"Not Totally Dead" Yet

In the Chicago suburbs of Burr Ridge, Naperville, and Hinsdale, sales of high-end real estate hit a huge slump this summer that still continues.

For example, Crain's Chicago reports the city of Burr Ridge, has 100 homes on the market for at least $1 million, but only 14 have sold at that price in the past six months.

Crain's Chicago has the details in This suburb has too many $1 million-plus homes for sale (emphasis mine).

"It's been disquietingly slow, brutally slow getting these sold," said Linda Feinstein, the broker owner of ReMax Signature Homes in neighboring Hinsdale. "It feels like the brakes have been on for months."Sales slowed down all over the Chicago area this summer, and sometimes potential sellers don't get the message soon enough, which creates an over-stock of inventory.

"It's not as busy as we'd all like it to be, but it's not totally dead," said Dave Ricordati, a Coldwell Banker agent with three $1 million-plus listings, the newest of which has been on the market since July. "I mean, it's not 2009 or 2010," when the real estate market was at a virtual standstill.

Another factor in the backlog, said Linda Saracco, a ReMax Signature agent who's been working Burr Ridge for over 30 years, is that "a lot of our sellers are baby boomers who bought in the '80s or '90s, built up a lot of equity in their homes and are ready to cash it in."

When the market doesn't deliver a buyer who's willing to pay the price they want, "they're not taking it. They'll wait and see if they can get their number."

Her prediction: They won't.

Ready to Cash In But No Buyers

I have to commend ReMax agent Linda Saracco for her accurate, honest assessment "They won't [get their price]".

This is precisely what happens when everyone heads for the exit door at the same time.

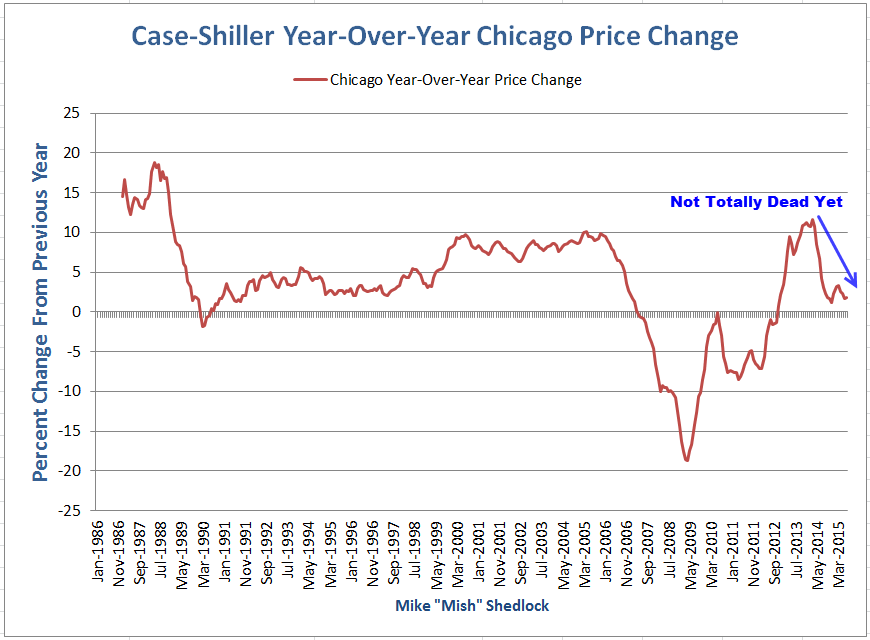

Case-Shiller Chicago Update

The Crain's report got me thinking about the most recent Case-Shiller Home Price Update.

Let's put a spotlight on Chicago where things are also "not totally dead" .... yet.

Chicago Year-Over-Year-Price Changes

Chicago Home Price Index

Chicago had a huge boom followed by a huge bust that never quite recovered.

Economic Rot vs. Home Price Rot

Unlike overall economic weakness that starts at the periphery and spreads to the core, real estate rot frequently starts at the high end as buyers balk.

Each drop in high-end prices progressively hits the next lower home price group level.

Illinois Rush

A rush for the exit in Illinois is underway. And why shouldn't there be one? Who can really afford such prices anyway?

Certainly not millennials with a mountain of student debt or those stuck in low-wage jobs.

A major part of the problem is the overall set of asset bubbles thanks to loosey-goosey policies at the Fed.

But why a rush to the exit in Illinois and not everywhere?

In Illinois, we have a second problem: State of Illinois policies.

Oh Come Oh Come Emanuel

No, I won't do a musical tribute with that title (accepting your thanks in advance). But Mayor Rahm Emanuel is crazy if he thinks tax hikes are the way out of Chicago's fiscal mess.

Yet, on September 23, I noted Chicago Tax Collector Hath Arrived With Massive Tax Hike: Emanuel Says "No Stone Unturned"

Worse yet, Emanuel says he's "Not Done Yet [hiking taxes]" and he will leave "no stone unturned" in the search for revenues.

Bet Your Bottom Dollar

You can bet your last dollar on this: When politicians promise to raise your taxes, they will, and by more than they say.

Emanuel will raise property taxes by the most in Chicago history. And that's not going to affect property values or the desire to cash out? What Fantasyland is Emanuel living in?

It's not just Chicago. Illinois has a litany of problems that make people want to leave. Citizens want to leave. And they will.

But not at the property prices they expect.

Mish Proposal

On May 4, in Beware, the Tax Man Has Eyes on You I wrote ...

To spare the citizens of Illinois massive tax hikes, the only reasonable course of actions are as follows:Advice Not Accepted

- Halt defined benefit pension plans for new employees

- Eliminate collective bargaining of public unions

- Scrap Davis Bacon and all prevailing wage laws so that cities do not have to overpay for services

- Enact right-to-work legislation

- Pass bankruptcy legislation allowing cities, municipalities, and other taxing bodies the right to declare bankruptcy

Had options 1-4 been done a decade ago, Illinois would not be as bad off as it is today. Now, even those measures cannot and will not fix the problems.

The tax man did not listen. He never does.

Related Articles

On March 2, I noted Illinois Pension Plans 39% Funded; Taxpayers On the Hook for $105 Billion in Liabilities; It Will Get Worse!

On April 1, I noted the Shockingly Bad Fiscal Health of Chicago (and the Financial Engineering Chicago Uses to Hide that Fact).

On September 29, Illinois Policy Institute Vice President Michael Lucci noted Food Stamp Growth Outpaces Illinois Job Creation 5-4 During Recovery.

Get Me the Hell Out of Here

Finally, please consider my August 13 article Get Me the Hell Out of Here.

Policies in Illinois are to hugely blame for this "rush to the exit" by businesses and ordinary taxpayers alike.

The net business flight and high-end wealth flight from Illinois to other states will now accelerate thanks to policies in the city of Chicago and the state of Illinois in general.