Let's start with the latest on the global descent into negative interest rates:

Fed would consider negative rates if economy soured - Yellen

(Reuters) - The Federal Reserve would consider pushing interest rates below zero if the U.S. economy took a serious turn for the worse, Fed Chair Janet Yellen said on Wednesday."Potentially anything - including negative interest rates - would be on the table. But we would have to study carefully how they would work here in the U.S. context," Yellen told a House of Representatives committee.

This would happen if the economy were to "deteriorate in a significant way," she said, adding that she believed negative rates "would have some at least modest favorable effect on banks' incentives to lend."

Janet Yellen is now firmly in the central banking "whatever it takes" mainstream. And since -- if the ongoing contraction in manufacturing is any indication -- the economy is indeed "deteriorating in a significant way," the US is now likely to join Europe in pushing rates down (or allowing rates to fall) to negative territory.

But already, the impact of zero and near-zero rates has been seismic. Virtually every class of financial entity, from retiree to central bank has, driven by a need for yield, begun taking the kinds of chances that used to be associated with gambling addiction or drug abuse. See the previous two entries in this series: We're All Hedge Funds Now and We're All Hedge Funds Now, Part 2: Tech Startups And Nigerian Bonds.

The latest bit of surreal news on this front concerns the Swiss National Bank, once upon a time the virtual definition of rock-solid risk aversion, and its growing and highly volatile -- get this -- equity portfolio:

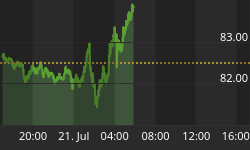

Swiss central bank owns big stake in troubled drug maker

(CNN Money) -Switzerland might be known for making precise clocks, but its timing couldn't be worse on at least one investment.The Swiss central bank increased its stake in Valeant Pharmaceuticals (VRX) right before the controversial U.S. pharmaceutical company was accused of Enron-like fraud.

First, you might be wondering, what is a European central bank doing owning stocks in the first place? In recent years the Swiss National Bank has used its swelling currency reserves to acquire equities. The central bank owned nearly $39 billion worth of shares in 2,569 U.S. companies as of the end of September.

The bank doesn't handpick its stocks. The central bank's website says it "only invests passively." It uses a set of rules based on strategic benchmarks to determine which stocks to add to its massive portfolio.

Unfortunately for Swiss taxpayers, one of those stocks is Valeant, the troubled pharmaceutical company whose share price is in freefall mode.

The SNB owned 1.44 million shares of Valeant as of the end of September, up from 1.28 million at the end of June, according to Securities and Exchange Commission filings. The central bank said its Valeant stake was worth about $257 million.

Valeant stock has more than halved to $84, from $178 at the end of September. That means that if the Swiss central bank did not sell any shares, it is staring at a loss of about $146 million on its Valeant holdings.

Other than Valeant, the SNB's portfolio looks like that of a typical large-cap equity fund's nifty-50 zero-analysis list, which is to say Apple, Google, GE, Microsoft and other familiar multinationals. These are the names that money managers pile into at the top of a cycle when they start worrying about how to justify their overvalued losers and decide that whatever happens they won't be fired for owning Apple. But of course at the top of a cycle even the Apples of the world are destined to fall by half or more.

So what does it mean that governments and central banks have become hedge funds?

Well, now that the monetary authorities have both the ability to push stocks up by buying them with newly-created currency and a burning need to do so in order to protect their multi-billion dollar equity portfolios, can there be any doubt about the course of monetary policy and general financial intervention in the next couple of years? No there can't. In effect, Wall Street now gets to decide on stock prices rather than wager on them. Every 5% drop in the S&P 500 will be met with both easier money and direct buying by the Swiss, Japanese, Chinese, European and US central banks. Markets -- in their old definition as price signaling mechanisms that tell capitalists what to do with capital -- are effectively over.

As valuations become more and more unrealistic -- either through rising share prices or falling corporate profits the scale of the necessary intervention will expand to the point that central bank equity portfolios will dwarf those of most hedge funds and mutual funds.

The amount of money creation necessary to buy up all those equities will spook the currency markets, leading to even more central bank intervention, which in turn will expose the contradiction inherent in the manipulate-all-markets strategy: Buying stocks with newly-created money is bad for exchange rate stability, but raising interest rates to protect a currency is bad for equity market valuations. One or the other will have to give.