pay check -- even if sales aren't growing. Eleven of the 15 non-financial U.S. companies that spent the most on buybacks last year base part of CEO pay on earnings per share or total shareholder return, or both... Linking compensation to buybacks and dividends can encourage managers to sacrifice funds that could be used for long-term investments, economist William Lazonick said. It also raises the prospect that executives are being paid for short-term returns rather than running a business well. 'A lot of people are making money without actually creating value,' said Lazonick, an economist who... has written about the economic effect of buybacks for the Harvard Business Review."

July 10 - Washington Post (Michael A. Fletcher and Steven Mufson): "The sprawling pharmaceutical plants nestled in the hills of this town west of San Juan are testament to the unusual nature of this island's struggling economy. The factories once employed a small army of highly trained workers that would be the envy of many other places in the United States. But those jobs -- for engineers, chemists and others skilled in precision manufacturing -- have been rapidly disappearing for largely the same reason they came here in the first place: policy decisions made in Washington. A generous series of tax breaks enacted by Congress shielded the profits of U.S. corporations operating here and helped transform Puerto Rico from a largely agrarian society to a manufacturing powerhouse. But what Washington gave, it also took away. When Congress decided to phase out a crucial tax credit that ended in 2005, it helped plunge Puerto Rico into a recession that began a decade ago and has yet to end."

July 6 - New York Times (Mike Isaac): "Shortly after presenting her start-up to potential investors at a conference, Nancy Hua was bombarded by eager suitors. A little more than 48 hours later, the Silicon Valley entrepreneur had amassed about $2 million from wealthy individuals known as angel investors. The total number of angels that Ms. Hua raised money from: 21. And she could have gotten more if she had not cut them off. 'Thirty seconds into my pitch, three people emailed me saying they wanted to invest in my company,' Ms. Hua, 29, said... 'We had dozens of people whose money we turned down.' For entrepreneurs, nabbing numerous angels -- and prominent ones to boot -- has become a kind of trophy collecting, a chase that comes with some risk for their companies. And for many relatively new investors, a winning bet on a hot start-up can pay off richly in Silicon Valley cultural capital. Last year, over 2,960 angels participated in a financing round, more than triple the 822 angels who did so in 2010, according to CB Insights... There is even a moniker for financing rounds that have many angels with no lead investor: 'party rounds.'"

July 7 - Bloomberg: "The U.S. trade deficit widened in May as exports declined by the most in three months, showing businesses were having trouble drumming up sales to overseas customers. The gap grew 2.9% to $41.9 billion... Exports dropped 0.8% on declining demand for commercial aircraft and industrial equipment... While persistent U.S. household spending led to record automobile imports, unsettled European and Chinese economies are limiting prospects for a pickup in exports."

Global Bubble Watch:

July 8 - Bloomberg (Jesse Riseborough): "Fears of faltering Chinese growth ignited a $143 billion meltdown in global mining stocks as investors confront sputtering demand in the world's biggest consumer of commodities. The Bloomberg World Mining Index of 79 producers dropped 17% in the past 10 days as prices for industrial metals such as copper, nickel and aluminum sank to six-year lows. The price of iron ore... slumped 10% Wednesday to its lowest since at least 2009 as new supply floods the market. China is set to grow at its slowest pace in a quarter of a century, sapping the country's demand for commodities and crimping mining companies' profits."

July 8 - Bloomberg (Lyubov Pronina): "Turbulence in global markets is pushing developing-nation debt sales into a freeze. Brazil is delaying its dollar offering to the end of the quarter... Kazakhstan and the Iraqi region of Kurdistan have yet to tap markets after completing investor meetings last month, while the number of issuers forced to postpone offerings will only grow, according to Sergey Dergachev at Union Investment Privatfonds GmbH in Frankfurt. Debt sales have dried up since Gabon's $500 million offering a month ago as a rout in Chinese equities and the deadlock over a bailout for Greece takes the country to the brink of exiting the euro...'There's a confluence of risks worrying markets at the moment including the Greek impasse, the Fed and also worries about stock-market volatility in China,' Mark Baker, who helps oversee about $1.5 billion in emerging-market debt at Standard Life Investments Ltd. in London, said... 'Most issuers would like to wait for markets to stabilize, sentiment to improve and ultimately achieve better issue terms.'"

July 7 - Bloomberg (Anna Andrianova and Andrey Biryukov): "The BRICS group of nations, which represent more than a fifth of the global economy, talked up closer financial ties on the eve of a summit in Russia hosted by President Vladimir Putin. BRICS finance ministers and central bankers, meeting Tuesday in Moscow, stepped up work on a development bank and finalized a $100 billion pool of foreign reserves to help one another out of liquidity binds. The leaders of Brazil, Russia, China, India and South Africa meet July 8-9 in the city of Ufa. They 'believe the time is ripe to create their own financial institutions,' Kremlin foreign-policy aide Yuri Ushakov said. The five nations gather at a time of global market stress, with China's stock market suffering a rout and Greece's future in the euro in the balance."

July 7 - Financial Times (David Oakley): "The global asset management industry grew to a record size last year as equity and bond values rose sharply, helped by hopes of economic recovery and central bank interventions in the markets. Assets under management increased to $74tn, the highest figure recorded by the Boston Consulting Group's annual survey. Profits for asset managers also rose to $102bn, matching the historic peak in 2007."

Europe Watch:

July 6 - Washington Post (Griff Witte): "When voters in Greece did the previously unthinkable and defied Europe's political titans by spurning their bailout proposal, some of the loudest rejoicing came from well beyond the country's borders. Across the continent -- from north to south, from the far right to the far left -- parties that have rocketed to prominence with populist rhetoric celebrated what they saw as perhaps the most direct strike yet at the heart of the European order. 'Today in Greece democracy won,' Pablo Iglesias, leader of the radical leftist Spanish party Podemos, cheered... The result was a victory against 'the oligarchy of the European Union,' declared Marine Le Pen, leader of France's far-right National Front party. The enthusiastic response from such unlikely bedfellows reflects the strange new politics of Europe, which have pitted mainstream parties against formerly fringe movements that, for different reasons, are determined to tear down the systems and ideologies that have governed the continent for decades. Lately, the outsiders have been surging."

EM Bubble Watch:

July 7 - Bloomberg (Jasmine Ng and David Stringer): "Iron ore's bear market deepened, with prices dropping below $50 a ton for the first time since April on concern that low-cost supplies from Australia and Brazil will expand further while demand stumbles in China... Prices entered a bear market Monday, dropping more than 20% from a June high. Iron ore's renewed slump highlights that the same factors of surging supply and stalling demand growth, which dragged prices to a decade-low early April, remain at the forefront."

July 9 - Bloomberg (Nathan Crooks and Andrew Rosati): "Venezuela's largest bank note of 100 bolivars is now worth about 16 U.S. cents on the black market, following a 33% plunge in the past month. The currency weakened to 616 per dollar Thursday, meaning the greenback fetches 100 times more bolivars in the black market than it does at the primary official rate..."

Geopolitical Watch:

July 8 - Wall Street Journal (Andrew Brown): "Far more than simply a market crisis, the turmoil on the Shanghai Stock Exchange is viewed by China's leadership as a potential security threat to the regime. That helps explain the barrage of measures unleashed by financial authorities to counter a sudden market downturn that threatened to shake public confidence in the government. In that sense, the unprecedented rescue moves, including a multibillion-dollar fund set up by Chinese brokerages at the government's behest to buy blue chips, is a preview of what's to come following the passage last week of a national-security law that massively expands the definition of threats to the state to cover almost every aspect of domestic life, including 'financial risk,' as well as international affairs. The law explicitly states that economic security is the foundation of national security."

Russia and Ukraine Watch:

July 9 - BBC: "A general in line for the highest US military post says Russia poses the greatest threat to national security. During his confirmation hearing to become chairman of the Joint Chiefs of Staff, Marine Gen Joseph Dunford called Russia's recent actions "nothing short of alarming". Relations between the US and Russia have deteriorated since Russia annexed Ukraine's Crimea region last year. A pro-Russian insurgency in eastern Ukraine has also prompted US sanctions. 'So if you want to talk about a nation that could pose an existential threat to the United States, I'd have to point to Russia.' Gen Dunford told senators..."

Japan Watch:

July 9 - Bloomberg (Toru Fujioka): "It could be difficult for the Bank of Japan to taper its record monetary stimulus before a planned sales-tax hike in 2017 and the government may need to compile a 2.5 trillion yen ($20bn) economic package to cushion the blow to households, an adviser to the prime minister said. Etsuro Honda, who has known Prime Minister Shinzo Abe for three decades and advises him on economic matters, said the government would need to 'take a cautious approach' after an increase in the levy last year sparked a recession."